U.K. Inflation Moderates Open Door for BOE Rate Cut

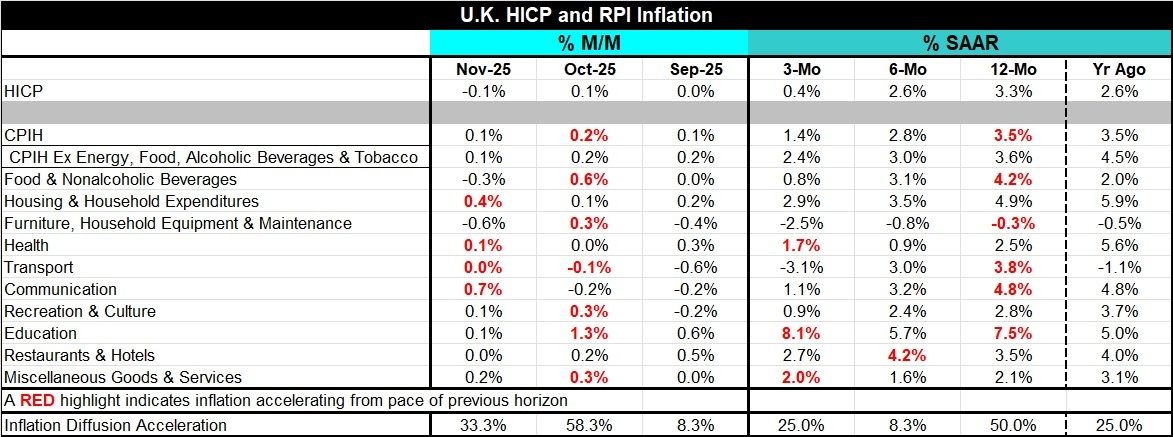

U.K. inflation has moderated in November, posting a 0.1% drop on the HICP, a 0.1% gain in the CPI-H headline measure as well as a 0.1% gain in the CPI-H core (excluding energy, food, alcohol, and tobacco). The sequential trend in core inflation points lower and is eroding but continues to run over the 2% mark set as a target by the Bank of England for overall inflation (over 12 months). The headline is excessive as well but also eroding.

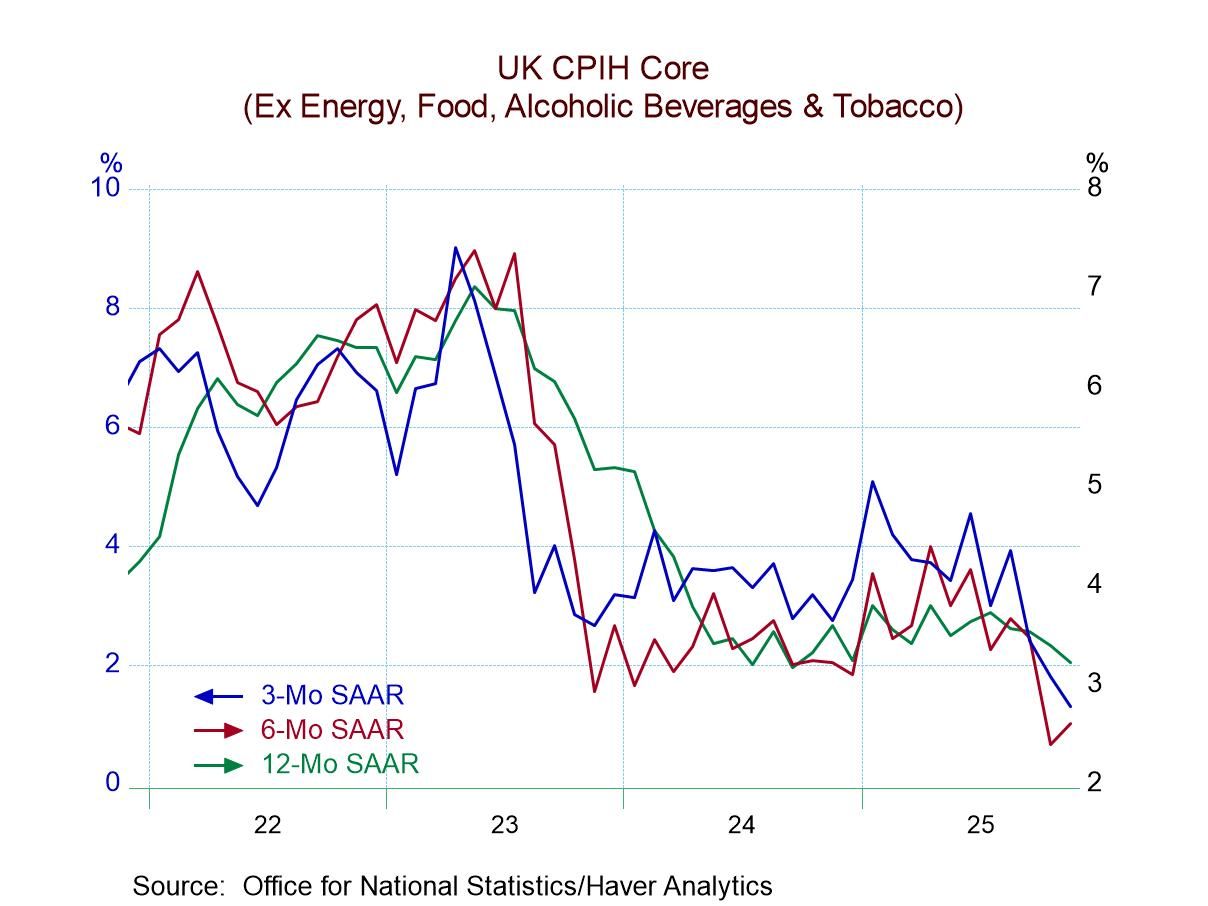

Sequentially the CPI-H gains 3.5% over 12 months, slows to a 2.8% annual rate over six months and then dips to 1.4% annual rate over three months. The CPI-H core rises by 3.6% over 12 months, ticks down to a 3.0% pace over six months, and then runs at a 2.4% annualized pace over three months.

The trend for the CPI core, and for the headline, both are quite good and would be completely consistent with the Bank of England cutting rates, a move that is widely expected – although the 12-month pace for each is excessive.

Not only is inflation showing signs of falling into the Bank of England's target zone, but the economy has been weak although the unemployment rate currently is only hovering around the 4% mark. Still, recent economic data have been weak, and the recent monthly GDP report posted a negative reading, further unsettling the outlook. The October monthly GDP change was estimated at -0.1% while the year-over-year increase in GDP in October produced a gain of just 1.1%. These metrics have put the U.K. economy on recession watch at a time when there has been a sharp revision in the budget process that will be much more constrictive. A sharp pullback in the manufacturing of motor vehicles is blamed for the sudden weakness in GDP in October. The three-month drop in GDP is the first such drop since December 2023.

Meanwhile, the headline and the core inflation statistics are progressing. The table calculates breadth statistics on how widespread inflation acceleration has been and we see that it has not been prevalent (over 50%) in September or November, although breadth did touch the 58% mark in October. Sequentially, inflation acceleration has been tamed: over 12 months (when it is neutral), six months, and three months. Over 12 months, inflation accelerated in only 50% of the categories. And inflation according to the CPI headline and in the core over six months continues to show deceleration to accompany narrowing breadth - only 8.3%. That reading indicates that there was more inflation deceleration than acceleration by a wide margin over six months. At 50%, inflation acceleration and deceleration forces are balanced. Readings below 50% indicate relatively more deceleration, and that is now the more common condition. Inflation acceleration is extremely rare across categories over six months and three months.

On balance, inflation by the headline and by the core measures is well disciplined and falling into line although still excessive over 12 months. The breadth statistics reinforce the view that inflation is broadly coming to heel at the same time the real economy data are showing a cooling in the economy- and perhaps an excessive slowing at that. The new budget should put the economy under additional downward pressure, further restraining inflation and causing growth to moderate. In this situation, a rate cut from the Bank of England is the odds-on bet. Perhaps the only question now is how large a cut? How much will the Bank think that circumstance have changed and that key trends have been altered in a significant way? Will policy react mostly to lower trend tempered by an excessive 12-month pace, or will it be willing to look farther forward and weight heavily the deteriorating economic trend as well?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global