Inflation – Debt Default by Another Name

|in:Viewpoints

The Congressional Budget Office (CBO) projects large federal budget deficits, in absolute as well as relative terms, as far as the eye can see. This, by definition, means continued increases in the federal debt, again in both absolute and relative terms. The CBO forecasts that the levels of interest rates across the maturity spectrum over the next 10 years will be approximately where they are currently. My “forecast” is that the levels of interest rates, especially in the longer maturities will be higher than the CBO’s forecast. Be that as it may, the CBO projects that net interest on the federal debt will rise inexorably over the next 10 years. Given that Social Security, Medicare, Medicaid and defense expenditures are projected to dominate federal outlays excluding interest on the debt, there is little room for the federal government to slow the growth in federal spending without precipitating a walker-aided march on Washington, DC. By the way, it is projected by the Social Security Administration that its “trust” fund for old-age benefits will be exhausted by 2036. This means that all else the same, benefit payments to then current recipients will have to be cut. Do you really think “all else will be the same”? I think there will be a change in the law allowing the Treasury to borrow more to allow Social Security to maintain its “promised” benefits. Increasing taxes in a meaningful way appears to be politically unfeasible. Under these circumstances, I believe that the federal government, with “cooperation” from the Federal Reserve will attempt to inflate away its federal debt/debt-servicing challenges. It will do this by the Treasury purposely shortening the maturity structure of the federal debt and inducing the Federal Reserve, which dominates the level of short-maturity interest rates, to maintain the federal funds rate at a below-equilibrium level. This will result in a steepening in the yield curve, with the level of longer-maturity interest rates increasing relative to the federal funds rate as well in absolute terms. This will be accompanied by faster growth in the credit created by the Federal Reserve and the depository institution system, i.e., credit created, figuratively, out of thin-air (drink). In turn, this faster growth in “thin-air” credit will result in higher inflation.

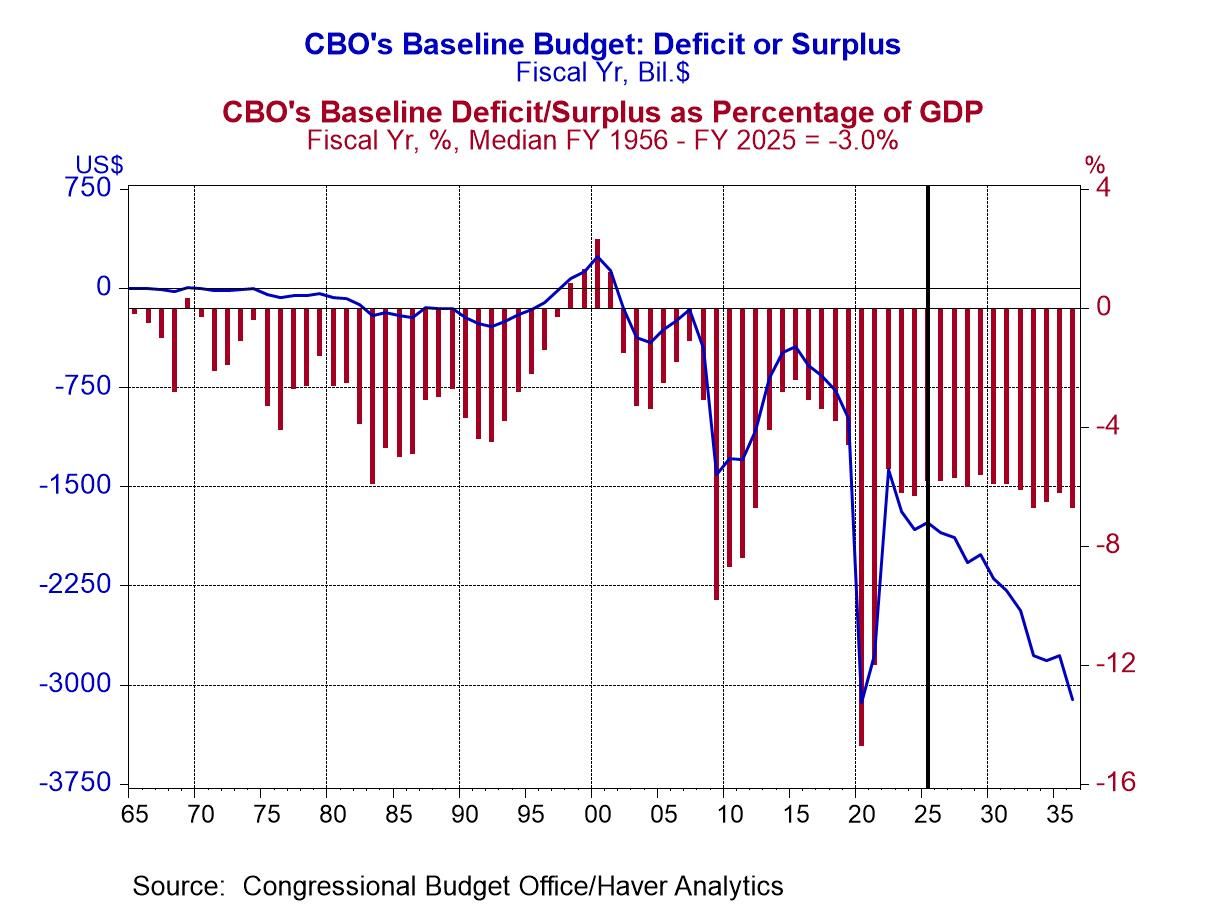

Plotted in Chart 1 are fiscal-year observations of federal budget deficits (-)/surpluses (+) in absolute terms (blue line) and relative to nominal GDP (red bars). Historical data run from FY 1965 through FY 2025 and CBO projections are from FY 2026 through FY 2036. By FY 2036, the CBO projects that the federal budget deficit will be $3.1 trillion, compared with $1.8 trillion in FY 2025. As a percent of GDP, CBO projects the budget deficit in FY 2036 to be -6.7% compared with a median of -3.0% for fiscal years 1965 through 2025.

Chart 1

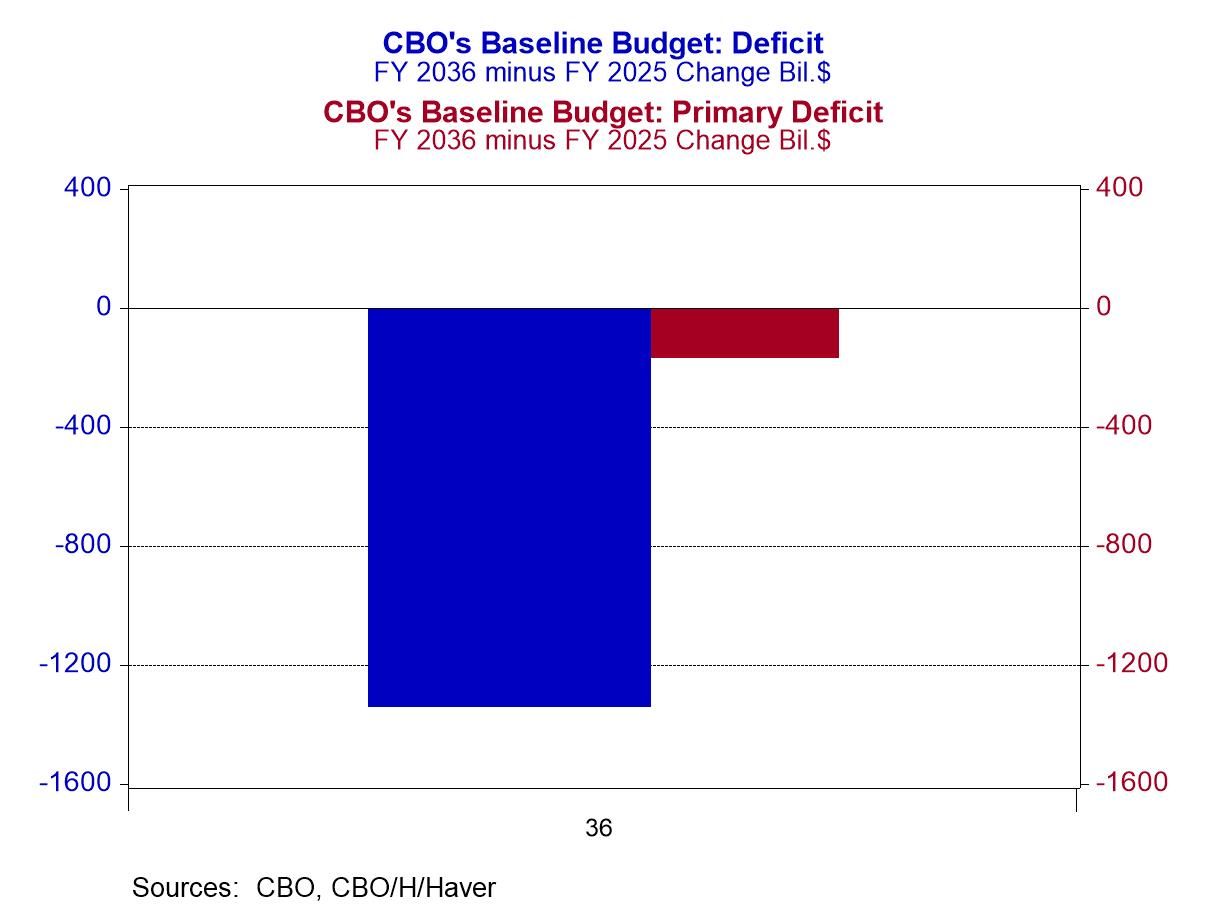

As shown in Chart 2, the CBO projects that the overall federal budget deficit will widen by about $1.3 trillion from FY 2025 to FY 2036 (the blue bar). But the deficit excluding interest payments on the federal deficit, known as the primary deficit, is projected to increase by about only $0.2 trillion in this same period. Thus, we can deduce that principal driver of widening federal budget deficits in the coming years is interest on the debt.

Chart 2

Subsequent to February 11, 2026, when the CBO issued its baseline projections the Supreme Court ruled that some of the tariffs that had been imposed by the Trump administration were unconstitutional. Thus, all else the same, projected federal revenues would be smaller than what was assumed in the CBO’s baseline projections. And thus, all else the same, the projected deficits would be larger. Moreover, the CBO’s baseline projections of revenues assume that some of the current tax breaks will expire during the projection period. Perhaps. But if these tax breaks are maintained, the CBO’s baseline projection of revenues will turn out to be too high. Also, when the CBO made its baseline-budget projections, military operations had not occurred in the Persian-Gulf area. The CBO projected that defense outlays in FY 2026 would be $904.4 billion, down from actual $953.8 billion in FY 2025. The Pentagon has requested a $1.5 trillion budget for FY 2027. This compares with the CBO’s baseline projection of $920.7 billion for defense outlays in FY 2027. Given the increased cost of US military operations so far in FY 2026 and the likely higher-than-projected defense expenditures in FY 2027 to replace spent weapons, the CBO’s February 2026 baseline projections of defense expenditures would appear to be too low. All else the same, then, the CBO’s baseline projections of deficits also would appear to be too low due to higher-than-projected defense expenditures.

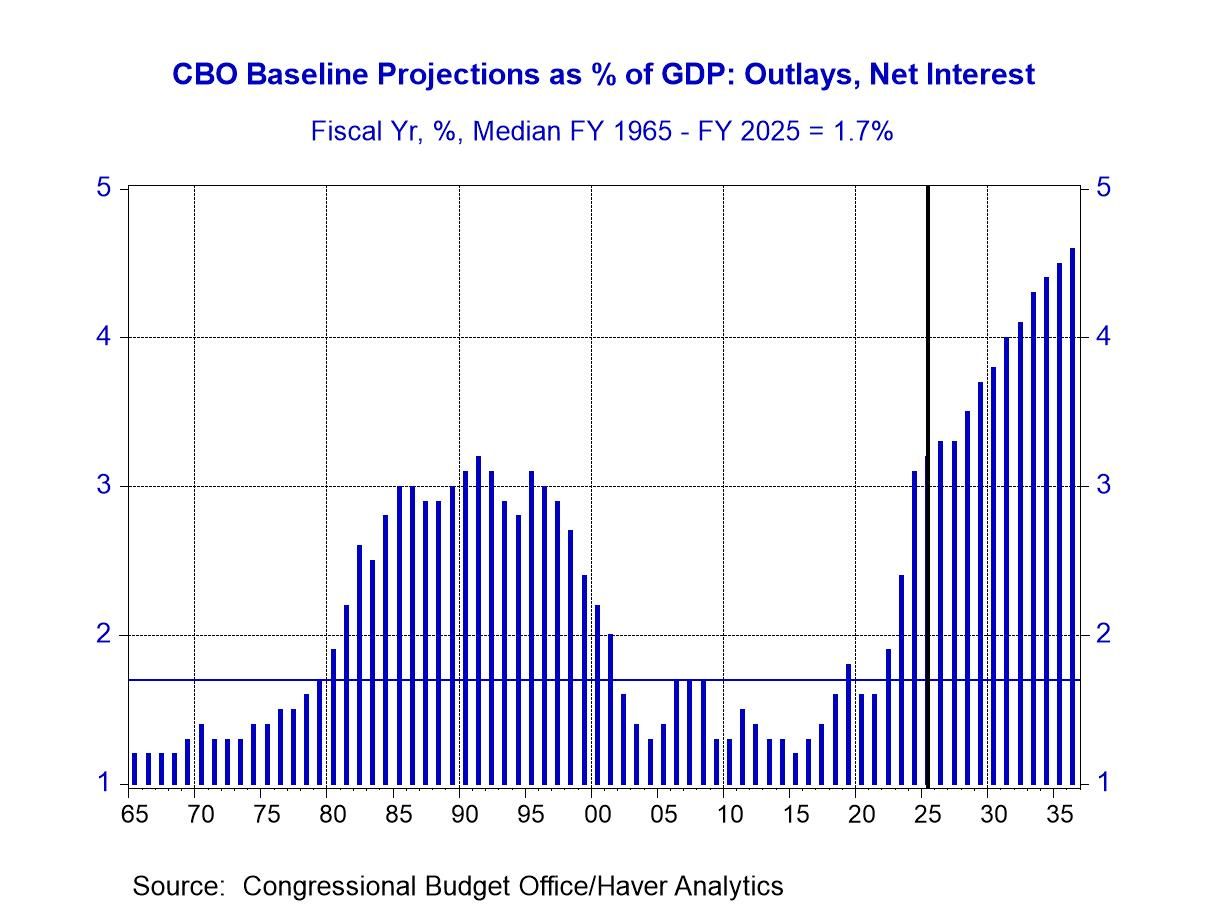

Plotted in Chart 3 are the fiscal year federal interest outlays as a percent of nominal GDP. From FY 1956 through FY 2025, the median value of federal interest expense as a percent of nominal GDP was 1.7%. In FY 2025, the value was 3.2%. The CBO projects that federal interest outlays as a percent of nominal GDP will reach 4.6% in FY 2036.

Chart 3

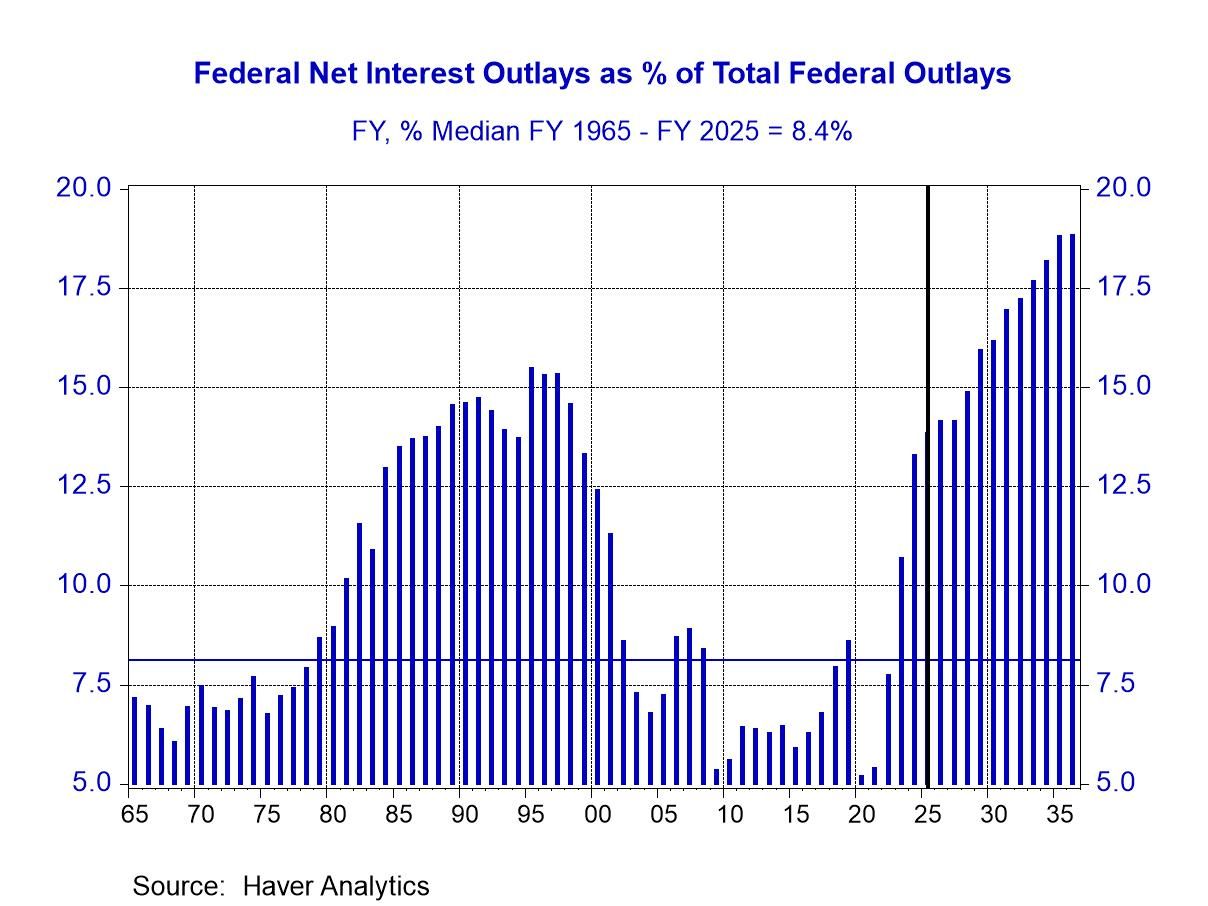

Plotted in Chart 4 are the fiscal year observations of federal net interest outlays as a percent of total federal outlays. The median value of this from FY 1965 through FY 2025 was 8.4%. In FY 2025, this value was 13.8%. The CBO projects that federal net interest outlays as a percent of total federal outlays will climb to 18.8% in FY 2036.

Chart 4

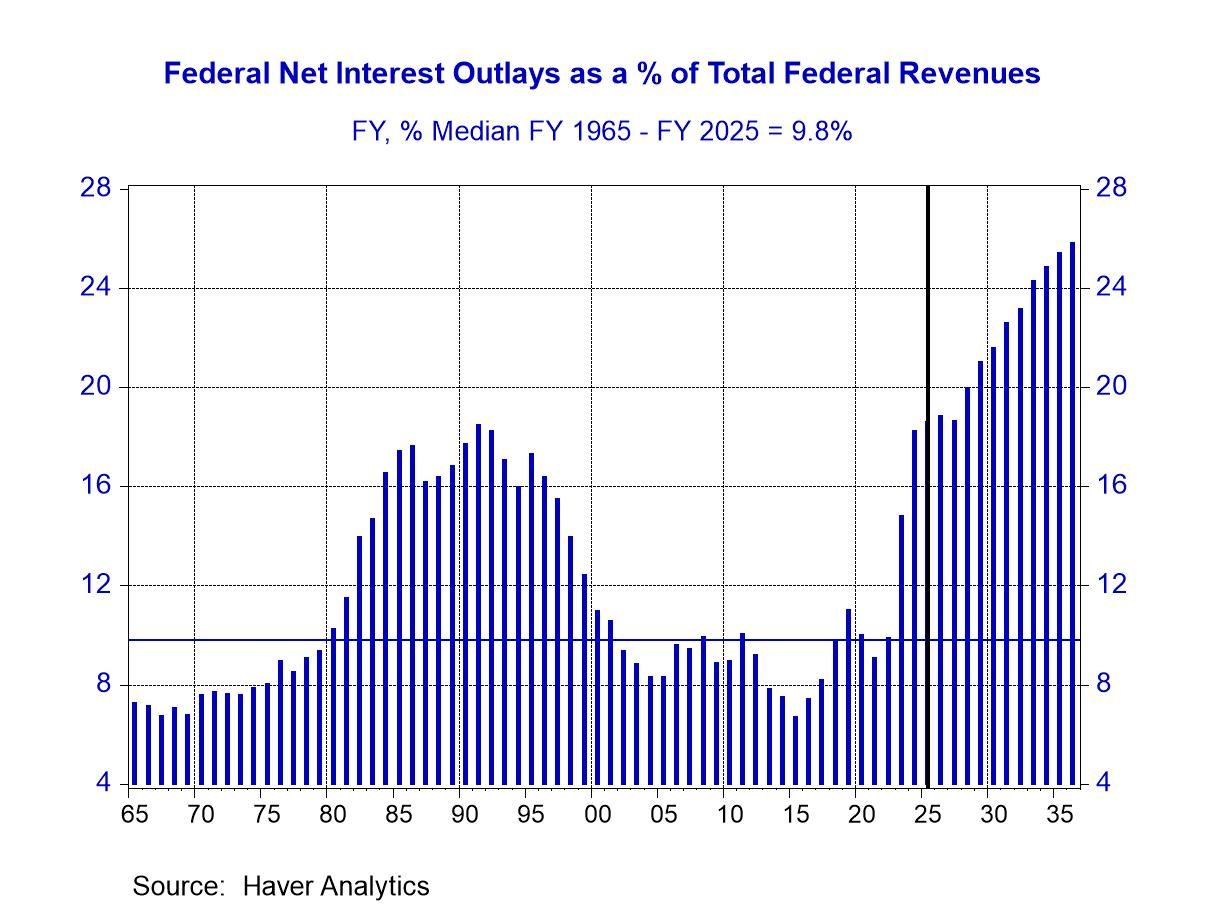

Plotted in Chart 5 are the fiscal year observations of federal net interest outlays as a percent of total federal revenues. The median value of net federal interest outlays as a percent of total federal revenues from FY 1965 through FY 2025 was 9.8%. The value in FY 2025 was 18.6%. The CBO projects that this value will climb to 25.8% in FY 2036. So, by FY 2036, the CBO reckons that one-quarter of total federal revenues will be “dedicated” to paying the interest on the federal debt.

Chart 5

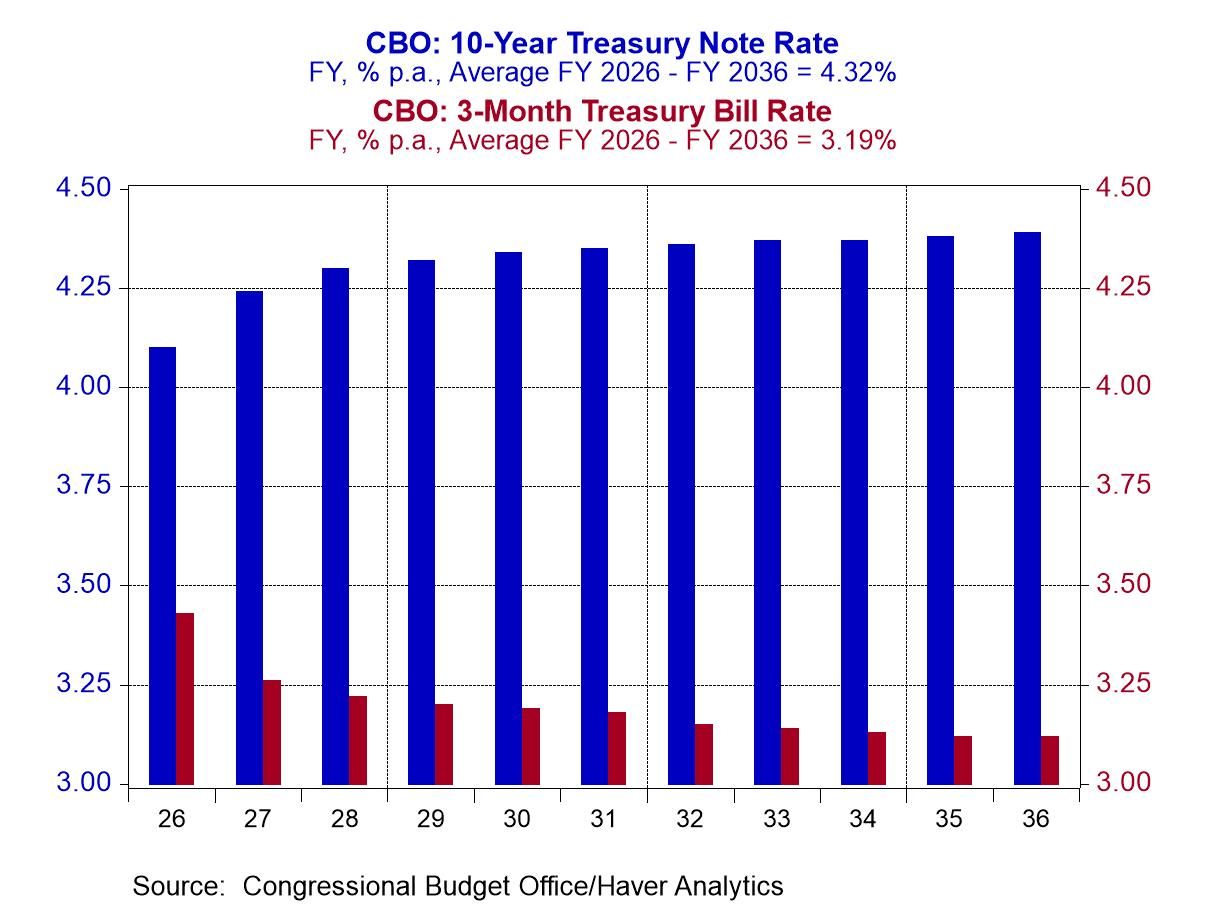

Among other things, the CBO’s baseline projection of federal net interest outlays depends on its projection of interest rates. Plotted in Chart 6 are the CBO’s fiscal-year projections of the interest rates on the 3-month Treasury bills and the 10-year Treasury security for FY 2026 through FY 2036. The average projected interest rate on the 10-year Treasury security over this period is 4.32%; for the 3-month Treasury bill, 3.19%. For some perspective, on Friday, May 1, 2026, the Treasury constant-maturity 10-year security ended the day at a yield of 4.39%; the 3-month constant maturity security at a yield of 3.68% (Source: Federal Reserve H.15 report). So, the CBO is projecting that for-close-enough-for-government work that over the next 11 fiscal years the average yield on the 10-year Treasury security will be little changed from its May 1, 2026 level and the average yield on a 3-month Treasury security will fall from its May 1, 2026 level by almost 50 basis points.

Chart 6

If interest rates should turn out to be higher, all else the same, the Treasury’s net interest outlays would turn out to be even higher than what the CBO is projecting. If there were only some way to guarantee that net interest outlays do not explode even if the amount of Treasury debt does. It turns out there is a way. It goes by the name of “fiscal dominance”. In essence, the central bank (in the US, the Federal Reserve) becomes subservient to the fiscal authority (the US Treasury). That is, the central bank’s primary responsibility is to use its monetary-policy tools, not to keep inflation in check, but rather to contribute to the orderly debt financing of the central government.

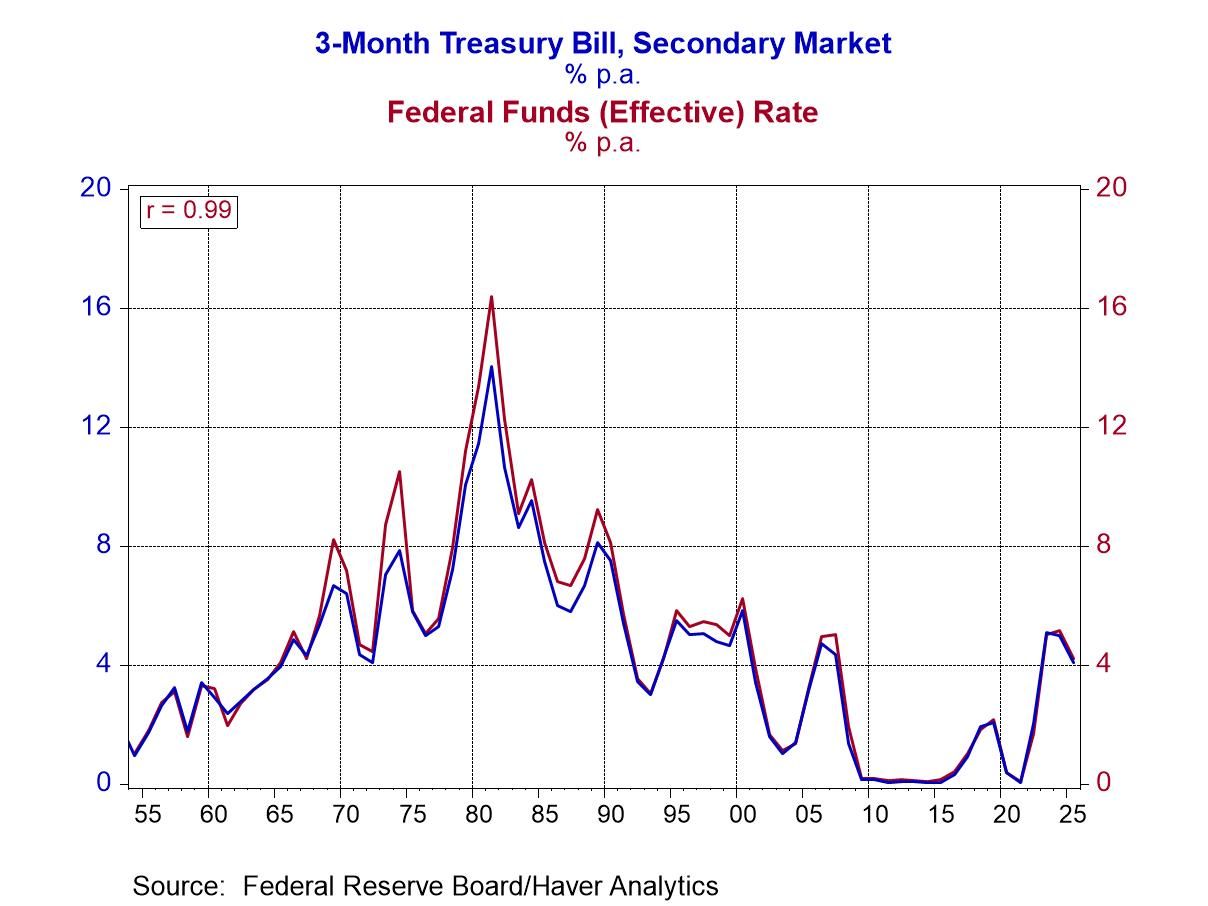

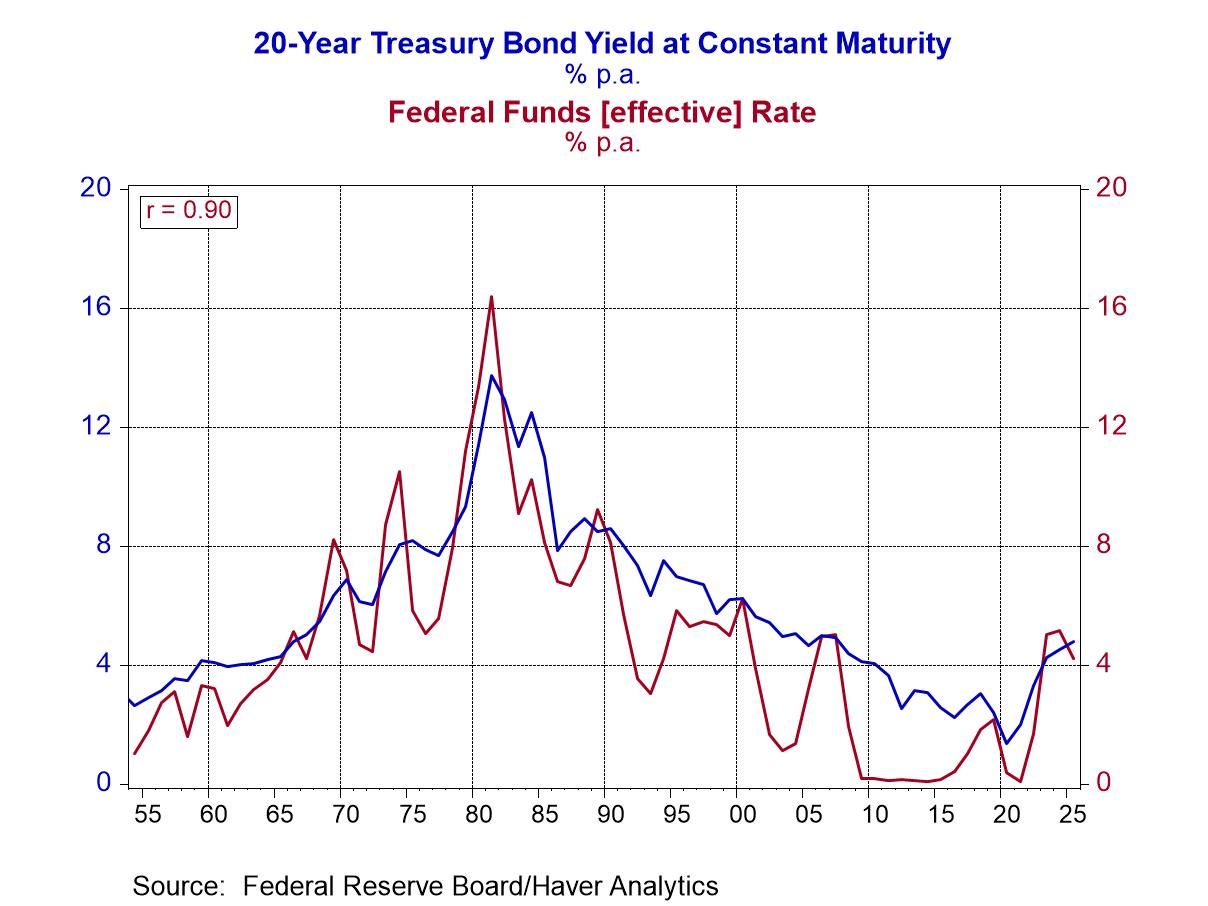

How might fiscal dominance be implemented in the US? Because the Federal Reserve has a monopoly on the creation/destruction of reserves held by depository institutions, the interest rate over which the Fed has the most control is the federal funds rate – the rate at which reserves are traded among depository institutions. If the fed funds rate is trading above the level desired by the Fed, the Fed can create more reserves in order to bring the fed funds rate back down to the Fed’s desired level. Conversely, if the fed funds rate is trading below the level desired by the Fed, the Fed can drain reserves in order to bring the fed funds rate back up to the Fed’s desired level. The federal funds rate has a maturity of one day. Shorter-maturity interest rates on Treasury securities are most influenced by the level of the federal funds rate. As shown in Chart 7, the correlation between the level of the 3-month Treasury bill rate and the level of the fed funds rate was 0.99 using annual average data from 1954 through 2025. Recall that a correlation coefficient of 1.00 means that two series are perfectly correlated. As shown in Chart 8, the correlation coefficient declines to 0.90 when the fed funds rate is compared to the yield on a 20-year Treasury security. A correlation coefficient of 0.90 is nothing to sneeze at, but the point is that the level of the fed funds rate is most closely associated with the level of the 3-month Treasury bill rate.

Chart 7

Chart 8

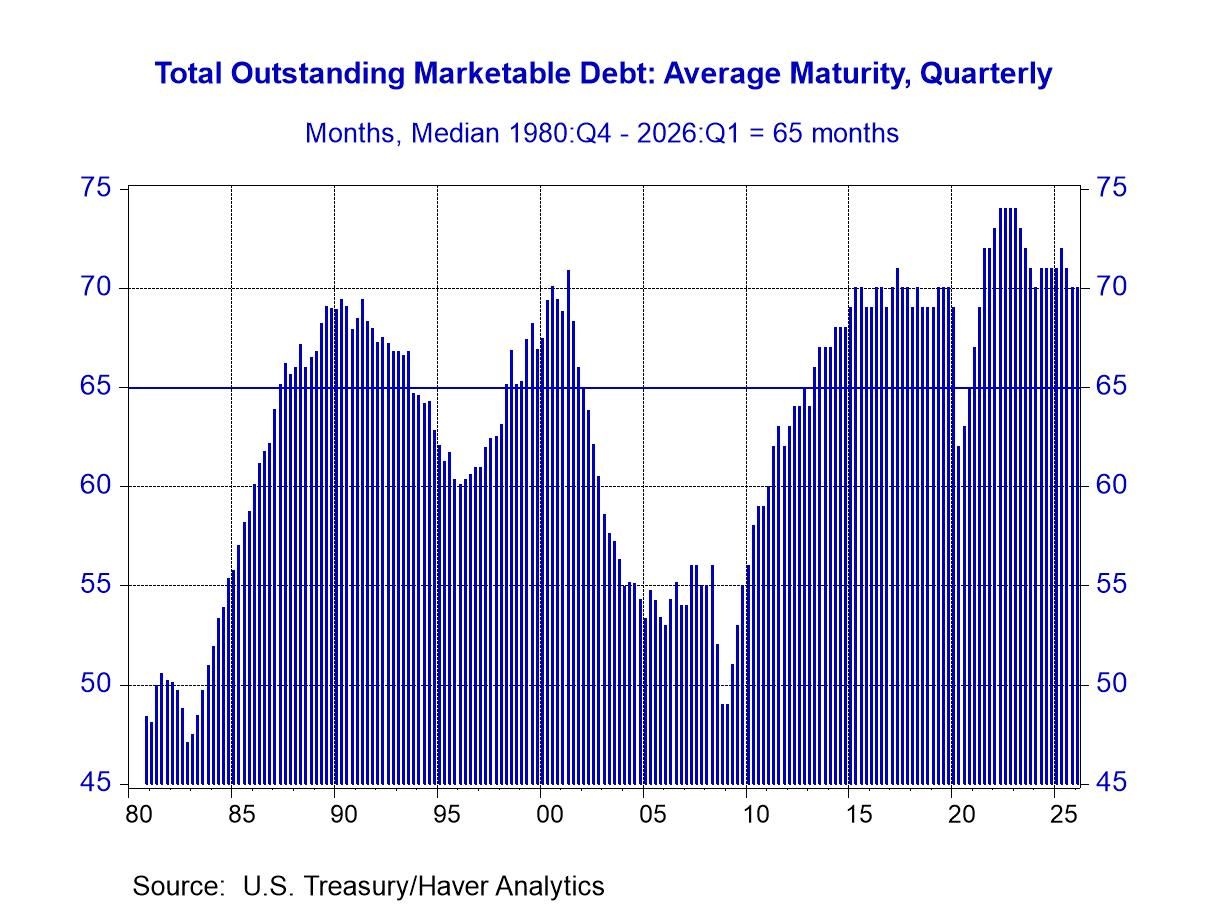

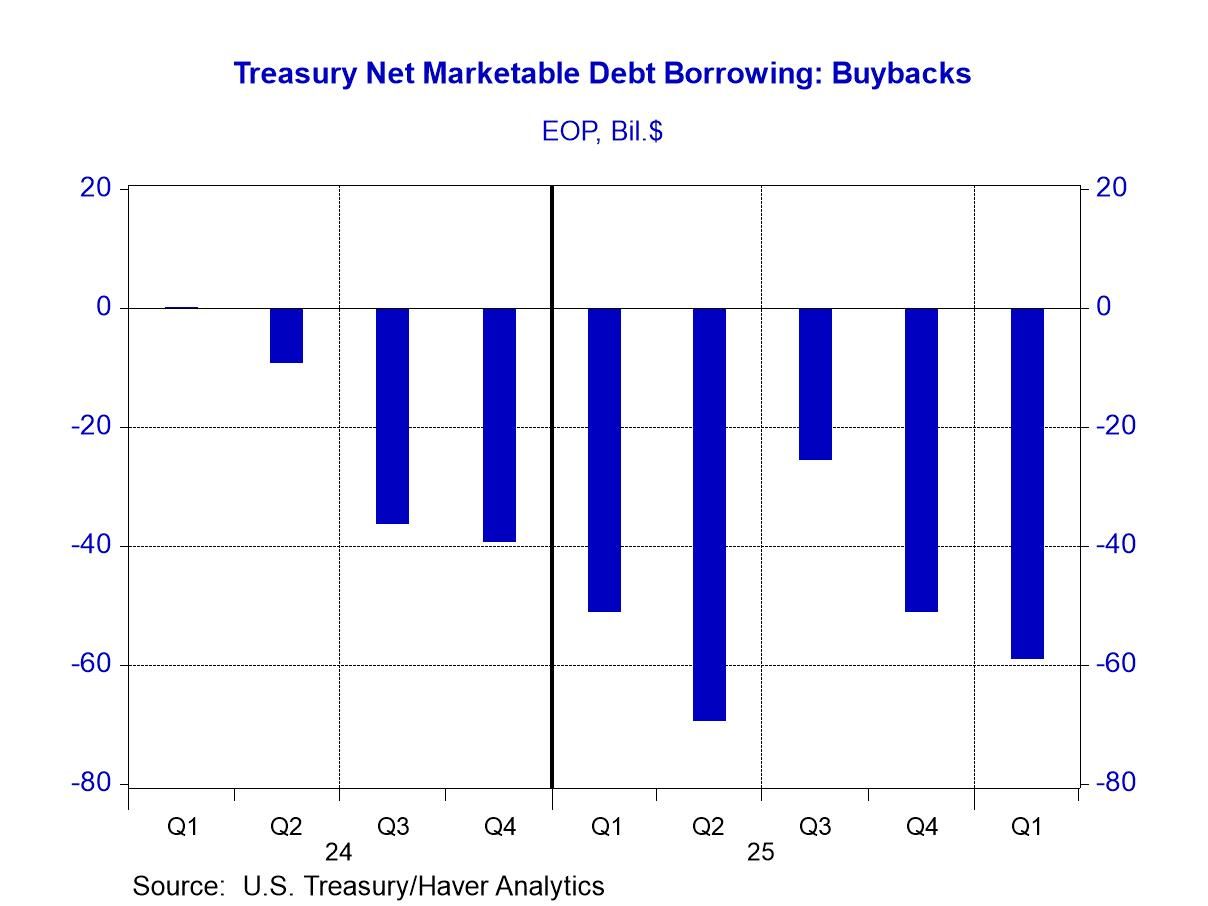

All right, what does this have to with fiscal dominance? If the Treasury can reduce the maturity of its outstanding debt and the Federal Reserve can be induced to maintain a low fed funds rate, then the debt-servicing costs of the Treasury can be mitigated. As shown in Chart 9, the average maturity of the outstanding marketable Treasury debt in 2026:Q1 was 70 months (5.8 years). This compares with the median average maturity of 65 months (5.4 years) for the period Q4:1980 through Q1:2026. Treasury Secretary Bessent aims to reduce the average maturity of Treasury debt. The Treasury started engaging in buybacks of longer-maturity Treasury debt in 2024 and has continued to do so in larger quantities through 2026:Q1 (see Chart 10), funding these buybacks with shorter-maturity debt.

Chart 9

Chart 10

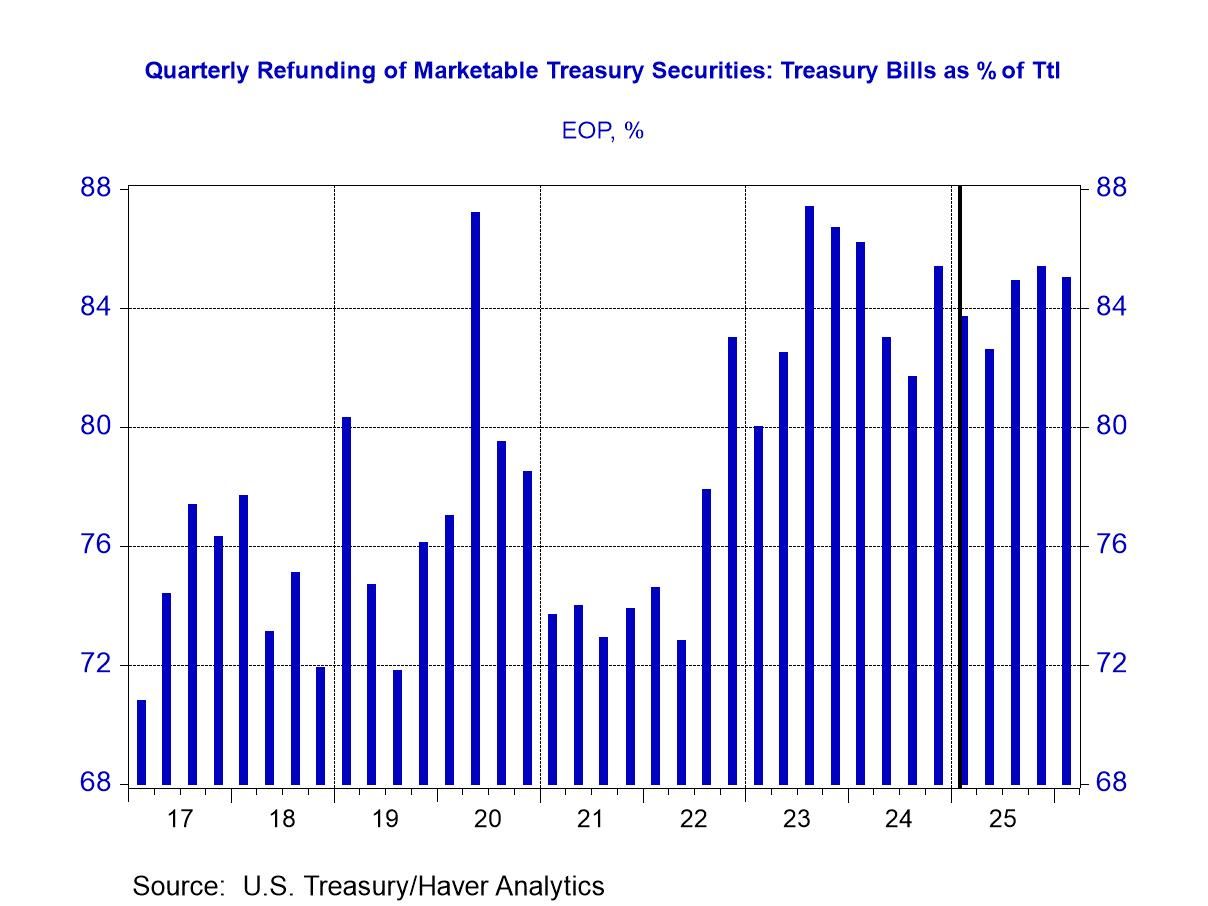

Treasury Secretary Yellen in the Biden administration was criticized for favoring issuance of short-maturity Treasury bills over longer-maturity Treasury notes and bonds. Soon-to-be Treasury Secretary Bessent was among these critics, claiming that issuing relatively more Treasury bills versus Treasury notes and bonds was a deliberate attempt to hold down the level of longer-term interest rates. Secretary Yellen was accused of “gaming” the fixed-income market. And indeed, as shown in Chart 11, starting in late 2022, Treasury bill issuance as a percent of total quarterly Treasury securities issuance did move up. Now that he is the Secretary of the Treasury, Scott Bessent has maintained the Yellen debt-management policy of Treasury bills “mostly”. Moreover, Secretary Bessent has championed the issuance of Stablecoin in order to increase the demand for Treasury bills.

Chart 11

As an aside, Stablecoin is a type of crypto currency that “promises” to pay back the holder at par on demand. The issuers of Stablecoin take in purchasers’ dollars and buy Treasury bills, among other types of investments, collecting the interest. It still is not clear to me why someone would purchase Stablecoin, forgoing the interest, when they could purchase shares in a government-only money market funds and collect the interest. Is the Stablecoin “guarantee” of redemption on demand at par any better than that of a government-only money market fund? The one advantage I do see in investing in Stablecoin over a government-only money fund is that illegal transactions are easier to mask with Stablecoin.

But I digress. I would suspect that a person as well-versed in financial theory as Secretary Bessent is aware that the preponderance of research indicates that the shape of the yield curve, that is, the relationship between the levels longer-maturity interest rates and the levels of shorter-maturity interest rates is not a function of the relative supplies of the maturities, but rather of market expectations of the future levels of short-maturity interest rates. So, although hedge-fund manager Bessent accused then Secretary Yellen of trying to hold down the levels of longer-maturity interest rates by issuing relatively more Treasury bills, I do not believe that this is the motive for now Treasury Secretary Bessent’s attempt to shorten the maturity of the public debt. Rather, I suspect his motive is to mitigate future debt-servicing costs by inducing the Federal Reserve to hold down the level of the federal funds rate.

If the Federal Reserve maintains too low a federal funds rate, goods/price inflation is bound to increase. So, with mounting federal debt, the Treasury can avoid formal default on its debt but rather, default by another name – inflation. If the maturity structure of the debt is sufficiently shortened and the Federal Reserve can be induced to hold down the level of the fed funds rate, debt-servicing costs can be mitigated and the real value of the debt can be reduced via higher inflation. Yes, The Mandibles, by Lionel Shriver is fiction. But is it also prescient?

Paul L. Kasriel

AuthorMore in Author Profile »Mr. Kasriel is founder of Econtrarian, LLC, an economic-analysis consulting firm. Paul’s economic commentaries can be read on his blog, The Econtrarian. After 25 years of employment at The Northern Trust Company of Chicago, Paul retired from the chief economist position at the end of April 2012. Prior to joining The Northern Trust Company in August 1986, Paul was on the official staff of the Federal Reserve Bank of Chicago in the economic research department. Paul is a recipient of the annual Lawrence R. Klein award for the most accurate economic forecast over a four-year period among the approximately 50 participants in the Blue Chip Economic Indicators forecast survey. In January 2009, both The Wall Street Journal and Forbes cited Paul as one of the few economists who identified early on the formation of the housing bubble and the economic and financial market havoc that would ensue after the bubble inevitably burst. Under Paul’s leadership, The Northern Trust’s economic website was ranked in the top ten “most interesting” by The Wall Street Journal. Paul is the co-author of a book entitled Seven Indicators That Move Markets (McGraw-Hill, 2002). Paul resides on the beautiful peninsula of Door County, Wisconsin where he sails his salty 1967 Pearson Commander 26, sings in a community choir and struggles to learn how to play the bass guitar (actually the bass ukulele). Paul can be contacted by email at econtrarian@gmail.com or by telephone at 1-920-559-0375.