U.S. Existing Home Sales Jumped 5.1% in December

by:Sandy Batten

|in:Economy in Brief

Summary

- Existing home sales jumped a much larger-than-expected 5.1% m/m in December, the fourth consecutive monthly gain.

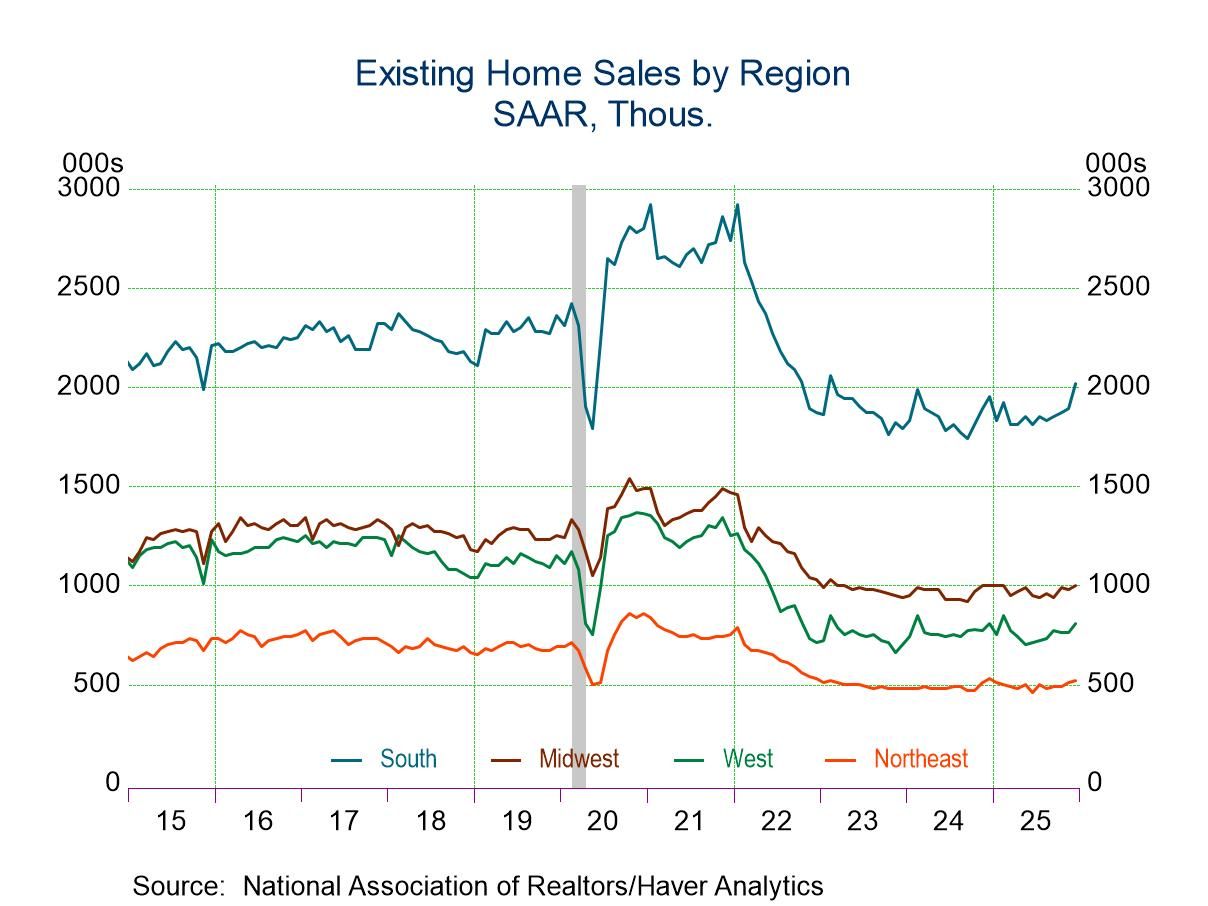

- Month-over-month sales increased in each of the four major areas.

- But year-over-year sales rose only in the South.

- For all of 2025, sales totaled 4.084 million, up slightly from 4.067 million in 2024.

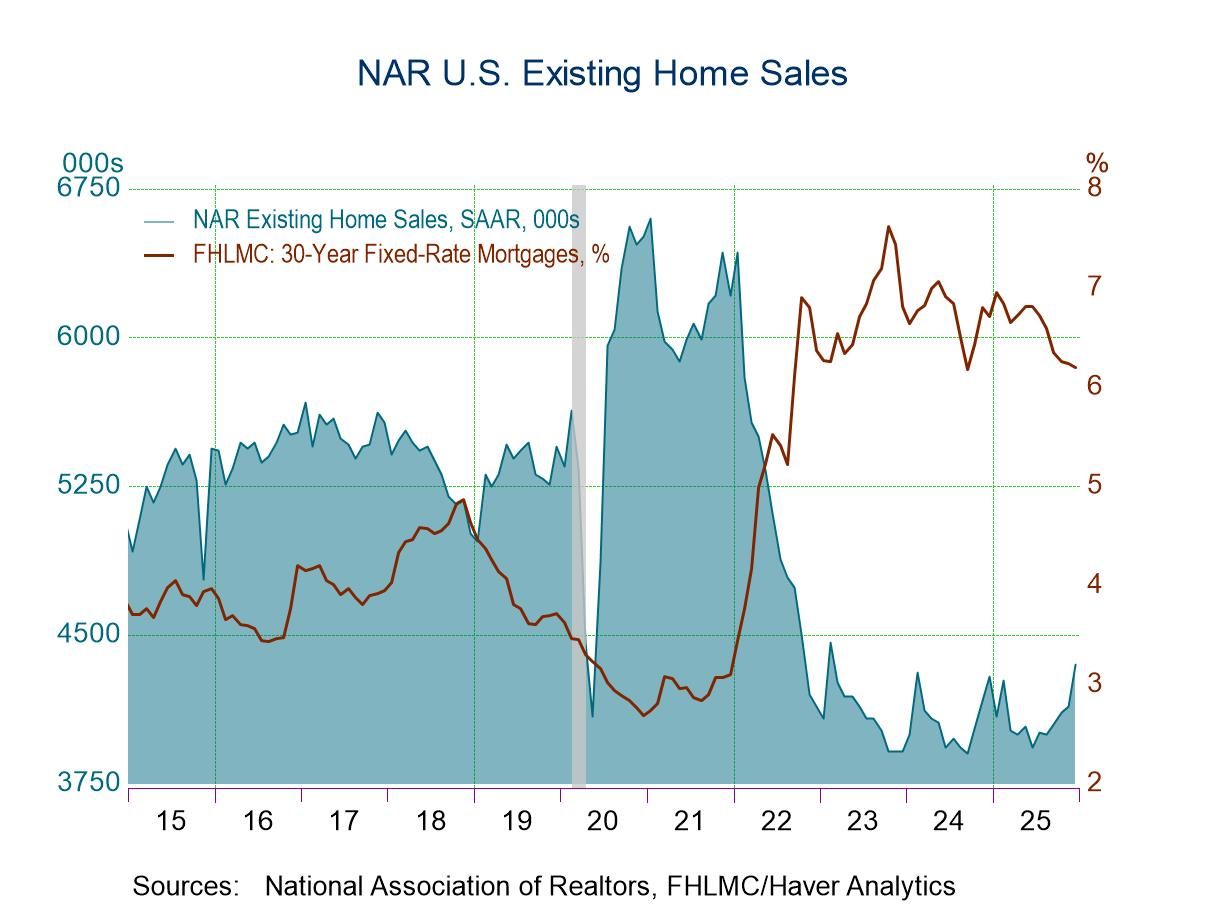

Existing home sales jumped 5.1% m/m (+1.4% y/y) in December to 4.35 million units (SAAR). This was the fourth consecutive monthly gain and was well above the 1.7% m/m increase expected by the Action Economics Forecast Survey. December sales were the highest since February 2023. For all of 2025, sales remained anemic, totaling just 4.084 million and only up slightly from 4.067 million in 2024, which was the lowest annual total in the history of the series dating back to 1999. The average effective 30-year mortgage interest rate fell to 6.51% in December from 6.54% in November. This is down markedly from 7.10% in May and accounts for some of the revival in home sales over the past several months. The sales figures are based on closings of sales contracts signed over the past couple of months.

Existing single-family home sales rose 5.1% m/m (+1.8% y/y) in December to 3.95 million. This was the fourth consecutive monthly increase and highest level of single-family sales since February 2023. Sales of condos and co-ops surged 5.3% m/m (-2.4% y/y) in December to 400,000, more than reversing a 2.6% monthly drop in November. For all of 2025, sales of single-family homes edged up to 3.706 million from 3.673 million in 2024. By contrast, sales of condos and co-ops declined to 378,333 from 393,333 in 2024.

Compared to a month ago, sales rose 2.0% m/m in the Northeast, increased 2.0% m/m in the Midwest, jumped 6.9% m/m in the South (the largest monthly gain since February 2024), and surged 6.6% m/m in the West (the largest monthly gains since February). Year-over-year comparisons were less flattering. Compared to a year ago, sales were unchanged in both the Midwest and the West and fell 1.9% y/y in the Northeast. By contrast, sales rose 3.6% y/y in the South.

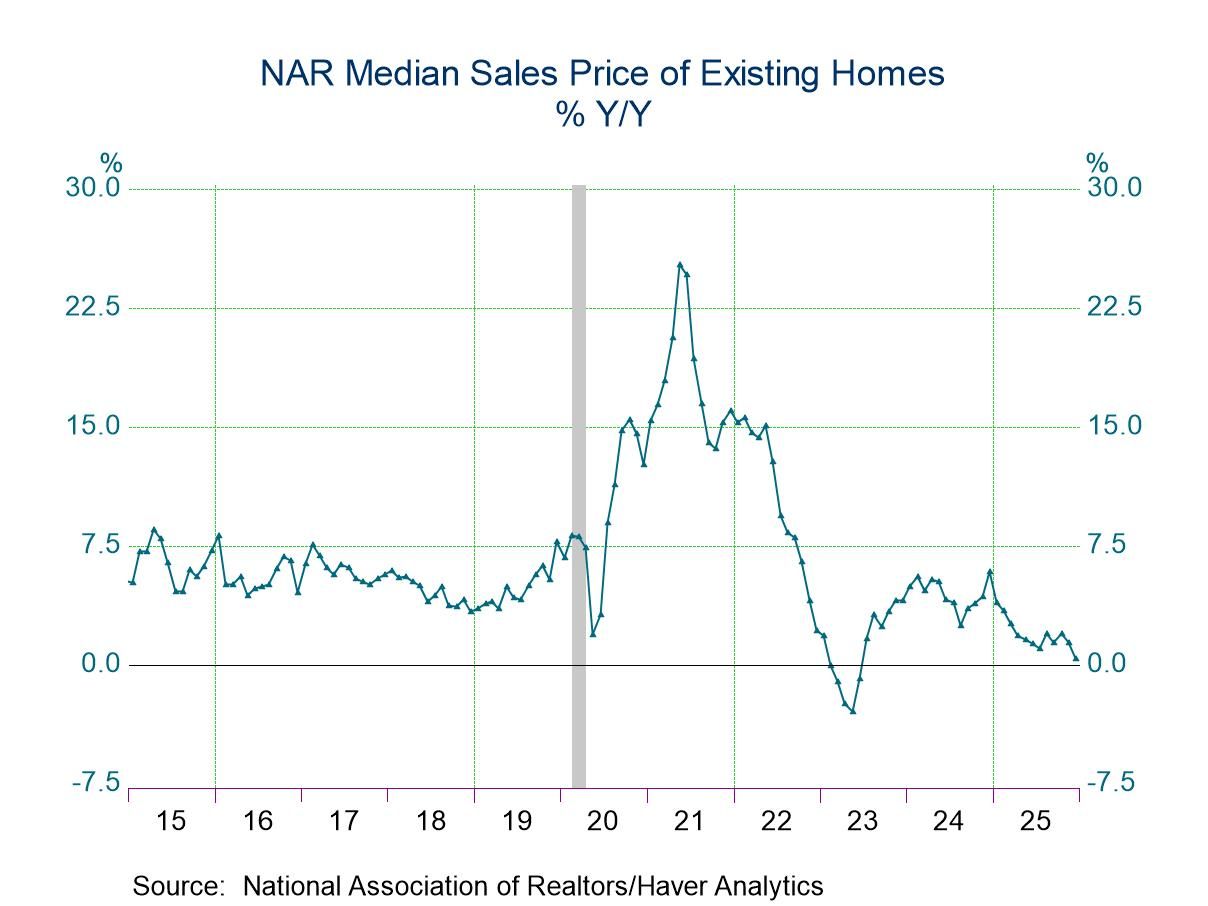

The median price of all existing homes (NSA) declined 1.1% m/m (+0.4% y/y) to $405,400 in December. The median price of an existing single-family home fell 1.3% m/m (+0.2% y/y) to $409,500 in December. Prices of single-family homes in the Northeast were essentially unchanged in December from November. However, prices in the other three regions fell: -3.6% m/m in the Midwest, -0.3% m/m in the South, -1.9% m/m in the West.

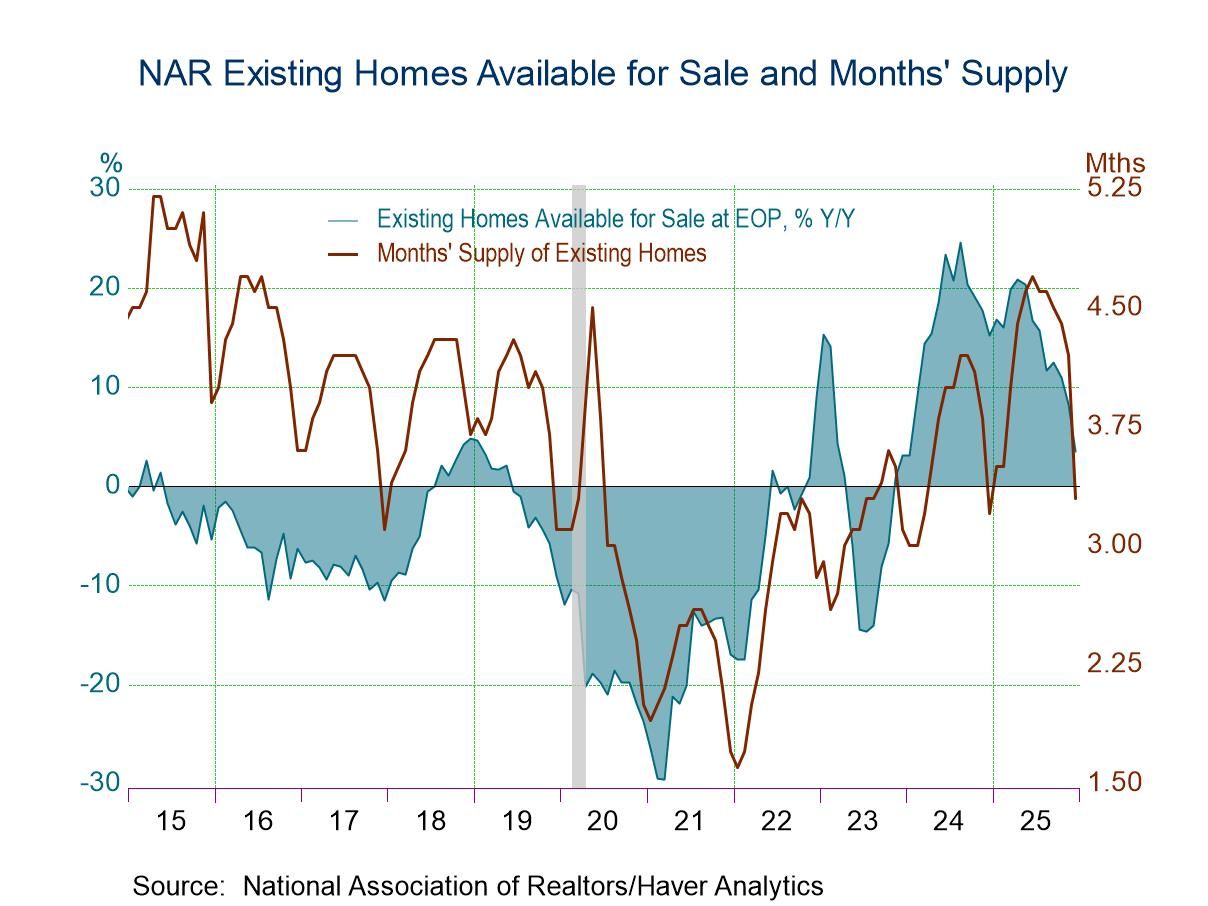

Inventories of homes for sale continued to weaken in December. The number of existing homes for sale (NSA) plummeted 18.1% m/m (+3.5% y/y) to 1.18 million units, the lowest level since January. The supply of homes on the market at the current selling rate (NSA) fell to 3.3 months, its lowest reading since last December.

The data on existing home sales, prices and affordability are compiled by the National Association of Realtors. The data on single-family home sales extend back to February 1968. Total sales and price data and regional sales can be found in Haver's USECON database. Regional price and affordability data and national inventory data are available in the REALTOR database. Mortgage interest rates can be found in the WEEKLY database. The expectations figure is from the Action Economics Forecast Survey, reported in the AS1REPNA database.

Sandy Batten

AuthorMore in Author Profile »Sandy Batten has more than 30 years of experience analyzing industrial economies and financial markets and a wide range of experience across the financial services sector, government, and academia. Before joining Haver Analytics, Sandy was a Vice President and Senior Economist at Citibank; Senior Credit Market Analyst at CDC Investment Management, Managing Director at Bear Stearns, and Executive Director at JPMorgan. In 2008, Sandy was named the most accurate US forecaster by the National Association for Business Economics. He is a member of the New York Forecasters Club, NABE, and the American Economic Association. Prior to his time in the financial services sector, Sandy was a Research Officer at the Federal Reserve Bank of St. Louis, Senior Staff Economist on the President’s Council of Economic Advisors, Deputy Assistant Secretary for Economic Policy at the US Treasury, and Economist at the International Monetary Fund. Sandy has taught economics at St. Louis University, Denison University, and Muskingun College. He has published numerous peer-reviewed articles in a wide range of academic publications. He has a B.A. in economics from the University of Richmond and a M.A. and Ph.D. in economics from The Ohio State University.

More Economy in Brief

Global

Global