Global| May 29 2020

Global| May 29 2020Euro Area EU Indexes Have Minor Bounce

Summary

A slug of economic data hit the tape at the end of month and for the first time really since the pandemic kicked into gear eco-data have snatched the headlines from COVID-19. The EU Commission indexes are a common set of data across [...]

A slug of economic data hit the tape at the end of month and for the first time really since the pandemic kicked into gear eco-data have snatched the headlines from COVID-19.

A slug of economic data hit the tape at the end of month and for the first time really since the pandemic kicked into gear eco-data have snatched the headlines from COVID-19.

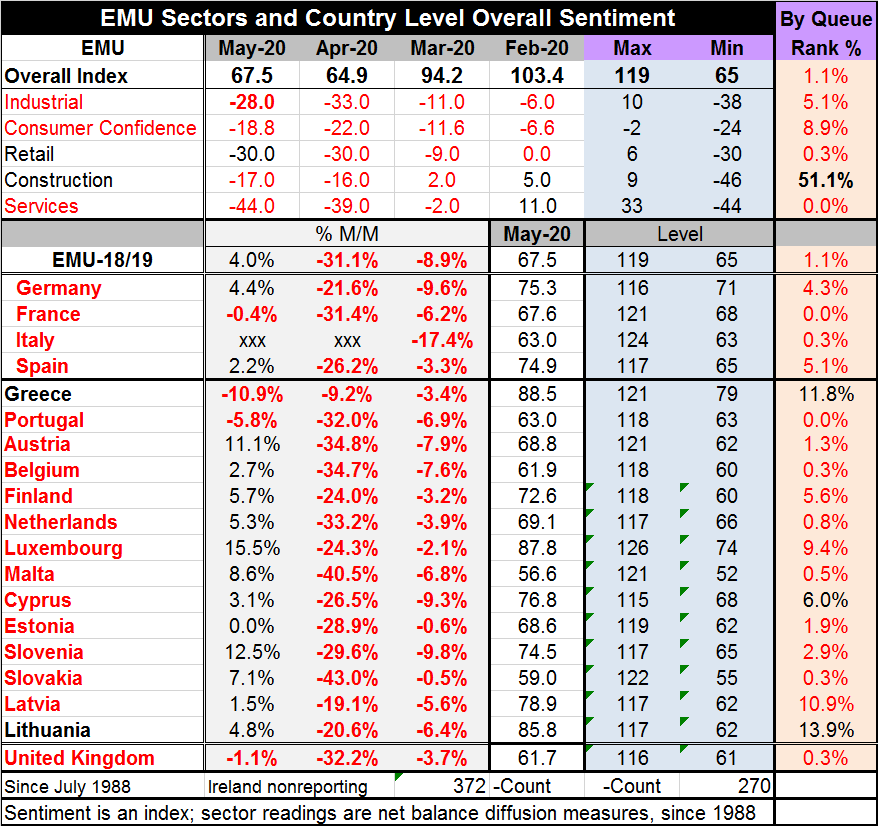

The EU Commission indexes are a common set of data across the EMU community that gives both country details and industrial-level reports to provide a good overview of what is happening. The sector reports show all sectors with a ranking of their May performance in the bottom 10th percentile of their historic queues of data, except for construction, that in May sits just above its median level.

April saw horrific declines (except Italy where the virus his so hard it suspended reporting data. Month-to-month in May, there is a bounce up and down the line with few exceptions. Greece fell hard again although it fell less than others in April. Portugal took a sizeable step lower in May despite a large drop in April. France ticked lower in May. Italy, of course, is 'off the clock' on this comparison since it did not issue a reading in April. The United Kingdom, now no longer affiliated with the EU, saw its index fall by 1.1% after a large fall in May.

Among countries the two strongest standings are for Greece and Lithuania; they are both in their bottom 15th percentile (so 'strongest' is a relative term). France and Portugal post all-time low readings this month. Italy, Belgium, Slovakia…and the U.K. are not far behind.

In separate economic reports today, there was weak inflation reported in the euro area. However, money and credit growth in the euro area are both beginning to show some life. There was a large fall in German retail sales and U.K. car production was the weakest since World War II. In Asia, Japan and South Korea both reported very weak industrial output. Brazil's economy shrank. And amid a flurry of reports from the U.S., it was reported that while personal spending fell hard in April nominal income rose smartly as transfer payments from the government dominated private sector income losses to individuals. This was a surprise. It points out how hard it is for a capitalist country to get its socialism right. In the U.S., small businesses are struggling; there are record bankruptcies pending; and State's finances are on the ropes. People are falling through the cracks between the support programs and are suffering, but the government has ponied up more than enough money to have made everyone's income whole. But some got none and others just put it in the bank. As a result, U.S. spending is down sharply and the saving rate has spurted.

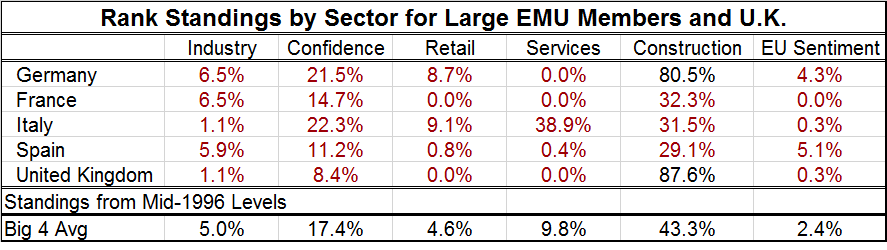

The table below summarizes EMU large countries' standings by sector along with the readings on the U.K. Retailing and industry are extremely weak everywhere. Confidence is also very weak across the board but not quite as weak as industry and retailing. Services are at their weakest everywhere except in Italy where the standing is surprisingly buoyant at its 38th percentile- a below-median reading but not as weak as anything else mentioned to-date. Construction shows more 30th percentile standing readings; those are bottom-one third standings and are clearly weak. Construction sector weakness is everywhere except in Germany and the U.K. where outright strength prevails still. And the EU Commission sentiment overall standings are very weak everywhere without exception.

The day's country-reported statistics as well as the EU industry results still give us little insight into the road ahead. There are isolated 'hot spots' of virus here and there, but mostly the virus is suppressed and being carefully watched for any signs of reemergence. Countries are lifting restrictions but doing it carefully, slowly.

In the U.S., Dallas Fed Bank President Robert Kaplan has called a bottom for the economy. Loretta Mester, Cleveland Fed Bank President, has said she can't imagine having a 'V-shaped' recovery. Europe is a step or two ahead of the U.S. in the coming out party, but the U.S. too is coming out.

In the U.S., there is a hot debate about relieving restrictions, but one poll reports that Trump's message of opening up is having resonance over Biden's. There is still a long path ahead and plenty of time/room for something to go wrong. The game of growth is on, not over.

Globally, everyone will be trying to make some progress back toward normal wondering how far they can go. Meanwhile, there will be a good watch on the rearview mirror for any pick-up and plenty of testing for virus. The global economy is on its way back. Slowly it turns inch by inch step by step… Recovery will be 'measured' which is not to say that it won't have some periods of relatively rapid recovery on its way back. But I would agree with Mester. There will be no overall 'V-shaped' recovery, but there might be pockets and periods of short-lived 'Vs' as industries and regions open up. The point here is that no one will ride a 'V-shaped curve' all the way back to normal. But there may be some V-curve riding mixed with walking and maybe even some crawling.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief