Global| Nov 05 2009

Global| Nov 05 20093Q U.S. Worker Productivity Surges -- Strongest Since 2003

by:Tom Moeller

|in:Economy in Brief

Summary

The U.S. labor market is clearly signaling that the recession is over. The magnitude of the 9.5% jump in nonfarm worker productivity during 3Q'09 wasn't unprecedented for this early in a recovery. Its size is noteworthy because the [...]

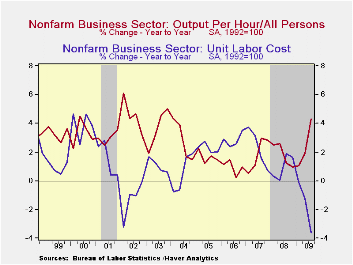

The U.S. labor market is clearly signaling that the recession is over. The magnitude of the 9.5% jump in nonfarm worker productivity during 3Q'09 wasn't unprecedented for this early in a recovery. Its size is noteworthy because the rise in output was moderate. The 3Q gain in productivity followed a similarly firm 6.9% 2Q rise which was little-revised. It was the strongest since 3Q'03 and outpaced Consensus expectations for a 6.4% increase.

The gain in productivity occurred as output posted its first

increase in over a year. The moderate 4.0% rise was accompanied by a

continuation of the sharp decline in hours-worked (employment times

hours), which has been so much a part of this recession. The 5.0%

(-7.5% y/y) decline in hours-worked followed a 7.5% 2Q drop.

The gain in productivity occurred as output posted its first

increase in over a year. The moderate 4.0% rise was accompanied by a

continuation of the sharp decline in hours-worked (employment times

hours), which has been so much a part of this recession. The 5.0%

(-7.5% y/y) decline in hours-worked followed a 7.5% 2Q drop.

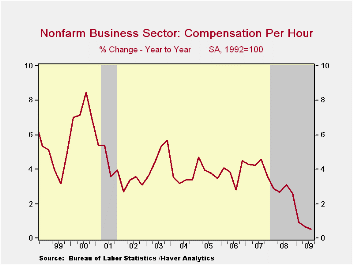

Compensation costs, however, improved with the gain in output per hour. The 3.8% quarterly increase was the first gain in a year though it left costs up just 0.5% y/y. That gain was nearly the weakest since 1949.

The surge in productivity combined with a moderate increase in

compensation combined to further drop unit labor costs. The 5.2% q/q

decline was the third consecutive quarterly fall and it lowered the y/y

change to -3.6%, the sharpest since early-1950.

The surge in productivity combined with a moderate increase in

compensation combined to further drop unit labor costs. The 5.2% q/q

decline was the third consecutive quarterly fall and it lowered the y/y

change to -3.6%, the sharpest since early-1950.

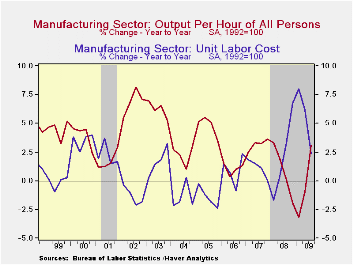

Surging worker productivity growth in the factory sector led the overall gain in output-per-hour. The 13.6% (AR) quarterly increase was a record and it lifted y/y growth to 3.1%, the highest since early last year. The increase came as output rose at a 7.7% rate (-10.8% y/y) and hours worked fell at a 5.2% rate (-13.5% y/y). Compensation rose 5.5% (5.5% y/y), therefore unit labor costs in the factory sector fell at a 7.1% annual rate (+2.3% y/y).

The productivity & cost figures are available in Haver's USECON database.

| Nonfarm Business Sector (SAAR, %) | 3Q '09 | 2Q '09 | 1Q '08 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Output per Hour | 9.5 | 6.9 | 0.3 | 4.3 | 1.8 | 1.9 | 0.9 |

| Compensation per Hour | 3.8 | 0.3 | -4.7 | 0.5 | 2.8 | 4.2 | 3.8 |

| Unit Labor Costs | -5.2 | -6.1 | -5.0 | -3.6 | 1.0 | 2.3 | 2.8 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief