This Isn't 1999 — But That Doesn't Mean There's Nothing to Watch

by:Andrew Cates

|in:Viewpoints

The comparisons are hard to avoid. Soaring valuations, massive capital expenditure on data centres and AI infrastructure, and near-universal conviction that a transformative technology is about to reshape the economy. To many observers, today looks uncomfortably like the late 1990s.

The parallel is understandable. It is also, on the most important dimension, wrong — and Haver data help explain why.

The critical variable: who holds the debt

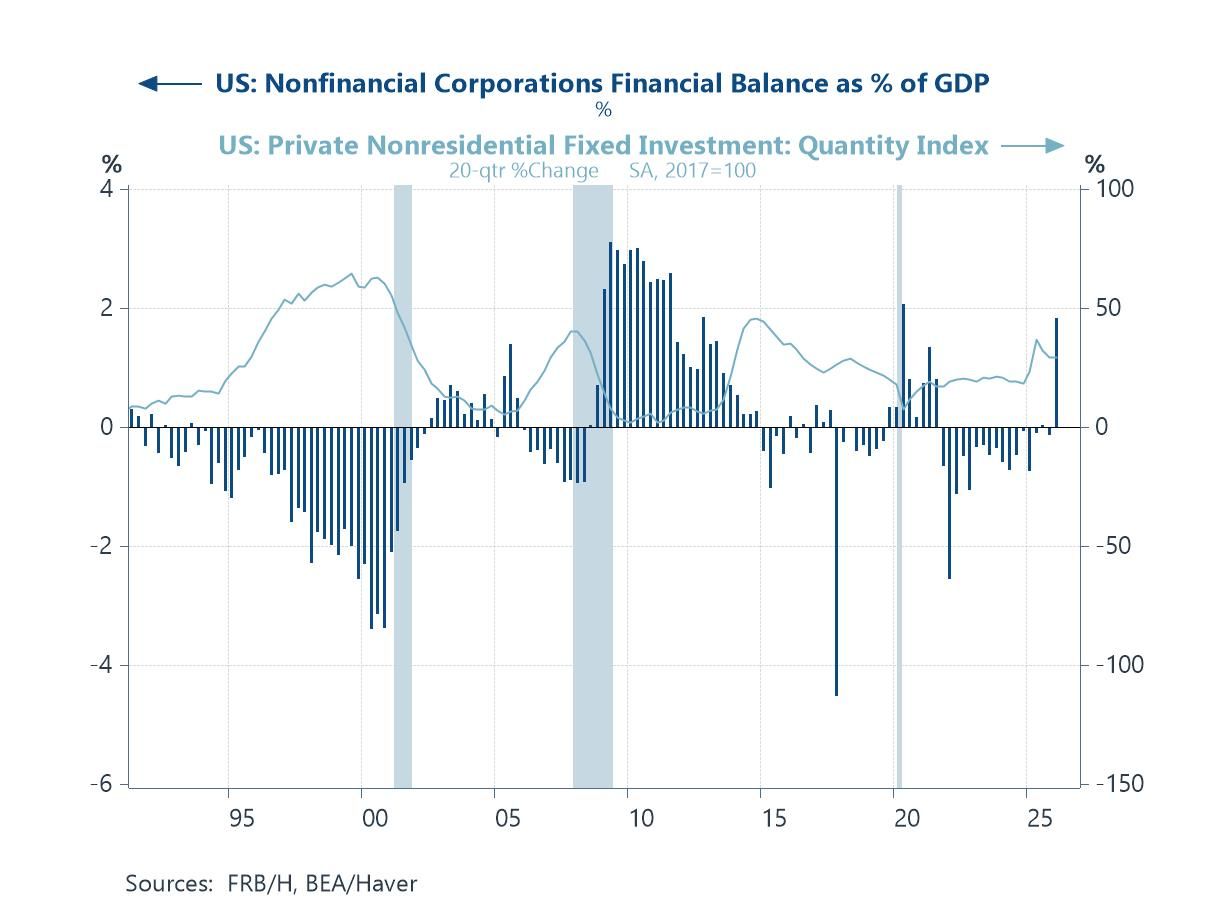

Investment booms become dangerous when they are financed by leverage. The late 1990s are a textbook case. As internet enthusiasm intensified, US corporations borrowed heavily to fund infrastructure buildout. By 2000, the non-financial corporate sector was running a financial deficit approaching 4% of GDP — spending substantially more than it earned. When expectations proved too optimistic, investment collapsed, and corporate deleveraging deepened the downturn.

A similar mechanism operated before the Global Financial Crisis, this time concentrated in the household sector. Cheap credit, rising house prices, and aggressive lending standards left consumers dangerously overextended. When prices turned, the deleveraging that followed produced the deepest global recession since the Depression.

Leverage was not merely a symptom of those episodes. It was the mechanism that made the busts so destructive — and so protracted.

Today's picture, as measured in Haver's Flow of Funds and national accounts databases, looks fundamentally different. Despite the AI-related surge in cloud infrastructure, semiconductor, and data centre spending, the US non-financial corporate sector is currently running a financial surplus of roughly 1.8% of GDP (Q1 2026). Corporate America is investing aggressively — and still generating more cash than it spends. The boom is being financed through profits, not debt accumulation. Financial crises are typically balance-sheet events. That particular vulnerability is far less pronounced than it was in either 2000 or 2007.

The borrowing hasn't disappeared — it has migrated

If corporations are running surpluses while the US runs a sizeable current account deficit, someone must be absorbing the other side of that position. The answer, visible in federal budget data available through Haver, is the federal government. Washington has effectively become the borrower of last resort, allowing the corporate sector to invest heavily while maintaining healthy balance sheets.

This matters for the financial stability question. Governments do not face margin calls and are rarely forced into the kind of rapid deleveraging that devastates private sectors. Excessive public debt creates real pressures — higher long-term rates, rising debt-servicing costs, sustainability concerns — but these tend to unfold over years rather than in the abrupt fashion that follows private-sector deleveraging. Pockets of vulnerability remain in commercial real estate, parts of private equity, and speculative-grade borrowers — all trackable through Haver's credit and property databases — but these remain sectoral risks rather than systemic ones.

The risks have shifted, not disappeared

Relative financial strength should not be confused with an absence of risk. The more important challenges ahead may have little to do with leverage and much more to do with the supply side of the economy.

Energy constraints, geopolitical fragmentation, demographic pressures, and infrastructure bottlenecks are shaping the long-term growth outlook in ways that financial markets have largely chosen to ignore. This is the underappreciated dimension of the AI investment story. The productivity gains promised by AI depend not only on software and algorithms, but on electricity generation and transmission, critical minerals, and physical infrastructure — variables that Haver tracks across dozens of databases covering energy production, commodity markets, and capital expenditure by sector.

A correction in AI-related valuations remains entirely possible — current pricing may well embed unduly optimistic assumptions about the pace and breadth of productivity gains. But even a significant correction would likely play out differently from previous episodes. Without widespread private-sector leverage, falling asset prices would not trigger the deleveraging spiral that made 2001 and 2008 so economically damaging.

The last two major crises were balance-sheet events. The next one, if it comes, may have less to do with debt and more to do with whether the real economy — energy grids, supply chains, labour markets — can actually deliver what financial markets are currently pricing in.

Haver's Flow of Funds, national accounts and energy, databases provide the granular time-series coverage needed to monitor each of these dynamics. Contact us to learn more.

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

Global

Global