Warsh and the Bond Market Vigilantes

by:Ethan Harris

|in:Viewpoints

Warsh and the bond market vigilantes

The recent bond market sell off is a reminder of the many risks to the market, including Warsh’s appointment as Fed chair. The market is justifiably worried about three of Warsh’s main policy views: (1) productivity growth will solve the inflation problem without help from the Fed, (2) the Fed should be selling off most of its bond holdings and (3) the Fed should be focused on the weakest of the core inflation metrics—the “trimmed mean” PCE deflator.

Independent, but in agreement

President Trump has made it abundantly clear that he wants lower interest rates. Indeed, he has said he will not appoint a Fed chair who does not believe major cuts in the funds rate are warranted and he expects the Fed to cut under Chair Warsh.

Last month, Bessent offered a more flexible message to the Fed. He noted the uncertainty around the Iran war, saying “if they [the Fed] want to wait for some clarity, I understand that.” Indeed, “we should wait for the new chairman, Warsh, and let him lead the next cycle.” Looking ahead, he said, “the conflict will end, prices will come down, and then headline inflation will come down.” This suggests a short honeymoon period for Warsh, followed by a string of rate cuts.

In his campaign for the Fed chair, Warsh has been adamant that he has independently arrived at a similar conclusion. He does not want to lower rates because the President wants it, but because economic fundamentals warrant lower rates. Specifically, he strongly supports two arguments. First, the Fed does not need to hike rates to bring inflation down. Quite the opposite, surging productivity will not only solve the inflation problem, but demands that the Fed cut rates to accommodate .

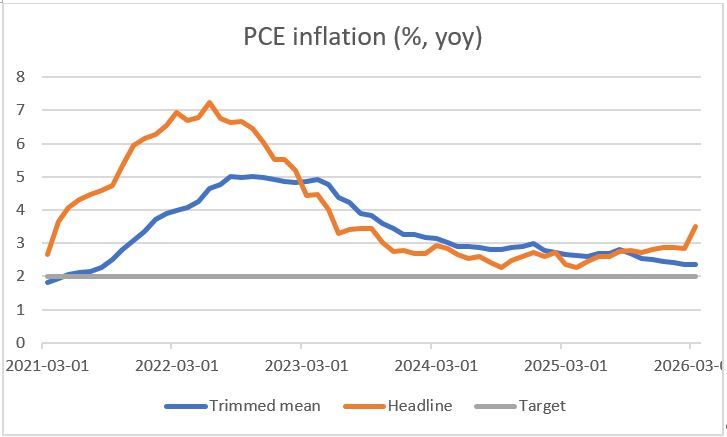

Second, he argues that any upward pressure on inflation is transitory. Indeed, in his testimony, he argued that the Fed should shift to the “trimmed mean” PCE as its preferred measure of core inflation. This metric strips out the components with both the highest and the lowest inflation. In March, the year-over year increase was just 2.4%, and much lower than other metrics (chart).

Source: BLS, FRB Dallas

Fed-Treasury discord?

While Warsh sounds very dovish on interest rates, he seems very hawkish about the Fed’s balance sheet. He wants to shrink the balance sheet back to its normal size as a share of GDP, with a particular focus on selling mortgage assets and treasury bonds. Of course, the impact of such a policy would be to put upward pressure on bond yields. Interestingly, the Administration is doing the opposite by having Fannie and Freddie buy (a modest amount of) mortgage back securities to bring down mortgage yields. On a similar vein, Fed Chair candidate Rick Rieder proposed to President Trump that the Fed should aid the process by buying bonds.

Bond vigilantes

Back in the 1980s, Ed Yardeni coined the term “bond vigilante.” The idea was that bond traders had a powerful impact on policy makers because they would drive up yields on any signs of irresponsible fiscal or monetary policy. Indeed, they likely had some impact on the drop in both inflation and the budget deficit from 1980 to 2000.

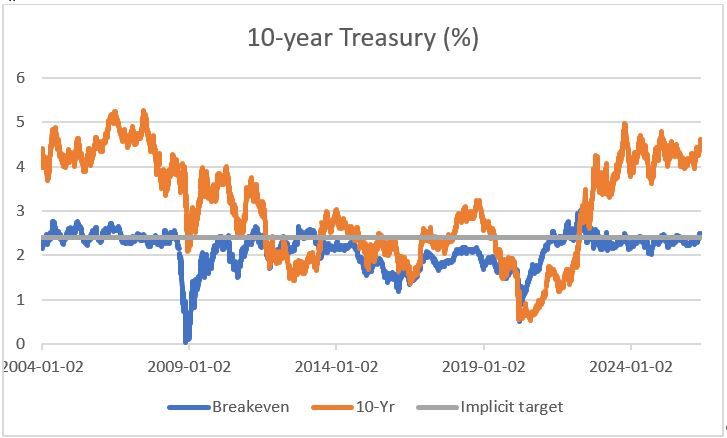

Unfortunately, in the last 25 years or so the bond vigilantes seem to have gone into hibernation. There has been little response to a series of threats to the bond market: • Dysfunctional government and credit rating downgrades • An on-going trend deterioration in the budget balance • Signs of a slow-motion slide in the dollar’s dominance as a reserve currency. • Despite more than 5 years of high inflation and public concerns about inflation, bond “breakevens” remain close to the Fed’s implicit CPI target of about 2.4% (chart). • Serious threats to Fed independence and Trump’s insistence that any new Fed Chair must agree with the case for rate cuts.

Source: Board of Governors of the Federal Reserve System

Hoping for a hawk

In a paper back in 1985, Ken Rogoff made the case for appointing a Fed Chair with a hawkish reputation: "Society can sometimes make itself better off by appointing a central banker who does not share the social objective function, but instead places 'too large' a weight on inflation-rate stabilization relative to employment stabilization." Translating this into English: having a strong anti-inflation reputation can mean not having to tighten as much to keep inflation down.

When the facts change

The upshot is that bond investors are understandably worried about how far Warsh will be able to push his agenda. After a burst of productivity growth in 3Q and 4Q last year, productivity has been weak for two quarters in a row and is likely weak this quarter. This suggests the Fed has more dirty work to do in pushing inflation lower. The war is clearly having more impact on inflation than on growth and oil prices are likely to come down slowly if the Strait is reopening. The trimmed mean PCE is the only measure of core inflation that is close to the target. Finally, there is a growing risk of inflation expectations “unanchoring” higher.

Like Ken Rogoff, the markets hope for a hawkish leaning Fed Chair, but are justifiably worried about Warsh’s dovish message. I think Warsh will try to take a low profile at the June FOMC meeting, as he enjoys his honeymoon. However, I’m very worried if he does not accept the growing hawkishness of his committee. There is plenty of upside risk to bond yields.

Ethan Harris

AuthorMore in Author Profile »Ethan Harris has a Ph.D. in Economics from Columbia University and was the Head of the Domestic Research Division at the NY Fed. He was Chief US Economist at Lehman Brothers from 1996 to 2008 and Head of Global Economics at Bank of America from 2009 to 2023. Currently he is the author of the blog Ethan on the Economy.