Global| May 23 2019

Global| May 23 2019EMU PMI Ticks Higher As Manufacturing Continues to Contract

Summary

The EMU PMI remains weak in May at 51.6, but it is a few ticks higher than its value in April. Its May value is just a tick below its three-month average, at its six-month average and below its 12-month average which does not speak [...]

The EMU PMI remains weak in May at 51.6, but it is a few ticks higher than its value in April. Its May value is just a tick below its three-month average, at its six-month average and below its 12-month average which does not speak well for momentum. Manufacturing clearly is slipping sequentially. The service sector reading for the EMU shows a slight bump up over three months compared to six months, but the May reading is below the three-month reading and at the six-month level. On balance, there are weak readings across sectors.

The EMU PMI remains weak in May at 51.6, but it is a few ticks higher than its value in April. Its May value is just a tick below its three-month average, at its six-month average and below its 12-month average which does not speak well for momentum. Manufacturing clearly is slipping sequentially. The service sector reading for the EMU shows a slight bump up over three months compared to six months, but the May reading is below the three-month reading and at the six-month level. On balance, there are weak readings across sectors.

The sector standings place the overall EMU reading in its bottom 9 percentile. Manufacturing is in its bottom 1.9 percentile and services stand in the bottom 13.2 percentile of their queue of data back to January 2015. By the standards set since January 2015, these are extreme weaknesses.

The German and French cases show significant differences but also show a lot in common. The German PMI composite readings gradually are getting weaker from 12-months to six-months then flatten out at unchanged over three months. The French composite headlines continue to weaken sequentially. The German composite reading improves across the recent three months and so do the French readings. However, German manufacturing contracts sequentially and worsens on the recent three months as well while French manufacturing weakens sequentially but continues to show some expansion and waffles over the recent three months. German service sector readings weaken then stabilize sequentially while French service readings deteriorate sequentially. Still, both French and German service sector readings show an improving trend in the recent three months.

The German queue standings show much more weakness for the overall composite compared to France as well as for manufacturing. Yet, all these reading are poor and below their respective medians. But German services are an exception with a 60th percentile standing whereas French services have a very weak 32nd percentile reading, weaker than the services sector in Germany.

It’s no wonder that the ECB continues to have concerns about the economy.

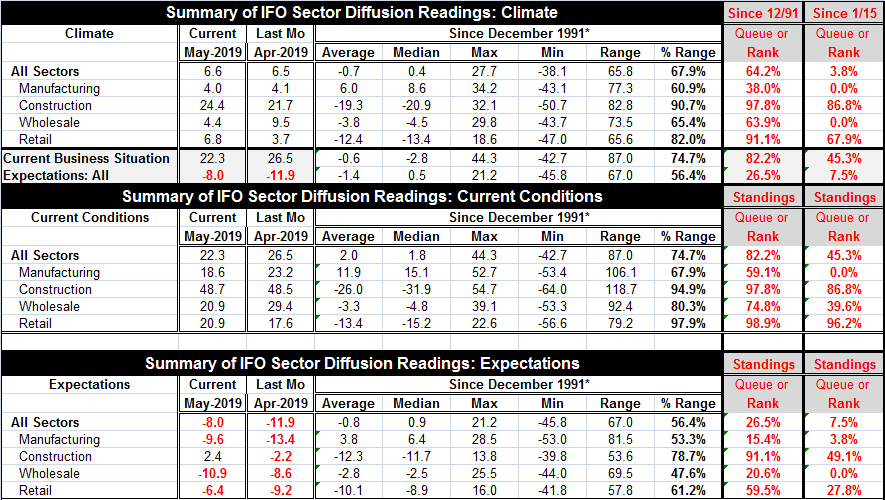

A separate survey of the German economy was released by the IFO today as well. The well-regarded German IFO survey shows weakness and readings that more or less stand up to the Markit PMI readings when judged on the same time period (January 2015 to date).

On that basis, the overall German climate reading has a 3.8 percentile standing with manufacturing at a low standing of zero percentile. That’s the same as the Markit reading. The services sector does not get a single reading in the IFO framework, but its segment readings on retail and wholesaling are comparable.

The IFO offers a composite climate reading and separately breaks out current conditions and expectations by sector. So the approach is not comparable to the Markit indexes. Still, it is clear that for Germany the two surveys are seeing the same things, the same weaknesses and the same dislocations. The current standings from IFO are slightly stronger than for Markit on service sector components; but they are just as weak as Markit for manufacturing. And the expectations reading from IFO are simply weak everywhere except for construction which IFO does not address at this time as a flash reading.

Returning to the Markit readings, beyond Europe we find sequential slippage in Japan for manufacturing from 12-months to six-months to three-months and a return in May to a reading that shows manufacturing contraction. Japan also sports a very weak 15th percentile standing for manufacturing.

The Markit readings for the U.S. are less closely watched since the ISM readings are preferred. ISM looks at manufacturing and nonmanufacturing and so has a slightly different breakdown than Markit; the ISM folds construction and mining in with services. Still, the Market readings for the U.S. have been weaker than the ISM for some time. This month the Markit readings for the U.S. have slipped again and they show both monthly and sequential deterioration. All U.S. sector readings are in the lower 6th percentile of their respective data queues or lower (since January 2015). The movement in the ISM and the Markit indexes are sometimes different so we have to take these readings for what they are.

What is clear from the market survey and the German IFO is that conditions are not improving. The deterioration in manufacturing has slowed in most places, but manufacturing remains weak and the services sector is under pressure as well. There is no sector that is trying pull things back to growth at least not yet. Most readings are subpar standing as they continue to reside below their historic median levels.

The geopolitical background continues to be a poor one with uneasiness in the Middle East and Kim Jong-un making it clear that he is not getting ready to cozy up to Joe Biden if Biden wins in the U.S. Yes, U.S. politicians running for office are making their positons known and we are getting feedback on it – clear evidence that the U.S. political situation is under scrutiny from abroad. The President, however, is still running the show. He is thinking about sending 5,000 troops to the Middle East to counter the Iran threat. China and the U.S. are deep in their trade/tech spat. And despite claiming to still be negotiating, the U.S. sent a naval vessel through the Taiwan straits angering China. Since China has grabbed the South China Sea, according to Maritime rules, in order to keep China’s claim contested ships much continue to seek and gain passage through the disputed waters.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief