India: Strong Growth, Fragile Balance

|in:Viewpoints

India’s economic performance in 2025 exceeded expectations across the board. During our recent visit to Mumbai, nearly all contacts expressed surprise at the economy’s resilience. Despite the disruption from Trump’s tariff measures—under which Indian exports faced duties of up to 50% until an interim agreement was reached in February 2026—India still expanded by 7.6% in 2025, an improvement on 7.1% in 2024.

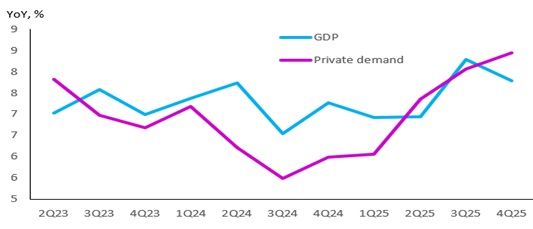

Growth did soften marginally in the final quarter, easing to 7.8% YoY from 8.3% YoY, largely due to weaker net exports. However, the more important takeaway for a domestically driven economy is that private demand strengthened (Figure 1). Consumption-led growth remained robust, and while export growth slowed, import volumes—a leading indicator of domestic demand—picked up significantly.

Figure 1: India GDP and private demand

Source: Have Analytics & Westbourne Research

India also made notable progress on inflation. Headline consumer price inflation fell sharply from above 5% year-on-year in December 2024 to just 1.1% by December 2025. This paved the way for the Reserve Bank of India to cut policy rates by 125 bps.

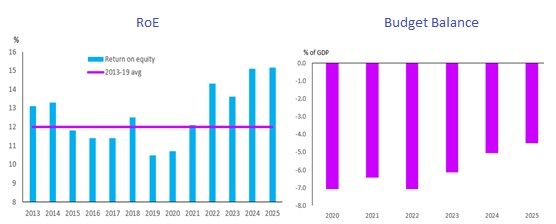

Corporate performance has been equally encouraging (Chart 1, Figure 2). Strong domestic demand has driven profitability higher, with average return on equity (RoE) for listed companies rising to 15.2%, well above the pre-pandemic average of around 12%. This suggests that the corporate profit cycle remains firmly in an upswing.

Public finances have also improved (Chart 2, Figure 2). The fiscal deficit narrowed for the third consecutive year, falling to 4.5% of GDP, while public debt has stabilised at around 56% of GDP, supported by strong nominal growth. Together, these factors paint a picture of an economy with solid macroeconomic fundamentals.

Figure 2: Corporate profits and public finances

Source: Bloomberg, Haver Analytics & Westbourne Research

Precariously Balanced

Yet beneath this strong performance lies a more fragile reality.

India’s growth model is becoming increasingly imbalanced. A sustained rebound in private investment remains elusive, and the country risks falling behind in emerging sectors such as artificial intelligence and next-generation manufacturing.

Traditional capital-intensive industries remain cautious following the boom-and-bust cycle of the mid-2000s. Many firms are still reluctant to commit to large-scale domestic investment and are increasingly looking overseas for expansion. Structural headwinds—including Chinese overcapacity, intense global competition, and regulatory uncertainty—continue to weigh on sectors such as steel, petrochemicals, and engineering procurement and construction (EPC).

At the same time, smaller firms are being squeezed as large conglomerates—such as Reliance, Tata, and Adani—expand aggressively into consumer-facing sectors. While corporate credit growth has picked up, it is largely being used for working capital rather than new capital expenditure.

The government’s flagship Production Linked Incentive (PLI) scheme has delivered mixed results. While it has succeeded in attracting investment in select sectors, its broader impact on private investment has been limited. Where investment is taking place—particularly in semiconductors, renewables, and data centres—it is not yet sufficient to offset weakness in traditional industries.

As a result, public investment continues to do the heavy lifting. Infrastructure spending has risen sharply since the pandemic and is set to reach a record US$133 bn (around 3.7% of GDP) in FY27, covering sectors such as transport, energy, and urban infrastructure.

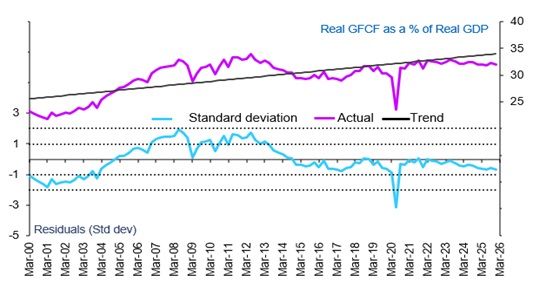

However, public investment alone cannot fully compensate for weak private sector participation. The share of private corporate investment in total national fixed investment has declined, while the share of government spending has increased. This has deepened the investment cycle downswing (Figure 3).

Figure 3: Investment cycle

Source: Haver Analytics & Westbourne Research

Concerns around governance and execution further complicate the outlook. Public-private partnership (PPP) models remain unattractive due to issues around risk allocation, delays, and uncertain returns. Some market participants also point to growing centralisation of decision-making, with project allocation increasingly influenced by the central government—reinforcing the dominance of large corporate groups.

China Factor and Industrial Strategy

China continues to exert a dual influence on India’s industrial landscape. On one hand, Chinese overcapacity discourages domestic investment in globally exposed sectors. On the other, India remains dependent on Chinese imports and expertise in areas such as EPC execution and low-cost components.

Looking ahead, Prime Minister Narendra Modi has set an ambitious target to raise manufacturing’s share of GDP from around 16–17% to 25% over the next decade. This vision is supported by the PLI scheme and a series of trade agreements aimed at integrating India into global supply chains.

There are some early successes. Emerging sectors—including electronics, electric vehicles, solar photovoltaics, and defence—are seeing stronger investment momentum. The electronics PLI scheme, in particular, has been effective. India now assembles all iPhone 17 models, accounting for roughly 25% of global iPhone production. However, this remains the exception rather than the rule.

Consumption: Strong but Questionable

With investment weak, consumption remains the primary driver of growth. Household spending ended 2025 on a strong note, growing by 8.4% YoY.

Rural households have been central to this momentum. Real rural incomes have outpaced urban incomes, supported by a shift toward non-agricultural activities. Non-farm income now accounts for over 50% of rural earnings and is growing faster than agricultural income.

By contrast, urban income growth has been constrained by job losses in manufacturing and IT, as well as slower wage growth in services. The rise of the gig economy—across e-commerce, food delivery, and transport—has not fully offset these pressures. Moreover, the share of regular salaried employment has declined to around 25%, dampening consumption stability.

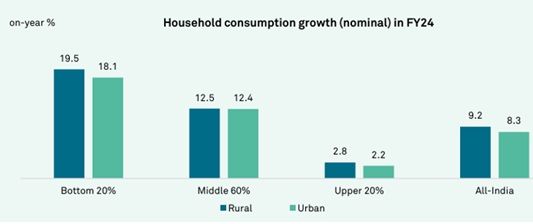

Rural consumption is now growing as fast as, or faster than, urban consumption across income groups (Figure 4). However, this strength is partly underpinned by fiscal support, raising questions about sustainability.

Figure 4: Consumption growth by income decile

Source: Crisil

Government transfers have expanded significantly. The number of states providing unconditional cash transfers has risen from 11 to 16 in recent years. Transfers to women and farmers have increased by over 36% since FY19, reaching approximately ₹2.6 trn (~0.7% of GDP). Additional support through food programmes and agricultural schemes further reinforces consumption.

Tax policy has also played a role. The September 2025 GST rationalisation reduced rates on mass consumption goods, including automobiles and consumer durables. While this has supported spending, its impact is likely to diminish over time.

In sum, India’s economy appears finely balanced. Growth is expected to moderate to around 7% in FY27, down from 7.6% in FY26, as the effects of fiscal support fade and investment remains subdued. Inflation dynamics and external risks may also limit further monetary easing, with the Reserve Bank of India likely to remain on hold or potentially tighten if conditions warrant.

Investment Implications

Against this backdrop, we are shifting our stance on Indian equities from overweight to neutral.

While macro fundamentals remain solid, the lack of investment momentum and questions around consumption sustainability warrant caution. That said, structural shifts—particularly in rural incomes and consumption patterns—create selective opportunities.

We favour sectors leveraged to domestic demand, structural change and public infrastructure spending, including: • Fast-moving consumer goods (FMCG) • E-commerce • Healthcare • Airlines • Cement

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.