Global| Apr 19 2019

Global| Apr 19 2019Confidence, Italian Style, Erodes a Bit

Summary

Consumer and business confidence peaked in the mature portion of this cycle about 1.5 years ago. As the graphic shows, consumer and business confidence are not always embedded in the same cycle. But the big swings in each series [...]

Consumer and business confidence peaked in the mature portion of this cycle about 1.5 years ago. As the graphic shows, consumer and business confidence are not always embedded in the same cycle. But the big swings in each series usually have some mutual correspondence. Right now both are transitioning lower.

Consumer and business confidence peaked in the mature portion of this cycle about 1.5 years ago. As the graphic shows, consumer and business confidence are not always embedded in the same cycle. But the big swings in each series usually have some mutual correspondence. Right now both are transitioning lower.

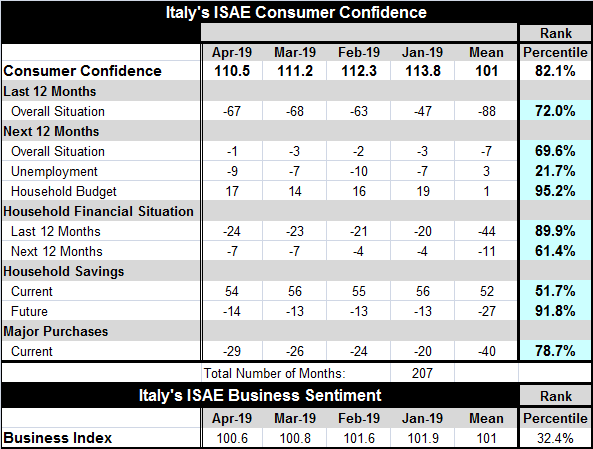

The overall situation over the past 12 months has a 72nd percentile standing, but it has slipped sharply from its January level. The overall situation for the next 12 months has a similar 69th percentile standing, but it has improved significantly since January. Unemployment prospects have become more remote and now they have a 21st percentile standing, putting fear of unemployment near the lower one-fifth of its historic set of readings. Meanwhile, the state of the household budget has improved. The measure fell off directly after January and has since recovered much of its loss; it has been better less 5% of the time since 1990.

The household financial situation over the last 12 months has an 89th percentile standing, but that is sharply lower as households look ahead to the next 12 months where the standing falls to its 61st percentile.

Households savings are currently in their 51st percentile. The future the ability to save rises sharply to a 91st percentile standing. Future prospects also have improved significantly since January. The environment for making a major purchase stands in its 78th percentile and has made significant improvement since January.

Taking the two series back to 1990, the consumer index has the relatively stronger standing at the moment as it stands in the 82nd percentile of this broad historic gauge compared to a 32nd percentile standing (lower one-third) for business climate.

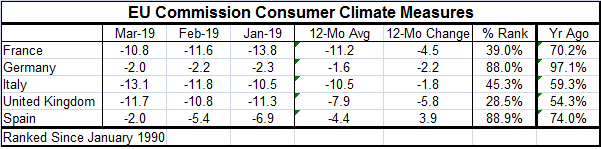

Among the five largest EU economies (yes, as of this writing, the U.K. is still an EU member), Italy has the third highest rank standing for consumer climate according to the EU Commission readings (updated through March) although Italy clearly groups more with the weaker members than with the stronger ones. Spain and Germany have the highest relative rankings on this gauge with readings in their respective upper 80th percentiles. Italy stands at its 45th percentile with France at its 39th percentile and the U.K. suffering Brexit fever at a 28th percentile standing.

All of these gauges have weakened over the past year except for Spain where its rank standing has improved from the 74th percentile to the 88th percentile, a substantial move higher. France, weathering its ‘yellow-vest’ protests, has seen the sharpest erosion as its percentile standing has fallen by 31 points in the past 12 months. That is even more than the 25 percentile points dropped by the U.K. as a Brexit deal has proved more elusive than a Leprechaun hiding his pot of gold. Climate in Italy has fallen by 14 percentile standing points over the past 12 months while Germany has shed only nine points.

Italy in Context

On balance, we see that Italy has showed some resilience; it even shows some optimism if we compare the standings for expected future conditions to past conditions. That is impressive because the past shows a good deal of deterioration in train and this forward-looking improvement implies that the economy is not expected to continue to deteriorate.

At the time of the IMF meeting- just concluded- participants were cutting forecasts and battening down the hatches as the IMF was pushing for countries with room to engage in stimulus to do so. This appeal, mostly to Germany, was rebuffed. But over the past week, there has been some somewhat improved data as U.S. consumer spending was a pleasant surprise and as spending in the U.K. firmed beyond expectations. The PMI gauges for Europe were hardly strong, but the downward pressure on them seemed to abate- although they continue to sport extremely weak readings. Italy has long had stronger confidence readings than economic readings and that is especially true now even with Italy as the only EMU member actually in a recession (at least on the dumbed-down two negative quarters in a row rule applied to GDP growth). Politically, the Italians are still pushing to form a more powerful protest voice in EU against the current migrant policies. Maybe, it will find an ally in Finland where elections saw the anti-immigration party nearly gain outright power. Any way you slice it, European politics are getting more interesting and that means less stable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief