Global| Nov 10 2006

Global| Nov 10 2006Credit Standards Eased as Demand Fell

by:Tom Moeller

|in:Economy in Brief

Summary

In the 4Q Senior Loan Officer Survey on Bank Lending Practices, the Federal Reserve Board indicated that credit standards for large firms were unchanged during the last three months. That represented a sharp easing of lending [...]

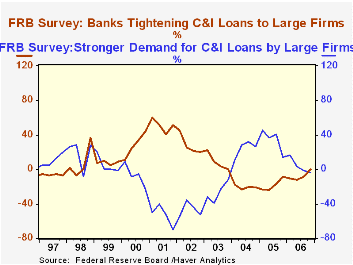

In the 4Q Senior Loan Officer Survey on Bank Lending Practices, the Federal Reserve Board indicated that credit standards for large firms were unchanged during the last three months. That represented a sharp easing of lending conditions relative to the stringency of one year ago.

The easing came as the strength in the demand for C&I loans waned substantially. Amongst large firms, 14.5% reported stronger loan demand but 18.2% reported either a moderately or substantially weaker call for credit. The net -3.7% was the weakest in three years.

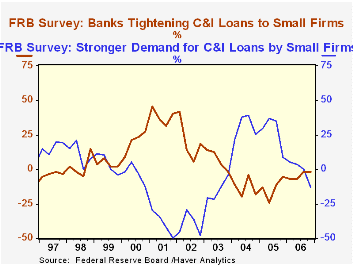

Amongst small firms, bank lending standards similarly eased to the least stringent in three years. However, loan demand here too fell sharply. In fact, the collapse to a net -13.0% reporting stronger demand reflected nearly one quarter of banks reporting at least moderately weaker demand.

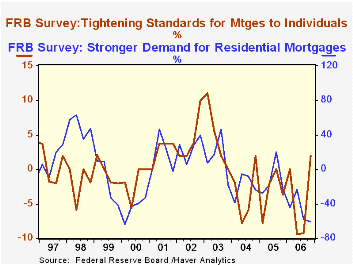

For individuals, loan demand for mortgages virtually dried up. The net -60.4% of banks reporting either moderately or substantially weaker mortgage loan demand was the worst since during the recession year of 2000. In contrast to the situation for businesses, the tightening of lending standards for mortgage loans to individuals was to the most stringent since 2004 and was in marked contrast to 3Q06 when standards were near the easiest since 1993.

Banks' willingness to lend to consumers also dried up. The net 1.9% of banks still willing to lend to consumers was the lowest since early 2003.

Some worry about M&A related loan activity was reflected in a net 26.9% of banks expecting loan quality to deteriorate either somewhat or substantially over the next twelve months. There were no banks that expected loan quality to improve. For loans unrelated to M&A activity, there was a similarly negligible 1.9% of banks that expected loan quality to improve at least somewhat and 36.5% expected at least some deterioration.

The figures behind the Fed survey of lending practices can be found in the Haver SURVEYS database.

The October 2006 Senior Loan Officer Opinion Survey on Bank Lending Practices from the Federal Reserve Board is available here.

Monetary Aggregates and Monetary Policy at the Federal Reserve: A Historical Perspective, today's speech by Fed Chairman Ben S. Bernanke can be found here.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief