The Backward Pass of Tariffs?

by:Joel Prakken

|in:Viewpoints

In early 2025 the Trump Administration announced a base tariff of 10% on imported goods, additional steep “reciprocal tariffs” on goods imported from countries running large trade surpluses with the United States, and additional levies on specific imported commodities. The average tariff rate on all imports surged from approximately 2.5% to 10%. The increase would have been larger if not for the many “slips twixt cup and (dutiable) lip.” Indeed, it might surprise many that today only 40% of imported goods are subject to tariffs (Chart 1).

Regarding the incidence of the tariffs. A model of supply and demand implies that the price of imports net of tariffs is positively related to their price measured in home currencies but inversely related to both the nominal exchange rate and the tariff rate. The more inelastic supply, the larger the negative response of price to the tariff rate. That is, the more the incidence of tariffs is shifted backwards to foreign suppliers.

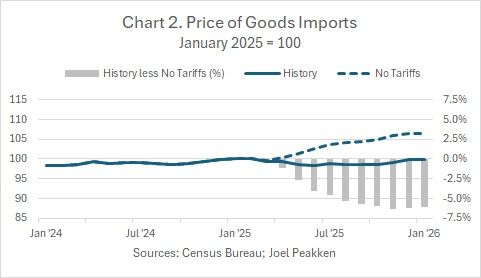

The price of imported goods, reported net of tariffs by the Bureau of Labor Statistics, has remained remarkably constant during this episode (Chart 2). Many observers, initially including myself, advanced this constancy as evidence that the tariffs have not been passed backwards. But my thinking on the issue has evolved. Previously in this space (“Are Foreigners Paying the Tariffs? October 1, 2025), I wondered whether a decline in the US dollar that put upward pressure on import prices might have offset, and thus obfuscated, a tariff-induced decline. Now, with the accumulation of enough time series data, that empirical case can be made directly.

The table reports a regression of import prices, estimated in logarithmic changes, based on the model of supply and demand described above. The monthly sample extends through January of 2026. The coefficient on trade-weighted foreign prices in home currencies (= 1.18) is highly significant and not statistically different from the expected unitary value. The highly significant pass-through of the Fed’s broad, trade-weighted exchange rate index is 54% over 10 months, consistent with the empirical literature on the subject. Finally, the results suggest that 84% of tariffs are passed backwards over 6 months. In this regression, the combined effects of an upward drift in foreign prices and a sharp decline of the dollar last year just offset downward pressure on import prices from the “backward pass” of the new tariffs.

For an alternative perspective, I simulated the equation over the last year of history holding the tariff rate constant at its January 2025 value. The results suggest that if the tariff rate had not increased then, all else equal, import prices would be 6% higher today (Chart 2); that is, the tariffs have induced a 6% decline in import prices. While this contradicts the consensus view, I find it hard out of hand to dismiss results that have a solid theoretical footing and are so highly significant. And perhaps they help explain why the inflationary impact of the tariffs seems less than initially feared.

Joel Prakken

AuthorMore in Author Profile »Joel Prakken is former Chief US Economist of S&P Global and IHS Markit, co-founder of Macroeconomic Advisers, and past president and director of the National Association for Business Economics. He has served as an outside advisor to the Congressional Budget Office, on the Advisory Panel of the Bureau of Economic Analysis, and as a consultant to the Joint Committee on Taxation. He holds a BA in economics from Princeton University and a PhD in economics from Washington University in Saint Louis.

Global

Global