Global| Sep 26 2008

Global| Sep 26 2008German Inflation Behaves a Bit…

Summary

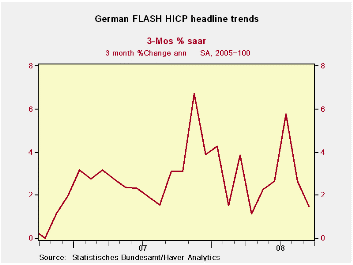

The chart on the left shows German inflation has been soaring and chopping around, then, recently it moved into a still-choppy but lower range. Headline inflation is and has been decelerating. But core inflation (only available thru [...]

The chart on the left shows German inflation has been soaring and chopping around, then, recently it moved into a still-choppy but lower range. Headline inflation is and has been decelerating. But core inflation (only available thru August) is still accelerating. Of course oil prices broke lower in this period but have since moved higher, implying the headline rate’s improvement is still a bit suspect. Core inflation over 3 months and 6 months shows some tendency to accelerate but for both the German CPI definition as well as the HICP definition through August year/year core inflation is below the 2% ceiling that applies to the overall EMU HICP. That much is good news. But Germany is also one of the EMU’s best inflation-controlled economies and it barely skates under this barrier for core inflation so we can expect that the news and trends for all of EMU are worse.

Energy prices continue to muck-up the inflation picture. Past energy increases still elevate the 12-month headline rate to a pace that makes the ECB somewhere between uncomfortable and embarrassed. Money growth and credit growth in EMU continue to be strong. Yet the growing US financial crisis and spreading economic weakness put the ECB on the spot when it comes to policy decisions. We suspect inflation is still the ECB’s dominant concern and wonder if it will be able to shift its focus fast enough to cushion the blow on growth that the overly strong euro and weakening global economies have in store for Europe.

| German HICP and CPI | |||||||

|---|---|---|---|---|---|---|---|

| Mo/Mo % | Saar % | Yr/Yr | |||||

| Sep-07 | Aug-07 | Jul-07 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| HICP Total | 0.2% | -0.2% | 0.4% | 1.5% | 2.1% | 3.0% | 2.6% |

| Core | #N/A | 0.3% | 0.3% | 2.7% | 1.7% | 1.9% | 2.3% |

| CPI | |||||||

| All | 0.2% | -0.2% | 0.3% | 1.1% | 2.3% | 2.9% | 2.7% |

| CPI ex Food & Energy | #N/A | 0.2% | 0.2% | 2.3% | 1.5% | 1.8% | 2.3% |

| Food | #N/A | 0.4% | 0.9% | 5.5% | 4.6% | 7.0% | 3.2% |

| Alcohol | #N/A | 0.3% | -0.5% | -1.8% | 0.5% | 4.1% | 2.7% |

| Clothing & Shoes | #N/A | 1.4% | -1.1% | 1.2% | -1.4% | 1.4% | 1.7% |

| Rent & Utilities | #N/A | -0.2% | 0.4% | 2.6% | 4.0% | 3.9% | 1.6% |

| Health Care | #N/A | 0.1% | 0.2% | 3.2% | 2.4% | 1.8% | 1.2% |

| Transport | #N/A | -1.3% | 0.2% | -1.1% | 2.9% | 4.7% | 2.3% |

| Communication | #N/A | -0.4% | 0.1% | -3.9% | -3.6% | -3.6% | -1.0% |

| Recreation & Culture | #N/A | -0.1% | 0.9% | 3.3% | 1.4% | 0.4% | 0.5% |

| Education | #N/A | -1.1% | 1.0% | -1.7% | -6.2% | 3.4% | 31.4% |

| Restaurant & Hotel | #N/A | 0.5% | 0.3% | 3.4% | 2.7% | 2.3% | 3.0% |

| Other | #N/A | 0.0% | 0.1% | 1.1% | 1.5% | 1.8% | 2.9% |

| Diffusion | 45.5% | 36.4% | 36.4% | ||||

| Type: | Diffusion: Current Compared to | 6-mo | 12-mo | Yr-Ago | -- | ||

| Shaded regions are lagged by one month due to missing month current observations | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief