U.S. Retail Sales Jumped More than Expected in May

by:Sandy Batten

|in:Economy in Brief

Summary

- Total sales increased 0.9% m/m in May, nearly twice expectations.

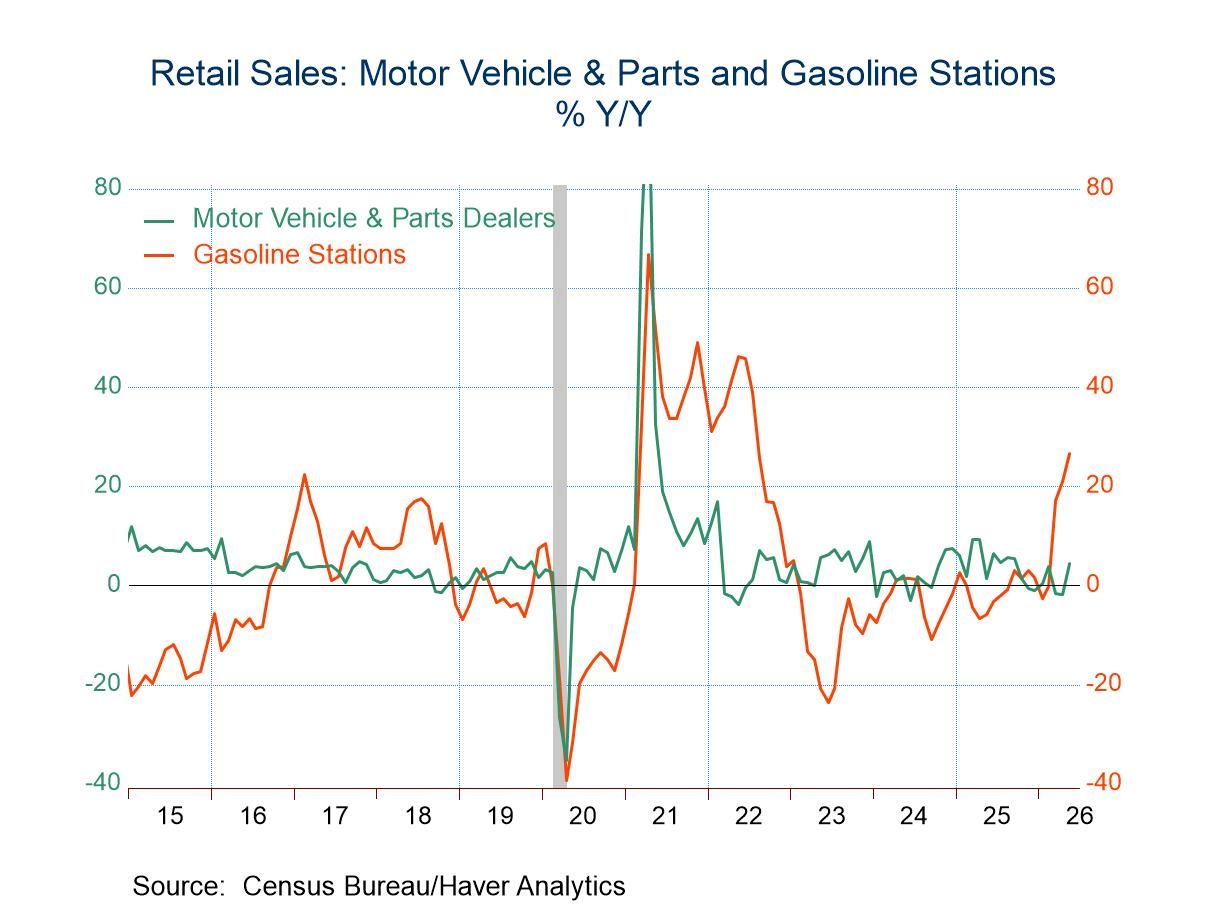

- Auto sales rebounded, rising 1.2% m/m in May, more than reversing a 0.9% monthly decline in April.

- Gasoline sales rose 3.4% m/m in May.

- Excluding auto and gasoline sales, remaining sales increased by a solid 0.5% m/m in May, the same monthly increase as in April.

- Sales of the retail control group that is used to construct PCE rose 0.7% m/m in May and are 8.6% annualized above the Q1 average.

Total retail sales rose a much larger-than-expected 0.9% m/m (6.9%y/y) in May following a slightly downwardly revised 0.4% monthly gain in April (previously 0.5% m/m), according to data released by the U.S. Census Bureau. The Action Economics Forecast Survey looked for a 0.5% m/m gain. Excluding autos, other sales increased 0.8% m/m (7.5% y/y) after an unrevised 0.7% m/m increase in April. Expectations were for a 0.5% monthly rise.

Elevated retail gasoline prices continued to boost the value of gasoline sales in May. Gasoline sales increased 3.4% m/m (26.5% y/y) in May on top of a 2.8% m/m increase in April. However, both monthly increases were slower than the 14.2% monthly jump reported in March. Gasoline sales accounted for 31% of total sales in May. However, sales were solid even without gasoline sales. Total sales excluding gasoline rose 0.7% m/m in April, up from 0.2% m/m in April. Sales excluding both autos and gasoline increased 0.5% m/m in May, the same monthly gain as in April.

The control group of sales (total sales excluding food services, autos, gasoline and building materials that the BEA uses to construct PCE in the national accounts) posted another solid increase in May, rising 0.7% m/m (6.3% y/y) following an unrevised 0.5% monthly increase in April. The strong performance at the end of Q1 followed by solid gains in April and May put the April-May level of control group sales up 8.6% at an annual rate from the Q1 average, pointing to another solid contribution by consumption to overall GDP growth in Q2. Consumer spending remains surprisingly resilient notwithstanding the recent hit to disposable income from the marked increase in energy prices.

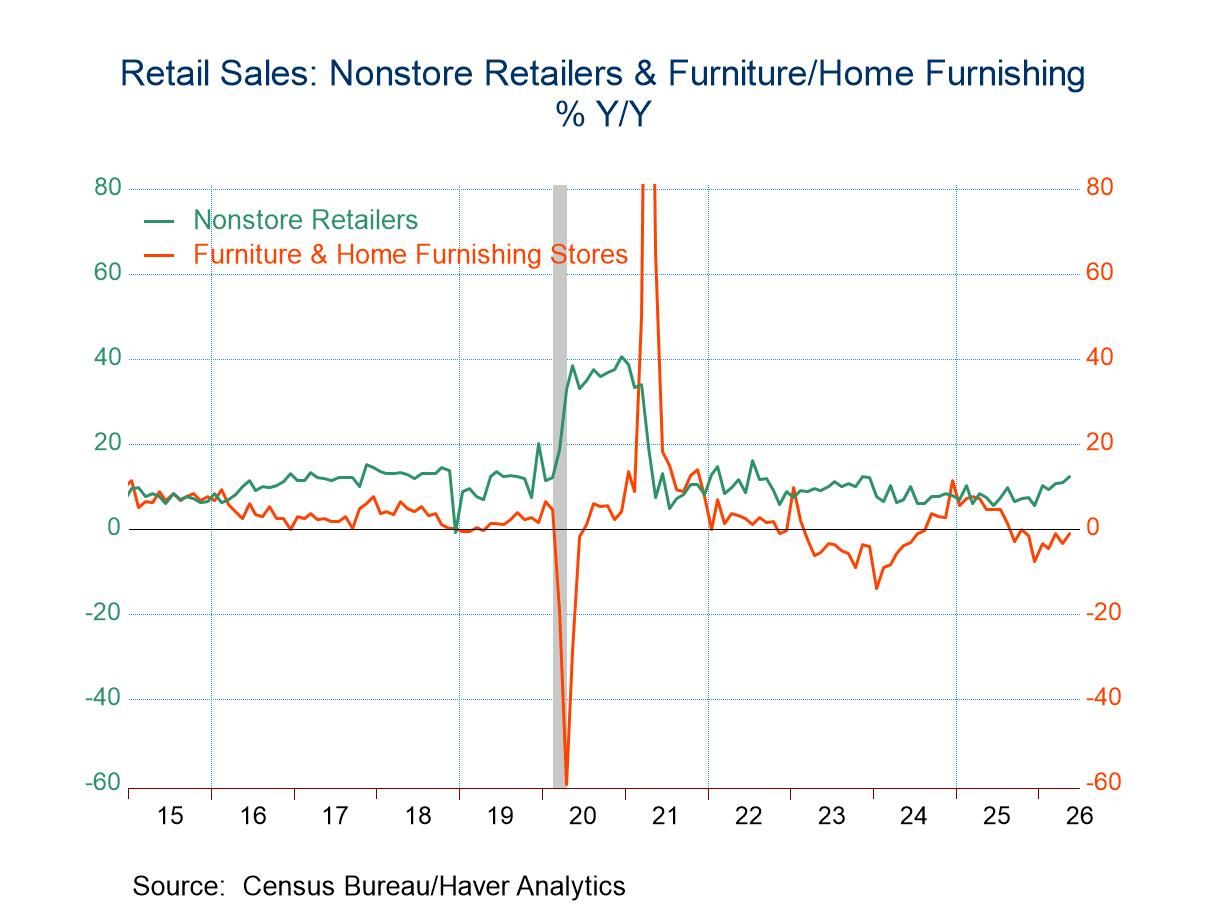

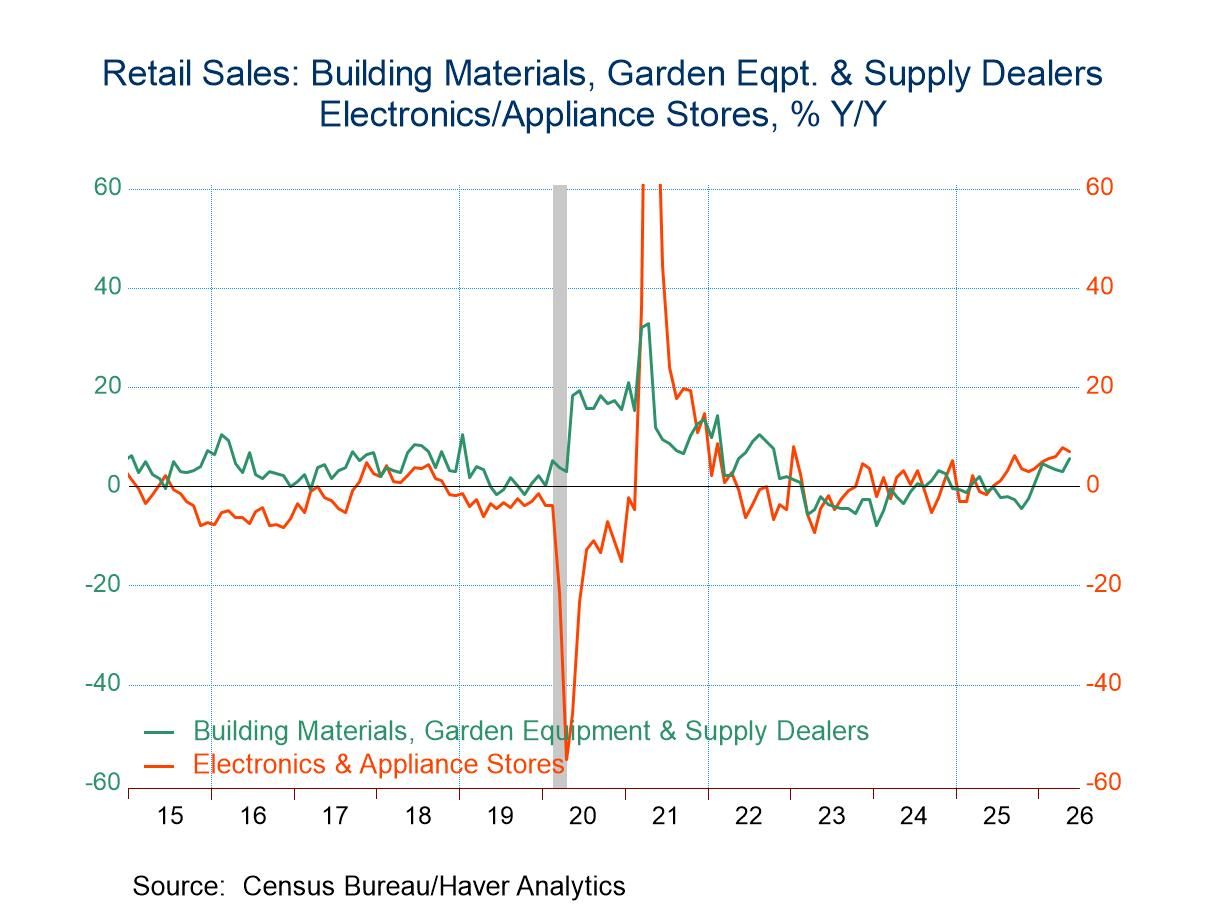

Sales generally increased across major sectors in May. Auto sales rebounded, rising 1.2% m/m in May and more than reversing the 0.9% monthly decline in April. This was the third gain in auto sales in the past four months. Furniture sales rose 1.0% m/m but sales at electronics and appliance stores slipped 0.5% m/m. Building material sales gained 1.0% m/m on top of a 1.1% monthly increase in April. Clothing sales rose 0.3% m/m. Sales at general merchandise stores gained 0.4% m/m in May. Miscellaneous sales jumped 2.3% m/m in May, their first monthly gain in three months. Sales by nonstore retailers continued their strong performance, increasing 1.5% m/m in May on top of a 1.1% monthly rise in April. Over the first five months of this year, nonstore retail sales have risen 7.2%, not annualized. By contrast, food sales were unchanged in May from April while sales at restaurants edged down 0.1% m/m in May, their first monthly decline in four months.

Retail sales data can be found in Haver’s USECON database. The expectations figures are from the Action Economics Forecast Survey in AS1REPNA.

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

Asia

Asia