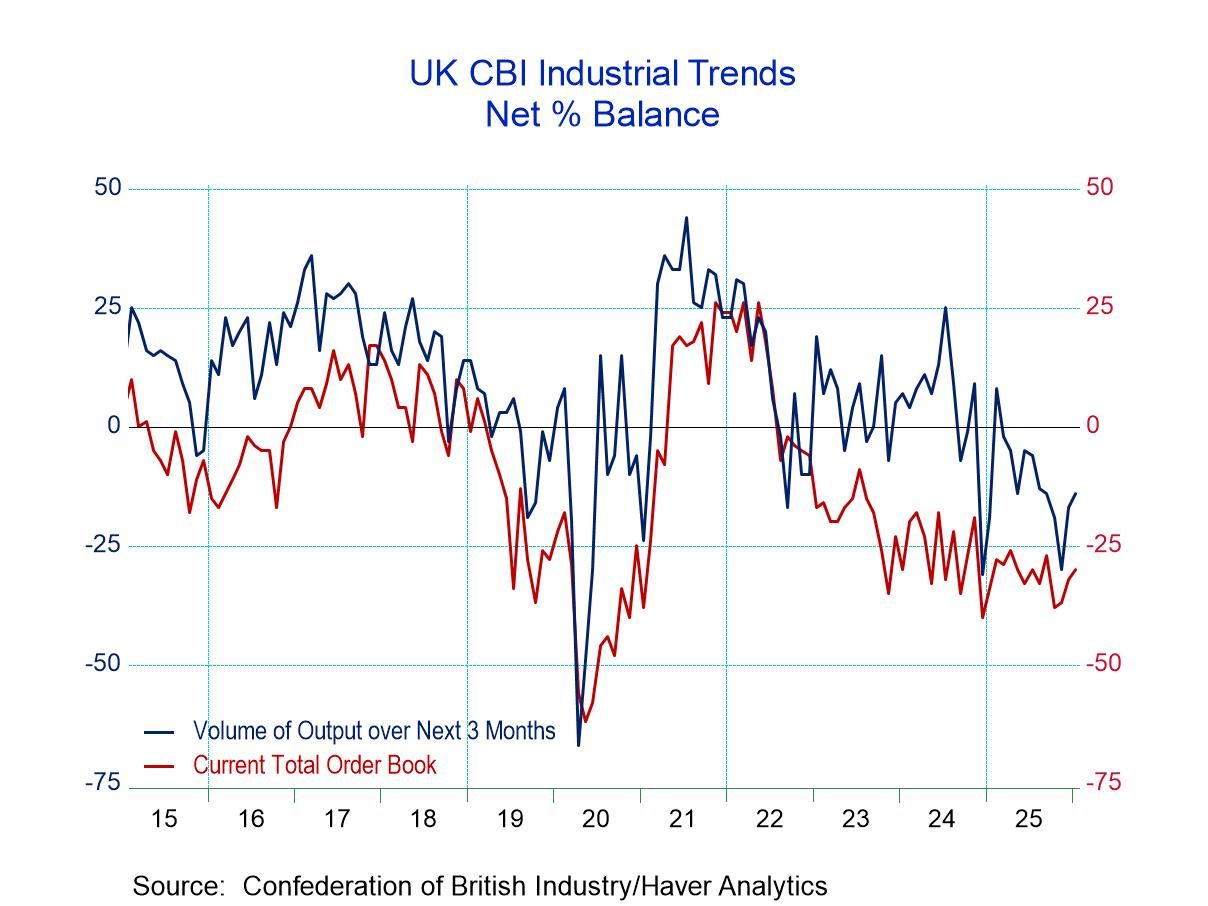

U.K. CBI Industrial Survey Flags Trouble Ahead

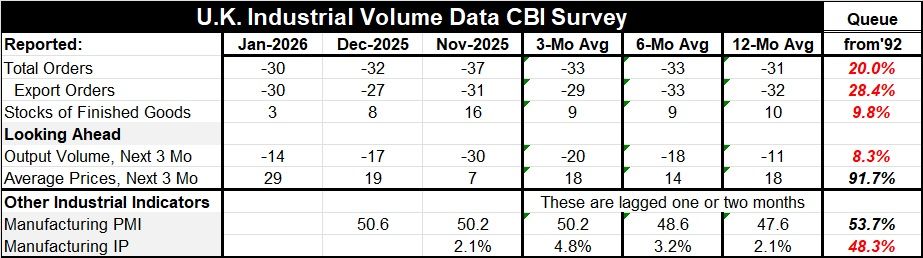

The CBI (Confederation of British Industry) Industrial Trends Survey showed slight improvement in orders in January 2026 as the survey reading rose to -30 on a net basis from -32 in December and -37 in November. However, the 12-month average of the order series is -31 and so the improvement compared to conditions that prevailed over the last 12 months is not significant.

Export orders, on the other hand, deteriorated to -30 in January from -27 in December although that reading was slightly better than the -31 print in November. Once again, the -30 reading for January is only slightly better than the 12-month average of -32.

Stock-building slowed in January at +3 compared to +8 in December and +16 in November. That, actually, could be good news suggesting that industries are getting control of their inventories at a time when sales have been weak.

Looking ahead for output volume over the next three months improved to -14 in January from -17 in December and -30 in November, a substantial pick up over this period. But the reading for January at -14 is still slightly more negative than the 12-month average of -11.

The unequivocally stronger reading in the table, unfortunately, is for prices with average prices over the next three months at a +29 net reading, up from +19 in December and up from +7 in November. The reading of +29 in January compares to a 12-month average of +18 indicating a significant pickup compared to conditions that prevailed over the last 12 months.

Evaluating these readings by ranking the queue standings of the net values and data back to 1992 shows total orders have a 20th percentile standing, export orders have a 28.4 percentile standing, while the stocks of finished goods have a 9.8 percentile standing, and expected output - despite its recent improvement - is quite weak with an 8.3 percentile standing. Average prices, on the other hand, are quite strong with a 91.7 percentile standing, indicating that the forces of inflation looking ahead are quite strong despite relatively weak demand and output conditions that are expected.

CBI data compared to annual growth rates in manufacturing and to the manufacturing PMI show rankings actually much better than the CBI survey. The manufacturing PMI has a 53.7 percentile standing that's only on data back over the last four years. The manufacturing production data have a 48.3 percentile standing, which is still very close to its 50-percentile standing, which would be its historic median. So, we have another case here of the accounting data being stronger than the survey data from the CBI. The strength in manufacturing industrial output does not compare favorably with the weakness portrayed in the CBI survey even though the manufacturing data are only up-to-date through November. The CBI data are up-to-date through January. And since CBI data generally show some stability or improvement from November to January, that data time mismatch with industrial production doesn't seem to be the reason for these readings being so vastly different. We’re going to have to keep an eye on other metrics for manufacturing to see which one of these surveys is giving us the best information.

For now, we don't know which of these series is the best and what we're looking at is a CBI series that is touting a great deal of economic weakness and portraying significant increases in prices over the next three months.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global