- CFNAI up to -0.02 in June, remaining negative for the third time in four months.

- One of four CFNAI components down m/m; two make negative contributions.

- CFNAI-MA3 slightly up to -0.05, third negative reading in four mths.; above -0.70 (recession signal).

- CFNAI Diffusion Index down to -0.03, lowest since February.

Introducing

Winnie Tapasanun

in:Our Authors

Winnie Tapasanun has been working for Haver Analytics since 2013. She has 20+ years of working in the financial services industry. As Vice President and Economic Analyst at Globicus International, Inc., a New York-based company specializing in macroeconomics and financial markets, Winnie oversaw the company’s business operations, managed financial and economic data, and wrote daily reports on macroeconomics and financial markets. Prior to working at Globicus, she was Investment Promotion Officer at the New York Office of the Thailand Board of Investment (BOI) where she wrote monthly reports on the U.S. economic outlook, wrote reports on the outlook of key U.S. industries, and assisted investors on doing business and investment in Thailand. Prior to joining the BOI, she was Adjunct Professor teaching International Political Economy/International Relations at the City College of New York. Prior to her teaching experience at the CCNY, Winnie successfully completed internships at the United Nations. Winnie holds an MA Degree from Long Island University, New York. She also did graduate studies at Columbia University in the City of New York and doctoral requirements at the Graduate Center of the City University of New York. Her areas of specialization are international political economy, macroeconomics, financial markets, political economy, international relations, and business development/business strategy. Her regional specialization includes, but not limited to, Southeast Asia and East Asia. Winnie is bilingual in English and Thai with competency in French. She loves to travel (~30 countries) to better understand each country’s unique economy, fascinating culture and people as well as the global economy as a whole.

Publications by Winnie Tapasanun

- June IP +0.1% (+1.1% y/y), fourth m/m increase in five months.

- Manufacturing unchanged (+1.1% y/y), w/ durables -0.1% and nondurables +0.2%.

- Selected high-tech +0.5%, eighth gain in nine mths.; motor vehicles +0.7%, sixth rise in seven mths.

- Mining +0.4% (+2.4% y/y), third consecutive m/m increase.

- Utilities +0.4% (+0.3% y/y), led by a 0.9% rebound in electric utilities output.

- Key categories in market groups post mixed results.

- Capacity utilization steady at 76.1%; mfg. capacity utilization marginally down to 75.7%.

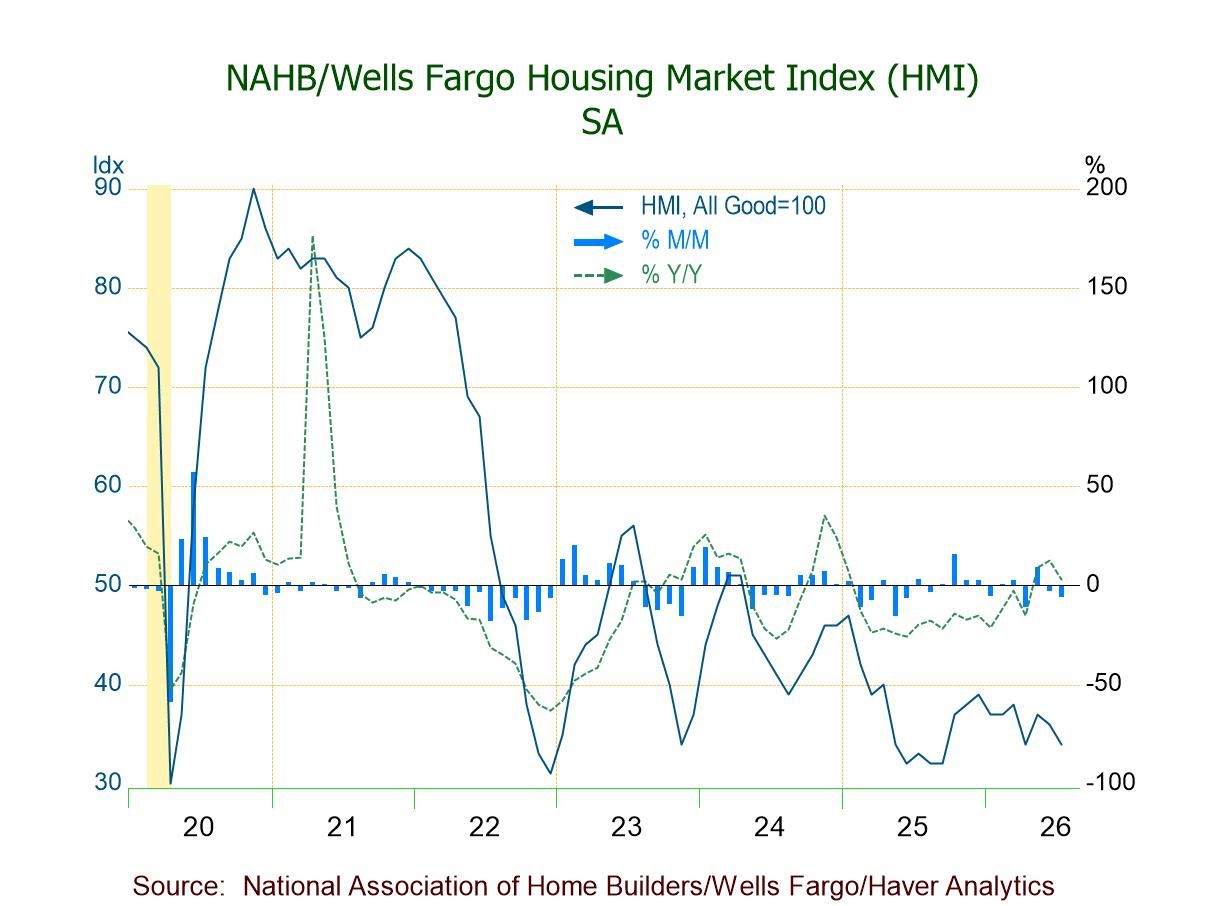

- HMI weakens m/m in July, indicating most builders remain pessimistic about the current and near-term housing outlook.

- All three HMI components down, w/ the steepest m/m drop in prospective buyer traffic (-8.0%).

- Mixed regional performance m/m: down in the Northeast (-18.0%) and West (-7.4%); up in the Midwest (+2.2%); flat in the South.

USA| Jul 15 2026

USA| Jul 15 2026U.S. Empire State Manufacturing Index Rebounds Strongly in July

- General Business Conditions Index up 9.9 pts. to 15.6 in July; fourth straight expansion.

- Shipments (24.4), highest since Apr. ’22; new orders (22.2); unfilled orders (5.0); inventories (4.0).

- Employment (11.4), a solid reading and highest since Dec. ’22.

- Prices paid (52.3) and prices received (27.6) both at three-month lows.

- Firms fairly optimistic: Future Business Conditions Index down to a still-positive 27.9; future prices paid at a four-month-low 53.0.

- Uncertainty Idx down 2 pts. to 89, remaining well above the historical avg. of 68.

- Expectations for economy up 10 pts. to 13%, a four-month high.

- Expected real sales up 8 pts. to 9%, a five-month high.

- Plans to expand business up 1 pt. to 8%, highest in three mths.

- Firms raising avg. selling prices up 2 pts. to 38%, highest since Feb. ’23.

- Top three business concerns: inflation (21%), taxes (19%), and labor quality (19%).

- June sales -2.4% m/m to 4.09 mil., first drop in three mths.; +2.8% y/y, third straight y/y rise.

- Sales m/m down in the South (-3.6%), Midwest (-3.0%), and West (-1.3%); up in the Northeast (+2.1%).

- Sales y/y up in all regions except the Northeast w/ a flat reading.

- Median sales price +2.2% (+1.8% y/y) to $440,600, a record high.

- Unsold inventory -0.6% (+1.3% y/y) to 1.56 mil. units, first m/m decline since Dec.; 4.6 months' supply, highest since Aug. ’25.

USA| Jul 06 2026

USA| Jul 06 2026U.S. ISM Services PMI Eases in June, Still Indicating Expansion for the 24th Straight Month

- ISM Services PMI down to 54.0 in June, remaining above the 12-month avg. of 53.1.

- Business Activity (55.4) expands for the 24th consecutive mth.; New Orders (55.1) for the 13th straight mth.; Employment (51.2, first expansion since Feb.); Supplier Deliveries (54.4 vs. 55.2).

- Prices Index (67.7) at a four-month low, still indicating prices rising since June ’17.

USA| Jul 01 2026

USA| Jul 01 2026U.S. ISM Manufacturing PMI Still Expansionary in June; New Orders and Production Growing at a Slower Pace; Employment Contracting

- ISM Mfg. PMI down slightly to 53.3 in June; sixth straight month above 50.

- Production (52.2) expands for the eighth consecutive mth.; new orders (56.0) for the sixth successive mth.

- Employment (49.7) contracts for the 33rd straight mth.; at the slowest contraction pace since Jan. ’25.

- Prices Index (73.0) at a four-month low, still indicating prices rising for the 21st consecutive mth.

- Exports (48.5) contract for the third time in four mths.; imports (52.9) continue to grow.

USA| Jun 30 2026

USA| Jun 30 2026U.S. Consumer Confidence Rebounds in June from a Four-Month Low

- Headline up 0.6 pts. to 91.2 in June, below expectations; fourth m/m increase in five mths.

- Present Situation Index down 3.0 pts. to 116.4, lowest since Feb. ’21.

- Expectations Index up 3.0 pts. to 74.4, a six-month high.

- Consumers less optimistic about current business & labor market conditions; more upbeat about future business & financial conditions.

- Inflation expectations down to 6.0%, lowest since Feb., as lower oil prices in recent weeks eased consumer inflation fears.

- Deficit: $105.75 bil. in May, up $22.75 bil. (+27.4%) from April’s $83.01 bil.

- Exports -5.4%, first m/m decline since Dec., led by a 9.2% drop in nonauto consumer goods exports.

- Imports +3.6%, fourth straight m/m rise to highest level since Mar. ’25, driven by an 11.5% gain in imports of other goods.

- May headline orders -4.5% m/m, first fall in three mths.; -3.5% y/y, first negative reading since Dec. ’24.

- Nondefense aircraft & parts -51.8% m/m vs. April’s +167.4%.

- Transportation orders -14.0%, first m/m drop since Feb.; orders ex transp. +1.3%, 13th straight m/m rise.

- Core capital goods shipments +0.3%, eighth gain in nine mths., pointing to a moderate contribution to Q2’26 GDP from business equipt. spending.

- Durable goods shipments +1.0%; unfilled orders +0.6%; inventories +0.2%.

USA| Jun 24 2026

USA| Jun 24 2026U.S. New Home Sales Unexpectedly Hit a Four-Month Low in May

- Sales -7.3% m/m (-6.8% y/y) to 580,000 in May; down 23.4% from a November high.

- Sales m/m down in the West (-26.9%) and South (-4.1%); up in the Midwest (+16.2%) and Northeast (+3.0%).

- Sales y/y down in all regions except the Northeast (+17.2%).

- Median sales price +2.0% m/m to $424,900, a 5-month high; avg. price +7.8% m/m to $540,600, highest since July ’22.

- Months' supply up to 10.3 mths., highest since July ’22.

- of33Go to 1 page