Global| Nov 25 2002

Global| Nov 25 2002Existing Home Sales Up Again

by:Tom Moeller

|in:Economy in Brief

Summary

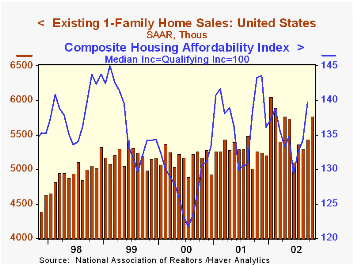

Sales of existing single family homes rose much more than expected in October. Sales rose 6.1% from September which was revised up slightly. Sales through October were up 11.0% versus last December. During the first ten months of 2002 [...]

Sales of existing single family homes rose much more than expected in October. Sales rose 6.1% from September which was revised up slightly.

Sales through October were up 11.0% versus last December. During the first ten months of 2002 sales were up 5.3% versus 2001.

Home sales rose in each of the country's regions.

The median price of an existing home rose 1.1% to $159,600 (9.8% y/y). The median price in September was revised down.

The figures reflect closings of past home sales.

The average rate on a conventional 30-year mortgage rose slightly last month versus September to 6.11%. Rates averaged 6.97% during all of last year. The decline this year in mortgage rates has combined with strong growth in disposable income to offset higher home prices and thus raise home affordability.

| Existing Home Sales (000, AR) | Oct | Sept | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Existing Single-Family | 5,770 | 5,440 | 9.5% | 5,291 | 5,159 | 5,193 |

by Tom Moeller November 25, 2002

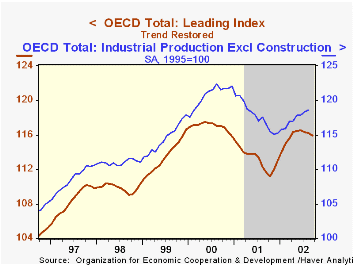

The OECD Index of Leading Indicators fell in each of the three months ending in September, heralding an end to the steady gains in industrial production of this year.

In the European Union, industrial production rose through the summer capped by a strong 1.5% August gain in Germany, but German leading indicators have fallen moderately in each of the last four months. EU leaders also have fallen in each of the last four months.

In the UK, production already has started to move lower, down in three of the four months ended September (-0.7% YTD). Leaders have fallen in the last two months.

Production in France has moved sideways since some respectable monthly gains early this year. Leading indicators in France have fallen in each of the last four months.

Trends in Japan have been firm relative to Europe. Production in Japan fell moderately in September but has gained 5.1% YTD. Leading indicators have been moving steadily higher since last Fall with a modest decline only this past September

The OECD Economic Outlook (Preliminary Edition) for November 2002 can be found by clicking here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief