Global| May 10 2019

Global| May 10 2019EMU Large Member IP Trends Align As Trade-War Clouds Gather

Summary

Among eleven of the longest term EMU members, there is always going to be some divergence. The large economy trends continue to show that they are in alignment while the broader community demonstrates some disparity and yet also seems [...]

Among eleven of the longest term EMU members, there is always going to be some divergence. The large economy trends continue to show that they are in alignment while the broader community demonstrates some disparity and yet also seems to be more or less on the same path. Just like there is ‘no crying in baseball’ in macroeconomics, there is no moving together in lockstep even for highly linked economies.

Among eleven of the longest term EMU members, there is always going to be some divergence. The large economy trends continue to show that they are in alignment while the broader community demonstrates some disparity and yet also seems to be more or less on the same path. Just like there is ‘no crying in baseball’ in macroeconomics, there is no moving together in lockstep even for highly linked economies.

Monthly behavior

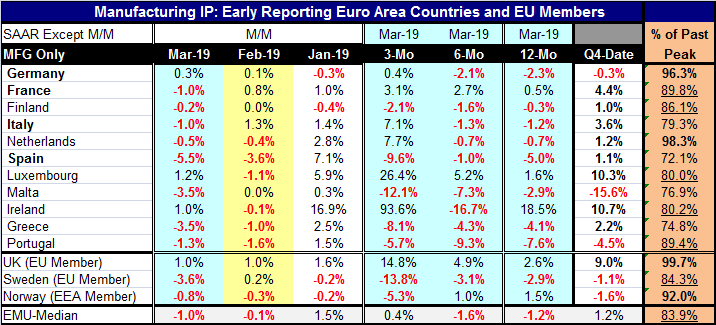

On monthly data, there is considerable divergence but also lingering weakness. Among the 11 EMU members in the table, eight show declines for output in March. Germany, Ireland and Luxembourg are the exceptions. That compares to February when output fell month-to-month in only six countries and was flat in two others with increases in three: Germany, France and Italy, the three largest EMU member economies. January showed increases in output in nine of eleven members with Germany and Finland as exceptions. These three months show the direction of change in German IP generally has been contrary to that for the bulk of EMU members.

Broader trends

Turning to the broader trends, there are only five output declines over three months for these EMU members with increases in six of them. Germany, France and Italy, the three largest economies, show IP increases over three months. Over six months, declines proliferate with nine of eleven countries showing IP drops. France and Luxembourg are the exceptions. Over a 12-month span, eight of eleven nations show IP declines with gains reported in France, Luxembourg, and Ireland. While the monthly growth rates of the large EMU economies seem somewhat out of sync, the chart shows that the recent adjustments in the path of the German, French and Italian annual growth rates have been remarkably similar. Each of these countries saw growth peak in early-2018, fall to a low at the end of 2018, then rebound and subsequently experience another setback to the year-on-year growth path. The small positive growth rate for France over 12 months does not put it out of step with Germany and Italy.

Quarter-to-date

In the quarter-to-date (which now refers to the completed first quarter of 2019), output is rising in eight of eleven countries. Germany shows an output decline but only technically since it is a small decline of 0.3% when expressed as a compounded annual rate. For the most part, IP shows resilience in Q1 2019 Q1. There is a sizeable decline of 15.6% for Malta and a drop at a 4.5% pace for Portugal.

Other Europe

The U.K., Sweden and Norway show divergence. The U.K. logs persistent output increases compared to chronic output declines for the northern Europeans.

Economic slack

On balance, there still seems to be substantial slack in European manufacturing sectors. The U.K. has the highest output when expressed as a ratio to its past cycle peak. Current U.K. output is 99.7% of its past peak as firms have created output and built stockpiles to anticipate and prepare for problems when Brexit is activated. Output in the Netherlands is 1.7% off its past peak. Output in Germany is 96.3% of its past peak. Output in Norway is only 8% off its past peak. After these four countries, seven European nations show IP in the range of 80% to less than 90% of their respective cycle peaks. Four countries show a great deal of slack with output at 70% to less than 80% of their cycle peaks. This group includes Italy, Spain, Greece and Malta.

Slack conditions are uneven

The largest economies tell an inconsistent story about economic slack as Germany’s output is 96.3 percentile of its past peak. France is 89.8% of its past peak. Italy is 79.3% of its past peak and Spain is 72.1% of its past peak. So even when output trends are more or less ‘moving together’ there are substantial differences still in play. And yet the ECB makes only one monetary policy for all of the EMU. Because of its heated industrial sector and low unemployment, Germany has been wary of inflation and its domestic inflation measure is running hot.

German exports rebound but fail to impress

Today German exports are reported to have rebounded in March. But there is still nothing impressive on the German export front. Exports are up at a 1.7% pace over three months, a deceleration from their 5.1% pace over six months. Imports have decelerated more broadly and are growing at less than a 1% annual rate over three months and six months. Real export and import trends (lagged) show more life, but it is imports that come to life after inflation adjustment not so much exports.

Slowdown with risks still lurking

On balance, IP trends are still on a path of moderation. The chart suggests that the slowdown may have been substantially accomplished, but it is too soon to be quite sure of that and in any event risks abound. Brexit is not set and neither does the U.K. have a viable or acceptable plan on the table – we can argue it does not even have a table. In the U.S., trade talks with China took a sharp turn for the worse when China decided to scrap the part of the agreement that the U.S. felt gave its recourse that made the pact enforceable. The loss of that provision caused the U.S. to impose the next layer of tariffs on China as the two parties met and talked. China is talking about getting a deal while U.S. President Trump says he is in no hurry after China’s recent backtracking. And how can China rescind crucial parts of what it had agreed to and think a deal is still at hand? If China thought it would call Trump’s bluff or if it thought Trump had been weakened by his domestic discord, it has misjudged his resolve and we will all be the worse off for it. Not surprisingly, the talks have broken up without an agreement.

EMU Area IP Trends

The path ahead

The U.S. seeks from China a deal that that is fair as well as enforceable. The U.S. seeks to put a stop to China’s unfair technology expropriation practices. I hear some blame Trump because he did not give China chance to save face. How do you let it save face when it won’t agree to enforcement and has never been trustable and has flaunted international law? Other countries are watching this deal closely as China has also thrust its reach broadly with an export drive called its Belt and Road program.

Below the belt?

The Belt and Road program was structured to heap insurmountable debt on developing economics and then seize their infrastructure for China. President Xi now claims that the Belt and Road effort will not continue to proceed like that. In truth, there is a lot of bad will that China has created on this and other projects. It’s seizure of the South China Sea is only the one of the most glaring examples. Its 99-year lease on the port in Sri Lanka that China took to let Sri Lank ‘pay’ for the excessive debt incurred when China’s Belt and Road infrastructure ‘help’ became unaffordable is another example. Yet, another is the crumbling nuclear reactor China built in Ecuador that is being paid for with Ecuador’s oil revenue but does not work. When you shake hands with China, be sure to check that all your fingers are still there when you ‘reclaim’ your hand. The U.S. is mindful of all this and so has no appetite to meet China ‘half way’ as China now ‘requests’ and takes back the enforceable part of the trade deal. Why would anyone meet them half way on that? Enforcement is binary. Either you have it or you don’t. Halfway to nowhere is nowhere. We can see that global trade and growth prospects will remain up in the air and pressured for some time to come. It is hard to say how much U.S. tariffs and China’s retaliation will impact global growth. But it sure won’t help.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief