Global| Nov 20 2013

Global| Nov 20 2013German PPI Sinks in October

Summary

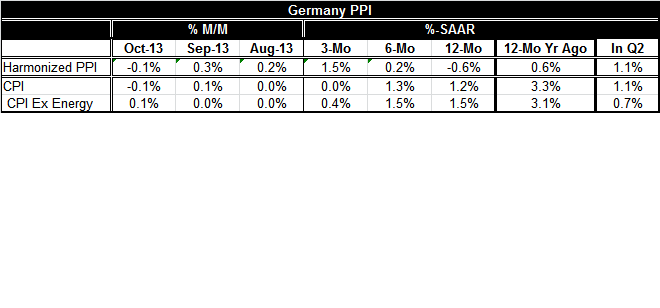

PPI trends in Germany are still working lower. This is also true of the HICP. Over 12-months the German PPI is showing contraction. Over 12-months the German CPI is rising by 1.2% or by 1.5% excluding energy. The chart depicts the [...]

PPI trends in Germany are still working lower. This is also true of the HICP. Over 12-months the German PPI is showing contraction. Over 12-months the German CPI is rising by 1.2% or by 1.5% excluding energy.

PPI trends in Germany are still working lower. This is also true of the HICP. Over 12-months the German PPI is showing contraction. Over 12-months the German CPI is rising by 1.2% or by 1.5% excluding energy.

The chart depicts the German, Austrian and UK PPI/WPI trends. Each of these countries (two, EMU members, one, just an EU member) shows a dropping PPI/WPI over 12-months. The CPI result reminds us that energy is playing a role in this price weakness. But even the CPI fails to show that much difference between overall CPI and core CPI trends. In short, the trend is the trend. You can put a cherry on top or not. For the PPI energy has a much higher weight, but the trend is still the trend (FYI, of the four EMU members that report an `ex-energy' or `ex-food and ex-energy' PPI, the most recent level of that index is still lower than it was one year ago).

Rather than splitting hairs over oil prices, which are weak and look to remain weak given weak global growth and the supply side effects, we need to consider what prices are doing and what that means.

Once upon a time, we looked upon deflation as a Japanese problem. And why not? Japan had a concentration of special problems: (1) a shrinking population, (2) overinvestment, (3) a sharply rising and overvalued exchange rate in an export-oriented economy, (4) a high savings rate (low consumption), and (5) huge federal debt. It could not easily solve these problems on its own. So it floundered.

But now many countries also share at least some of Japan's special characteristics. A slow-growing population is now common, even if not all countries with weak population growth have a shrinking population. The sharp drop-off in demand growth has left the world with excess capacity. This condition is not because of overinvestment, but the slack due to the sharp drop in global demand has the same effect on pricing and growth. Similarly, the sharp drop-off in demand has left all nations with much weaker growth abroad and tougher competition from global competitors who face the same circumstances. This is much the same as what an overvalued exchange rate did to Japan. A rising exchange rate will also depress domestic prices; weak demand is creating its own deflation effect today. Japan's high savings rate was an issue for it to deal with, as it is an issue for some countries that continue to run current account surpluses (excess domestic savings). But beyond that, the collapse in demand and the slowing of growth have left many with excess debt and now many individuals are forced to save even more to combat their sudden excess indebtedness while austerity is the prescription for national policies.

While Japan still occupies a special place in the pantheon of global indebtedness, many countries, most notably many in the eurozone, have found themselves forced to austerity and are even worse off than Japan whose slow growth lasted for decades because Japan tried to address its debt problem using a policy of postponement while Europe has not.

When we stack up our current global macroeconomic circumstances with the `special case' Japan once was (and in some sense, still is), we see many similarities. However, nations, particularly, when acting together, have the capacity to change the environment. They can use fiscal policy. They can (and have been) use monetary policy. But for the most part, global fiscal policies have been contractive at the same time that private sectors are struggling. Monetary policy has been accommodative in the face of very strong headwinds. Beyond achieving some sort of stabilization, it has largely failed to rekindle growth.

But because we are recovering from of an era of excess and because many look at this austerity as the penance or policy to restore health, many see this period of such weak growth as simply the price to pay for past policy errors.

The question is: "Is that true?"

Is there no way to restore the global economy to health but by this path that leads trough such misery? If the concern is `moral hazard' hasn't there been enough pain to date to render that as no concern at all? Is all this really necessary? Such high unemployment? Such dislocation? Such political instability?

It seems to me that the suffering has been great and has been too much- it is not a punishment that fits the crime. Moreover, as a question of fairness, many of the trouble-makers are making out just fine in this new environment while those who were the pawns in the game of excess are now suffering the most. The question is if there isn't another way to pump some air into the balloon without overinflating it again? I think the answer is `yes.' But this is not an answer with much of an echo, at least not from important policymakers. I fear the over-reliance on monetary policy as current period placebo will morph into an engine of destruction later. I also fear than an improper use of fiscal policy could make things even worse.

The very weak trends we see in prices and in inflation are warnings on the road to deflation. There may still be further turnoffs we will encounter as we stay on this path. But will policymakers take any of them? Or are they on a predetermined course because they misjudge the ultimate costs? With economic in stability always come political instability. And we already see much of this in train. Europe has no consensus on what are some very clear and pressing needs. The US political situation is made up of two inflexible parties each thinking it can break the other instead of live with it. The Middle East is a mess. China has just announced watershed changes in its policies. Japan is trying to dig out of its deflation. All that should be grounds to rethink our current policy path. But will those in a position to see it, embrace change and make a clear break from the destructive policies of the past?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief