Global| Apr 23 2008

Global| Apr 23 2008Belgian National Bank Index Signals Euro-Trouble Ahead

Summary

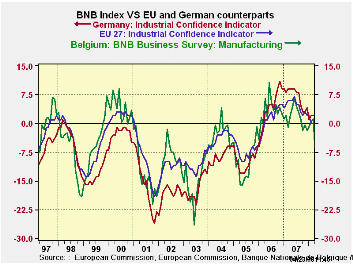

BNB index is a harbinger for the Euro-Area: The BNB index has plunged sharply in April. This early read on Euro Area health in April has been a GOOD SOLID barometer of what the larger and geographically linked key EMU economies will [...]

BNB index is a harbinger for the Euro-Area: The BNB index has

plunged sharply in April. This early read on Euro Area health in April

has been a GOOD SOLID barometer of what the larger and geographically

linked key EMU economies will report for the month. The chart shows the

tracking of the Belgian industrial index – usually the first read on

the Euro Area and EU in any given month - with the EU’s industrial

index and with the EU Commission index for Germany. The Belgian index

has often moved ahead of the EU and German indices. In this episode,

the Belgian index had started to strengthen ahead of any such signs for

Germany and EU before posting this recent drop. So the plunge in

Belgium in April may overstate the extent of the drop yet to be seen in

Germany and in EU. In any event, the smaller Belgian economy often sees

its BNB index move more sharply than the indices for Germany and the EU

but it is generally a good ‘hint’ for them and is not to be ignored.

MFG sector is weak

The BNB index shows us widespread weakness in Belgium. The MFG index

(an up minus down net reading, like all the other components) is at

-7.9, the weakest since it was at -10.5 in August of 2005. The domestic

production reading slipped from +6 to +2 in April but the domestic and

foreign orders indices have both plunged to register deep negative

readings. Foreign orders were last weaker in May of 2005 and domestic

orders were last weaker in June of 2003.

They’re here – not the poltergeist but worse… FX gremlins

The current assessment, by comparison, is only mildly negative at a -2

reading, and was last weaker in January of 2008 at -5: so that’s no big

deal- or is it? Foreign orders at a -8 are more serious weakened in the

current assessment, suggesting that foreign-linked weakness is here now

and not just in some vague pipeline of indeterminate length. This is

the sort of thing we have been waiting to see happen in the aftermath

of the ongoing surge in the euro. Maybe the Euro Area is not so

resilient after all. Maybe the German economy is not as ‘robust’ as its

deputy Finance minister sees things. Maybe the ECB has lost its cool in

pursuit of an inflation objective that made no SHORT TERM SENSE given

the nature of the international strains in the system. Maybe, maybe,

maybe- a great word that word ‘maybe.’

Weakness across Belgium a geographically central-EU state

Apart from industry the Belgian wholesale/retail index fell sharply to

-9.5 in April from +0.2 in March. It had briefing resided at -8 in

February of this year and then recovered - but no more. It was last

weaker in May of 2005 at -8.7. The construction index is very weak as

well. It was last weaker in Sept of 2002. The business services index

at 6.3 was last weaker in August of 2005. And so on…

Raven-mad?

Those lows in 2005 mark the time when the Euro Area was beginning to

recover from its period of extended weakness. What we see is the new

lows in the various components of the April 2008 Belgian survey go back

to OR BEYOND that point, inviting comparisons with a time when things

were bad and terms like euro-sclerosis were in vogue. The ‘New Europe’

where ‘robust’ and ‘solid’ and ‘inflation-fighting’ have been key words

and phrases may now be past their vintage years. The euro consumer

never did kick in as force to support growth. Investment-led growth can

only take you so far especially when the rest of the world is slowing

and external demand for investment goods begins to dry up…and your

currency is setting record highs while your central bank with inflation

marginally over the target starts threatening to HIKE RATES! For a time

Euro Area growth seemed to be able to out-run the speeding bullet that

was the streaking strong euro. But as Edgar Alan Poe once

wrote…nevermore. The basis for the belief was flawed from the start,

even raven-mad. Exchange rates do matter. Maybe (oh, that word again…)

now the ECB can let its policy pay some heed to that.

| Belgium National Bank Indices | ||||||

|---|---|---|---|---|---|---|

| Apr-08 | Mar-08 | Feb-08 | 3-Mo Change | 6-Mo Change | 12-Mo Change | |

| Total Industry | -7.9 | 1.2 | 0.2 | -7.1 | -7.8 | -11.7 |

| MFG | -7.4 | 1.1 | 0.5 | -6.6 | -5.6 | -9.7 |

| Production | 2.0 | 6.0 | 3.0 | 2.0 | 3.0 | 1.0 |

| Domestic Orders | -22.0 | 1.0 | 0.0 | -19.0 | -19.0 | -28.0 |

| Foreign Orders | -14.0 | 1.0 | 6.0 | -18.0 | -17.0 | -18.0 |

| Prices | 8.0 | 7.0 | 15.0 | 5.0 | 5.0 | 1.0 |

| Current assess | ||||||

| Total Orders | -2.0 | -1.0 | 3.0 | 3.0 | 4.0 | -5.0 |

| Foreign Orders | -8.0 | 4.0 | 0.0 | -6.0 | -3.0 | -11.0 |

| Inventories | 5.0 | 3.0 | 4.0 | 1.0 | 3.0 | 0.0 |

| Wholesale & Retail | -9.5 | 0.2 | -8.0 | -6.8 | -16.2 | -19.8 |

| Construction | -8.7 | 2.9 | 7.0 | -10.1 | -9.7 | -12.7 |

| Business Services | 6.3 | 6.4 | 7.5 | -0.8 | -6.5 | -7.2 |

| Comparisons: | Changes lag one month | |||||

| EU Index: Industry | #N/A | 0.0 | 0.0 | -2.0 | -3.0 | -6.0 |

| Germany Index: Industry | #N/A | 2.0 | 2.0 | -2.0 | -1.0 | -7.0 |

| Compare: BNB Index | 3.1 | -0.2 | -0.2 | |||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief