Global| May 07 2019

Global| May 07 2019German Orders Mount a Weak Rebound

Summary

Germany's real orders continue to run weak. Orders rose by 0.6% in March, a weak rebound from a 4% decline in February and a 2.1% drop in January. Foreign orders gained a solid 4.2% (still unimpressive in the wake of a 5.8% February [...]

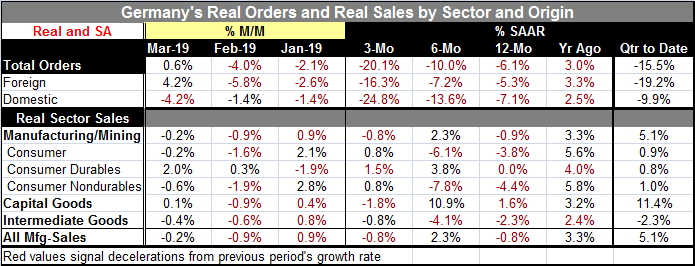

Germany's real orders continue to run weak. Orders rose by 0.6% in March, a weak rebound from a 4% decline in February and a 2.1% drop in January. Foreign orders gained a solid 4.2% (still unimpressive in the wake of a 5.8% February drop). Domestic orders fell by 4.2%, marking the third straight month of domestic order declines and of substantial monthly declines.

Germany's real orders continue to run weak. Orders rose by 0.6% in March, a weak rebound from a 4% decline in February and a 2.1% drop in January. Foreign orders gained a solid 4.2% (still unimpressive in the wake of a 5.8% February drop). Domestic orders fell by 4.2%, marking the third straight month of domestic order declines and of substantial monthly declines.

Sequential weakness

Sequential growth rates from 12-month to six-month to three-month show accelerating rates of decline so that the six-month and three-month growth rates (for the most part) demonstrate annualized declines in double digits (except for foreign orders over six months). Over three months domestic orders are plunging at a 24.8% annualized rate – and that can't be good news. Over six months the annualized pace of decline is 13.6% and over 12 months real German domestic orders fall by 7.1%

Perspective for domestic order weakness

The 7.1% drop in domestic orders year-on-year is severe. But in the last three German recessions, domestic orders fell on average by 19.1% in the recession. In 2011 in this expansion, there was a domestic order decline of 13.2% in the expansion period. In 2016, there was a decline of 5.4%. This sort of decline is survivable. The drop in domestic orders is severe and it is eye-catching, but it is not any sort of recession indicator…yet. The German government has slashed its 2019 growth forecast to 0.5%. This would mark a sharp slowdown after expansion rates of 2.2% in 2017 and 1.4% in 2018. But a slowdown is not a recession.

German foreign weakness

German exports seem to be suffering from a variety of ailments. Last month it was a plunge in German export orders to Turkey that helped made the foreign data so week. It is also thought that Brexit uncertainty has been doing harm to the German factory sector. But in March foreign orders rebounded by 4.2% month-to-month as domestic orders hogged the limelight for weakness.

Sales vs. orders

Quarter-to-date (this is now for the completed Q1 period) shows double-digit declines nearly all around: -15.5% for total orders, -19.2% for foreign orders and -9.9% for domestic orders. In the quarter, manufacturing sales are doing much better than orders as they rose at a 5.1% annual rate.

Real sales by sector

Real sector sales showed their second decline in a row, falling by 0.2% in March. But there is much less weakness in sales than in orders. Manufacturing sales show a 0.8% annual rate drop over three months and a 2.3% pace of increase over six months. But over 12 months, sales still fall by 0.8%. Year-on-year all categories of sales are slower than their 12-month growth rates of 12-months ago. Only capital goods show a sales rise over 12 months (a gain of 3.2%).

Very weak sector in a weak economy

On balance, the German factory sector is very weak. Some say that the sector itself is in recession, but such talk is all euphemism since only a whole economy can be in recession- recession is a macroeconomic phenomenon, not a sector phenomenon.

Spreading impact of weakness

Germany is struggling and the focus of the recent weakness is the bind it will put Germany in because this weakness means lighter tax revenues and Germany is trying hard to run a fiscal surplus. Germany also has dug its heels in on paying a greater proportion of its GDP to benefit NATO. The outlook is muted and Europe is in the midst of elections that could turn its house upside down. Europe faces more than just a ‘German' problem.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief