The Trump Economy, One Year In

by:Ethan Harris

|in:Viewpoints

The US economy is neither in a “Golden Age,” as Trump supporters argue, nor is it regularly flirting with recession, as Trump critics argue. In reality, Administration polices have contributed to “stagflation”—a combination of below-trend growth combined with persistent above-target inflation. An even bigger test lies ahead, with a significant risk of a major energy shock.

Presidential report cards

In comparing Presidential regimes, a common approach is to average growth and inflation over the four years in office. Of course, this ignores other drivers of the economy, and the lagged effect of policies from the prior President.

Trump’s Presidency is different. He took “ownership” of the economy out of the gate, with sharp shifts in economic policy. In the process Congress was largely sidelined and Fed policy became secondary. This has been Trump’s economy from the get-go.

Let’s briefly look at how five kinds of policy shifts—trade, immigration, tax cuts, deregulation and war have impacted the demand and the supply-side of the US economy.

Demand damage

The impact of Administration policies on spending and demand has been mixed. The good news is that income tax cuts tend to stimulate consumer spending and corporate tax cuts tend to stimulate investment. Unfortunately, these positive effects have been canceled out by the dramatic increase in consumer and business uncertainty.

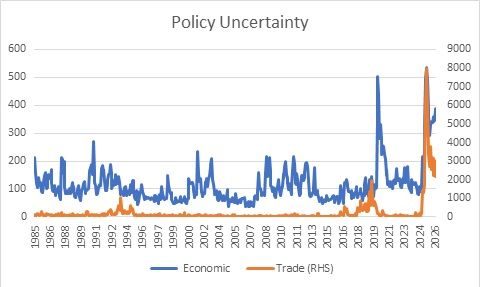

The chart below shows a news-based measure of policy uncertainty from Bloom and others. There has been a massive spike in policy uncertainty in general and trade policy uncertainty in particular. The later is much higher than during the first trade war. This has put sand in the gears of the economy, with firms reluctant to hire and invest and households reluctant to spend. This is one of the reasons why business investment, outside of data centers, has remained weak and manufacturing jobs have declined.

Source: policyuncertainty.com

Golden age or cooking the golden goose?

The cross currents on the supply side of the economy are even more dramatic. The Administration sees a big boost in potential growth as deregulation improves productivity, tax cuts encourage work and investment, and tariffs induce companies to move operations to the US.

Getting the timing right

Unfortunately, this is not the end of the story. History shows that there are long lags from policy changes to improved potential. It takes years to build new productive capacity, change business planning around regulations, and to revamp supply chains. Indeed, as I noted above very high levels of uncertainty have made the lags even longer than usual. The increase in investment projects (outside of AI) hasn’t happened yet, let alone completion of the projects.

Meanwhile some policies are undercutting potential growth. Not only is policy uncertainty freezing up business plans, huge budget deficits are absorbing savings, crowding out private investment. Perhaps most important, immigrant reduction policy has been very successful in slowing the growth of the labor force. The “breakeven rate” for employment growth—the rate that keeps the unemployment rate constant—has dropped close to zero. This is down from the 150k or more at the height of Biden’s “open door” policy. This is already having a big impact on potential growth.

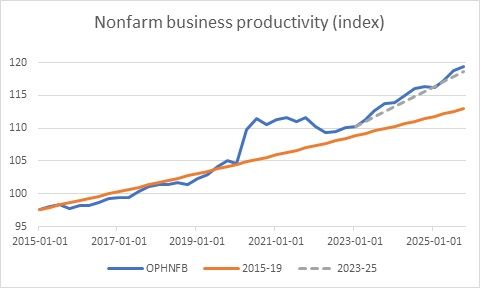

With all that said, other developments—unrelated to Administration policy—have been good for potential growth. As the chart shows, productivity growth started to trend higher back in 2023. The driver was not Administration policy, but investments and innovations in response to the COVID shock. Similarly, while it is too early to see real benefits from Artificial Intelligence, as data centers are completed, and businesses learn how to use the new tools it could spark a productivity boom.

Source: BLS

The verdict

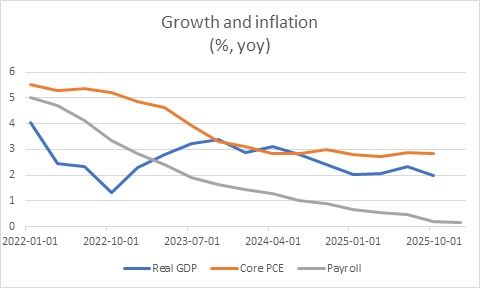

Coming into 2025 both growth and inflation were trending down. On net, Administration policies seem to have caused a leveling off inflation, while contributing to slower growth, particularly in the labor market inflation (chart). On the other hand, I think the trend growth in productivity has improved, first from the business response to COVID and over time due to Artificial Intelligence.

Source: BLS, BEA

Unfortunately, the Administration’s second year could look about the same or considerably worse. I expect immigrant reduction policy to continue to suppress labor force growth. I also think high levels of policy uncertainty are here to stay. On the other hand, the benefits of the tax cuts and deregulation could start to show up.

The wild card, of course, is the Iran war. I think both economists and investors are underestimating the risks to both growth and inflation. So far, the US economy has been spared the worst of the shock: energy prices have jumped more in Europe and there are physical shortages in Asia. However, as US oil exports increase, US prices will tend to rise to global levels. Most important, there is no easy answer for opening the Strait and the longer it is closed, the bigger the risk of a huge price spike. Fingers crossed.

Ethan Harris

AuthorMore in Author Profile »Ethan Harris has a Ph.D. in Economics from Columbia University and was the Head of the Domestic Research Division at the NY Fed. He was Chief US Economist at Lehman Brothers from 1996 to 2008 and Head of Global Economics at Bank of America from 2009 to 2023. Currently he is the author of the blog Ethan on the Economy.