Energy Shock, What Energy Shock?

by:Ethan Harris

|in:Viewpoints

While the press is filled with stories about the biggest oil supply shock ever and crippling gasoline prices, the economic data look fine so far. Nonetheless, I’m getting more, not less, worried.

So far, so good

The business press is loaded with stories about how the rise in energy (and related) prices is a huge shock to the economy. There are endless articles about how $4/gal gasoline prices are devastating to households. And perhaps warning comes from none other than the International Energy Agency. They are all over the press arguing that this is “the largest supply disruption in the history of the global oil market.”

And yet, seemingly miraculously, the US economy seems fine. Most March indicators were solid. Payrolls surprised to the upside and jobless claims remain low by historical standards. suggesting low layoffs. The various purchasing managers indexes are healthy. The only ugly data is the chronically weak consumer confidence surveys. Overall, trendlike growth of 2% or so seems to continue. What gives?

Time

The first thing to note is that there are lags between the onset of the shock and the impact on the data. It takes time to change behavior—people tend to look through temporary shocks. Moreover, current data releases measure where the economy was in the middle of March. April data should show some (small) impact.

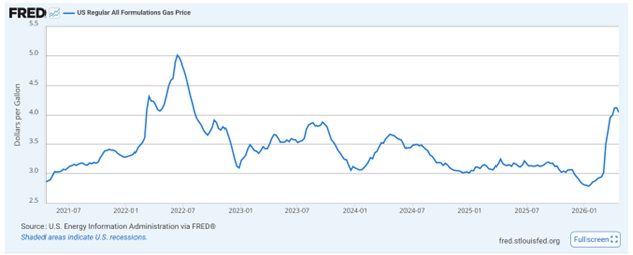

A small shock so far

Despite the warnings from the IEA, so far this is a small shock by historical comparisons. It makes no sense to measure an oil shock looking only at the peak amount of supply disrupted. The duration of the disruption is more important. It is the cumulative amount of oil taken off the market that matters. A short disruption is cushioned by inventories and the consumer response to a short price spike will be small. The size and duration of today’s price shock isn’t even close the recent Russian shock, let alone the 1970s oil shocks (chart).

Tailwinds

Financial conditions remain supportive of growth. One of the big misunderstandings around the US economy is that “r-star”—the funds rate that neither stimulates nor weakens the economy—is only about 3%. That is way too low. It implies four years of very tight monetary policy with the funds rate as much as 2.5% above r-star. Why then have financial conditions and the economy remained healthy. Even today, with only a brief dip in the stock market, financial conditions remain a tailwind for growth.

The Little Orphan Anne Markets

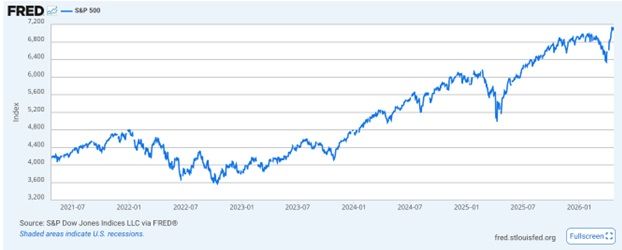

Financial markets, particularly oil futures and the stock market, seem to assume that an end to the energy crisis is always only days away. Benchmark prices for Brent and WTI—which are the month-ahead futures—seem to assume a high probability of a resolution is imminent. Buoyed by strong earnings and promises of a quick end to the energy shock, the stock market is back to setting new records. The markets seem encouraged by the extended ceasefire.

May day?

There is a big debate over which side in the US-Iran negotiations will blink first. However, for the US and global economy, that is not the key question. What matters is when they blink. Specifically, when do normal oil flows resume? My reading of the news is that this could take a long time. Both sides seem to think they have the negotiating advantage and both sides seem to be digging in for a long fight.

Meanwhile, the risk of a nonlinear oil price surge is rising. Inventories are being steadily depleted, tankers at sea have dropped off their cargos. Moreover, the US has been relatively insulated so far. However, there are already physical shortage and much higher prices outside the US. President Trump has said, xxxxxxx. However, as oil and refined products are moved out of the US and into global markets, the pain will intensify for the US. My reading of the experts is that the price “tipping point”—if the Strait is not reopened—is sometime this month.

The upshot is that this is not a good time for complacency. So far, the energy shock has been relatively mild with very little economic impact. However, time is not on our side: the longer the Straits are closed the bigger the risk of a serious energy shock.

Ethan Harris

AuthorMore in Author Profile »Ethan Harris has a Ph.D. in Economics from Columbia University and was the Head of the Domestic Research Division at the NY Fed. He was Chief US Economist at Lehman Brothers from 1996 to 2008 and Head of Global Economics at Bank of America from 2009 to 2023. Currently he is the author of the blog Ethan on the Economy.

More Viewpoints

Global| Aug 04 2026

Global| Aug 04 2026The Real Rate Has Turned — and the World Still Expects the Old Normal

by:Andrew Cates