Global| Jan 17 2007

Global| Jan 17 2007December Industrial Output Gained, But Vigor Questionable with Downward Revisions

by:Tom Moeller

|in:Economy in Brief

Summary

Total U.S. industrial production rose 0.4% last month but revisions generally had the effect of lowering the gains in output during the prior two months. Consensus expectations had been for a 0.1% December rise. Factory sector output [...]

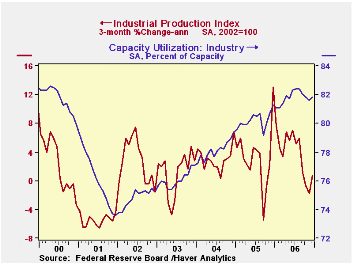

Total U.S. industrial production rose 0.4% last month but revisions generally had the effect of lowering the gains in output during the prior two months. Consensus expectations had been for a 0.1% December rise.

Factory sector output rose 0.7% but a November's 0.3% increase was revised to zero. Even so, the strong December brought manufacturing back to within a hairbreadth of its August high.

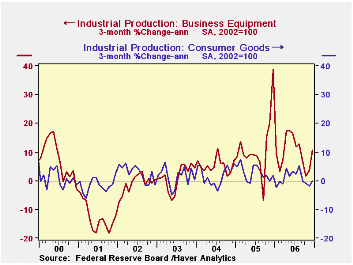

With a 1.5% (0.1% y/y) increase, production of durable consumer goods added to a slightly revised 1.6% gain in November, recovering further from its October plunge, which was revised lower still to a 2.3% fall. Both automotive products and home electronics had December increases of around 2%.

Nondurable consumer goods output slipped 0.2% (0.8% y/y) a second consecutive monthly decline. November was revised from a 0.1% decrease to -0.4%. Food and energy goods both fell, the former by 0.3% and the latter, 0.8%. Clothing had a nice rebound of 1.4% to partially offset.

Business equipment production jumped 1.6% but both November and October were reduced, November to 0.9% from 1.2% reported before and October, registered a month ago at +0.2%, was trimmed to 0.1%. Output of all major types of equipment -- transit, information processing and industrial -- showed sizable December gains, but the downward revisions, which were the second in a row, leave us a bit cautious about characterizing the overall trend as a vigorous one.

Total industry capacity utilization increased to 81.8% in December from 81.6% in November. This latter period was, however, revised from an initial 81.8% reported last month. Factory sector utilization increased to 80.2% from downwardly revised 79.8% in November and 79.9% in October, both somewhat lower than reported a month ago. Factory sector capacity again rose 0.2%; November's 2.8% y/y gain represents a slight upward revision, but December's yearly increase in capacity eased to 2.7%.

| Production & Capacity | December | November | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Industrial Production | 0.4% | -0.1% | 3.0% | 4.1% | 3.2% | 2.5% |

| Manufacturing (NAICS) | 0.7% | 0.0% | 3.5% | 5.0% | 4.0% | 3.0% |

| Consumer Goods | 0.2% | 0.1% | 0.6% | 1.3% | 2.8% | 1.4% |

| Business Equipment | 1.6% | 0.9% | 10.4% | 11.7% | 7.9% | 4.3% |

| Capacity Utilization | 81.8% | 81.6% | 81.3% (12/05) | 81.8 | 80.2% | 78.1% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief