U.S. Construction: Sluggish in June

Summary

- Private building, both residential and nonresidential, drifting lower.

- Public construction hesitating after two strong years.

Total construction activity fell 0.4 percent in June, continuing a soft trend that began in the middle of last year. After peaking in May 2024, total outlays have declined 3.6%. The retreat was modest at first, but the softness began to intensify last fall. Activity has now declined in nine of the past ten months, with the drop over this span totaling 3.1%. The private sector accounts for nearly all of the softness, with both residential and nonresidential contributing; public construction has continued to advance, although gains in recent months have been modest.

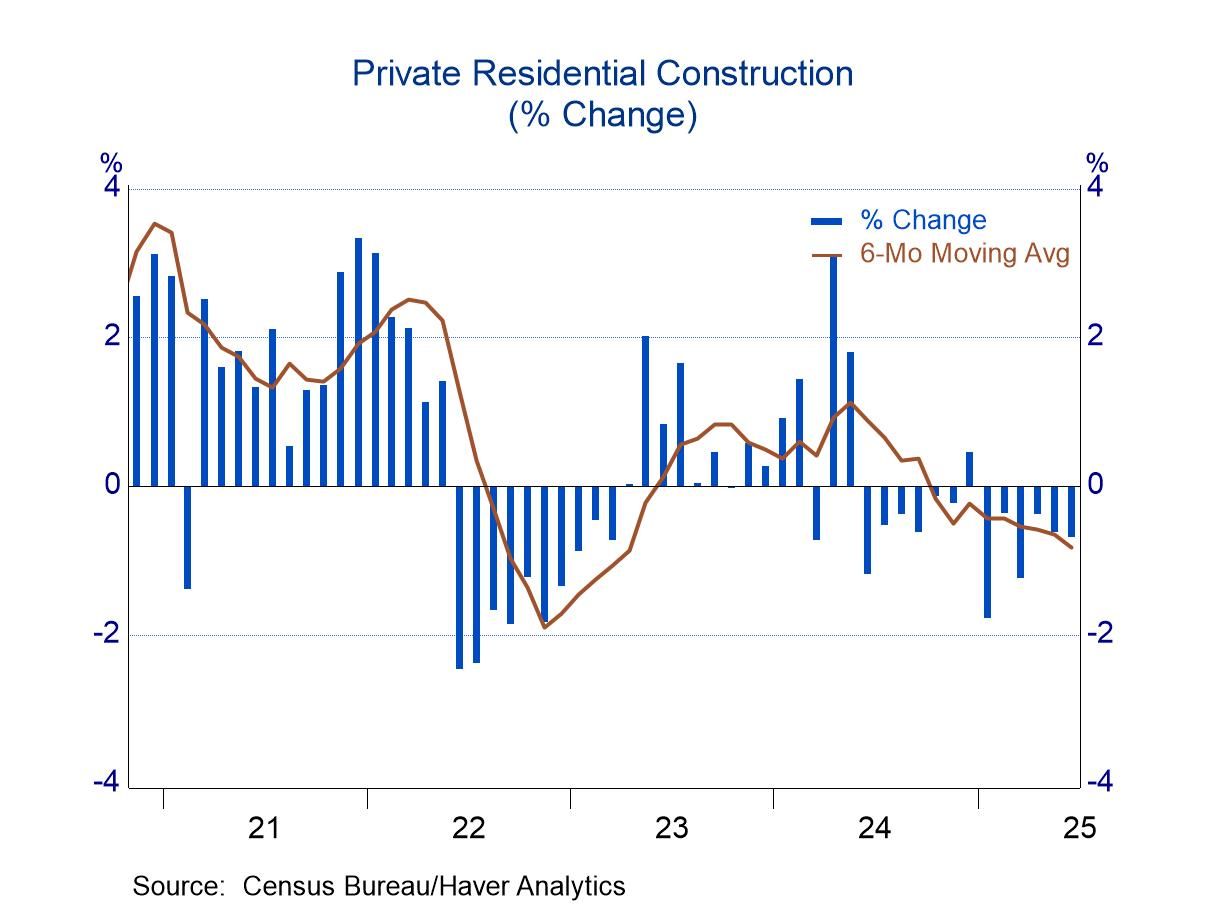

Private residential construction fell 0.7% in June, marking the 12th decline in the past 13 months and leaving activity 7.3% below the peak in May 2024. Hints of softness in private residential construction first appeared in mid-2023, when multi-family construction first stalled and then moved notably downward throughout 2024. Following the swoon in 2024, multi-family activity has stabilized in recent months.

However, single family building has taken the lead in pulling activity lower, declining for four consecutive months with pronounced retreats in the past three (average of -1.8%). Prospects for single-family construction do not seem bright, as the ups and downs in single-family housing starts have left little net growth in the past year; the past four months have been especially soft.

Improvements to existing structures contributed to weakness with sharp declines early in the year, but this area has posted small gains in the past three months. Home improvements (i.e. additions and renovations) should not be ignored in assessing residential construction, as they typically represent 35 to 40 percent of private activity.

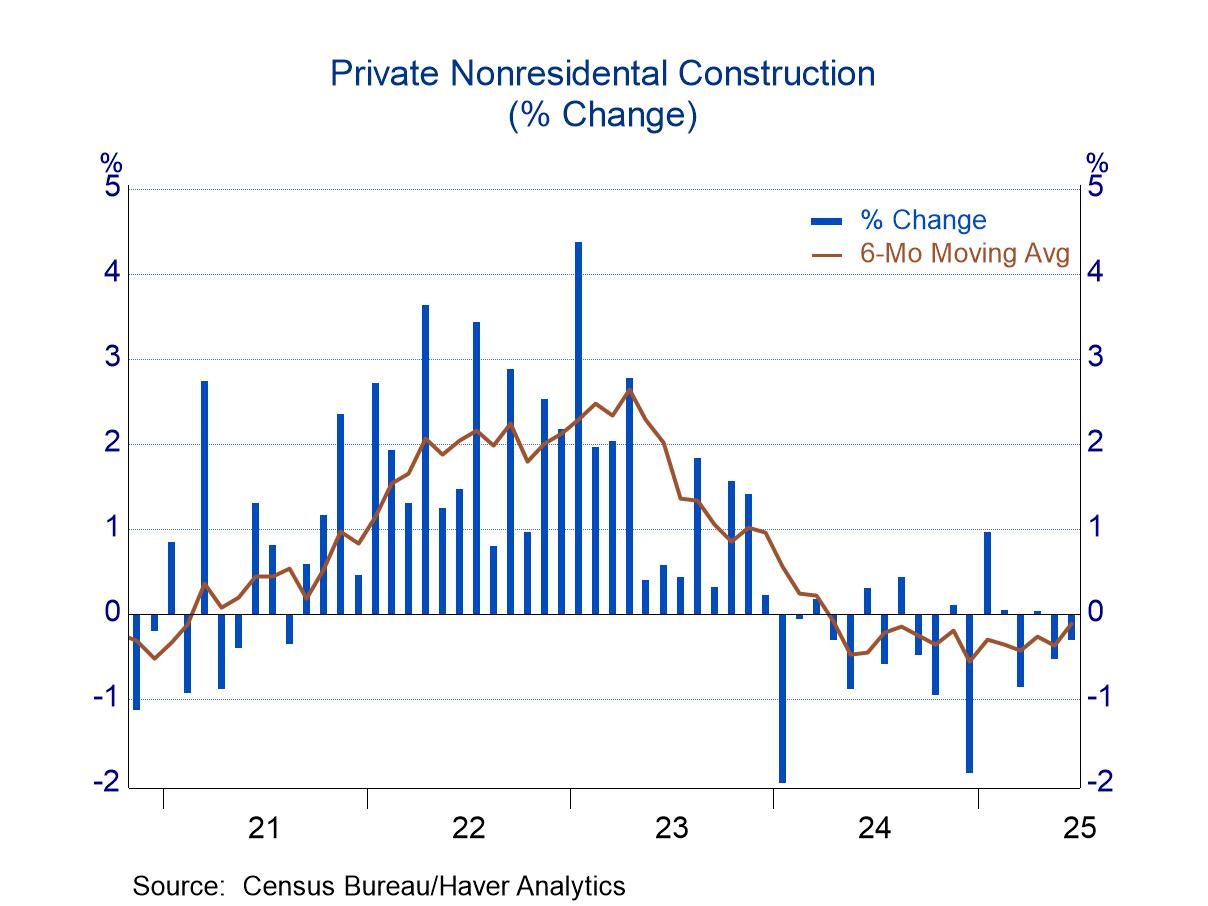

Private nonresidential construction fell 0.3 percent in June, reinforcing the downward drift that has been in place since the start of 2024. This sector has posted 11 declines in the past 18 months. While activity grew in several months over this span, most of the increases were minuscule. The net effect of the ups and downs was a drop of 6.6% (annual rate of 4.4%). Total nonresidential activity has several components, and some have advanced in the past year or so, but none has posted an impressive performance. Two areas, lodging (hotel, motels, resorts) and commercial (retail and wholesale), have been notably soft.

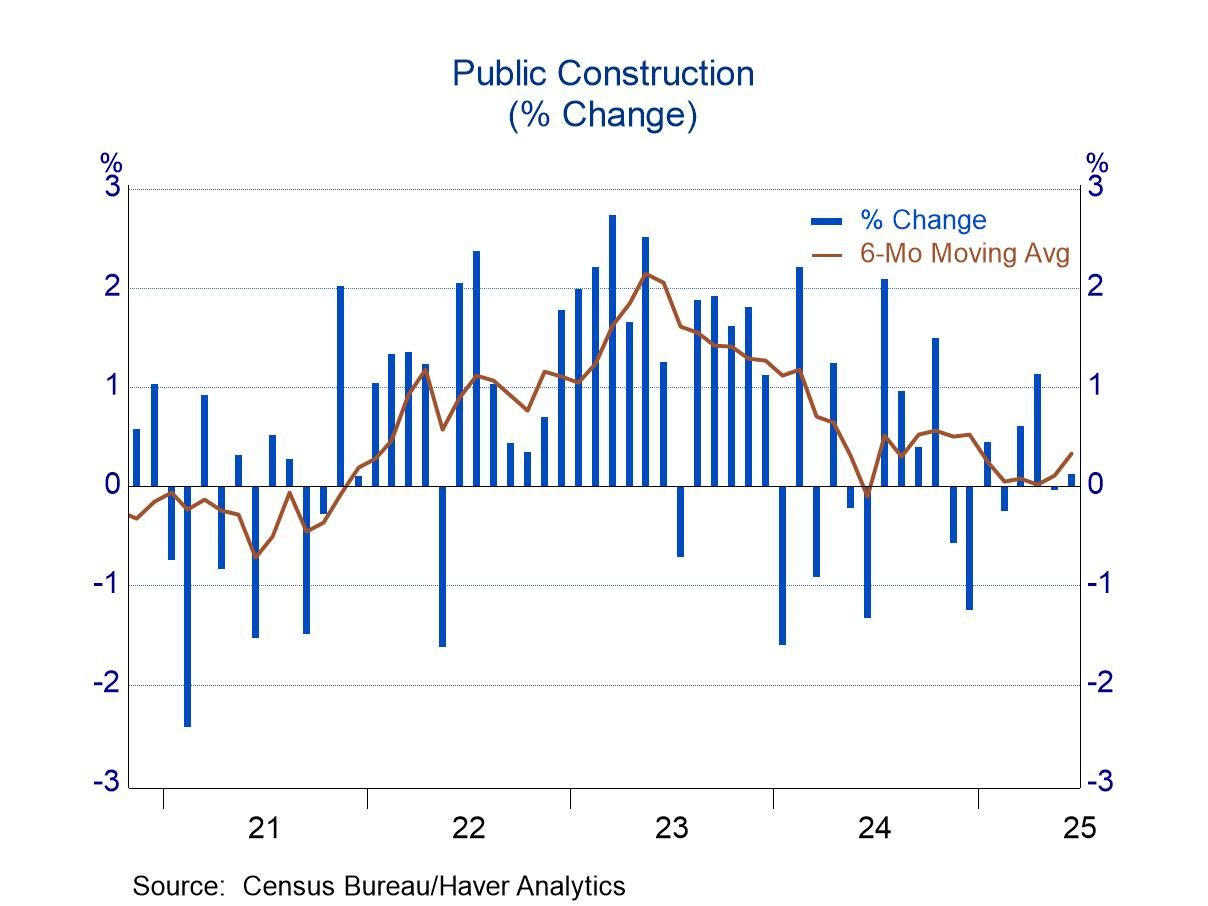

The public sector has started to sputter after two years of strong activity. Building was vigorous in 2023, growing 21.8% (December to December), and activity advanced an additional 2.4% in 2024. Growth so far this year has been modest on balance. Most months have registered gains, but they offset declines in the closing months of last year by only a small margin. Activity in June was 0.1% above the reading in October (the high point in 2024). Both state and Local governments and the federal sector have posted similar performances: robust in 2023, moderate in 2024, and hesitating this year.

The construction figures can be found in Haver's USECON database. The expectations figure is from the Action Economics Forecast Survey in AS1REPNA.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global