Global| Nov 12 2007

Global| Nov 12 2007Commodity Prices: Oil Up, Most Other Inflation Forces Topped

by:Tom Moeller

|in:Economy in Brief

Summary

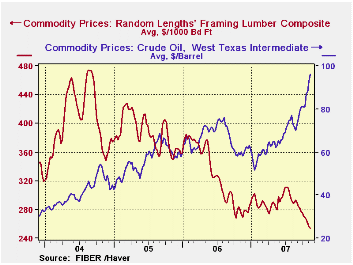

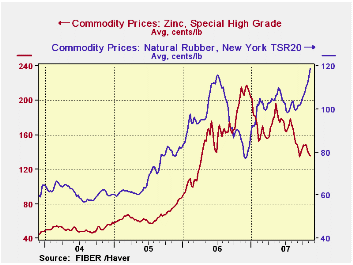

The headline commodity price worry is the rise in oil and energy prices: 57.2% for WTI and 28.7% for gasoline since the beginning of the year. And gasoline prices look to be headed higher while rubber prices have soared 62.8% this [...]

The headline commodity price worry is the rise in oil and energy prices: 57.2% for WTI and 28.7% for gasoline since the beginning of the year. And gasoline prices look to be headed higher while rubber prices have soared 62.8% this year.

With any luck, however, that isn't the whole story. There seem to be other factors which will mitigate the effect that these gains will have on overall consumer price inflation.

The first is that factory sector pricing depends both on overall demand growth, which is easing, and the overall rise in costs of which commodity prices account for 25% or less. The other 75% is labor costs, and the employment cost index for factory workers is up 1.2% so far this year versus a 1.8% gain last year, a 3.4% rise in 2005 and a 4.8% rise during 2004.

The second is that for the economy overall, the dependence on oil is roughly half what it was in the early 1970s due to conservation and improved efficiencies in production techniques. And, in total, U.S. demand growth has slowed as well as the growth in the Fed's monetization of that growth. Year to year growth in the monetary base through October was 2.5% versus a 3.9% rise last year and a 4.3% 2005 increase.

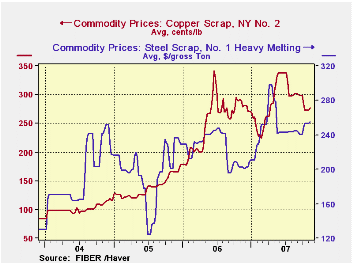

Finally, other commodity prices have topped or have been declining. The housing market's weakness has dropped lumber prices 5% so far this year after a 15% decline last year, and a 4% decline in 2004. In addition, steel scrap prices have been roughly flat this year after strong gains in years prior. Zinc prices are 31% lower so far this year and have retraced most of a strong gain at the end of 2006. Similarly, aluminum prices have fallen 12% this year and have retraced the strong gains during the latter part of 2006.

In conclusion, inflation worries have affected the consumer's psychology greatly. The worries have been enough to drop consumer sentiment by nearly one quarter since the highs early this year. This would seem to guarantee some near term slowing in consumer spending. The mitigating factors sighted above, with that luck, will prevent a protracted decline.

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.