Kevin Hassett Is Right, For Once?

|in:Viewpoints

Grinnin’ Kevin Hassett, a White House economic adviser, said on Fox Business on May 6, 2026: “Credit card spending is through the roof. They’re [households] spending more on gasoline, but they’re spending more on everything else, too.” Hassett went on to say that the spending surge was due to households having “so much more money in their pockets”. Well, if households are running up their credit card balances, yes, they temporarily have “more money in their pockets”. Although Hassett thinks that this is a good thing, I see it as a reason why the increase in energy prices will seep into the prices of non-energy goods and services.

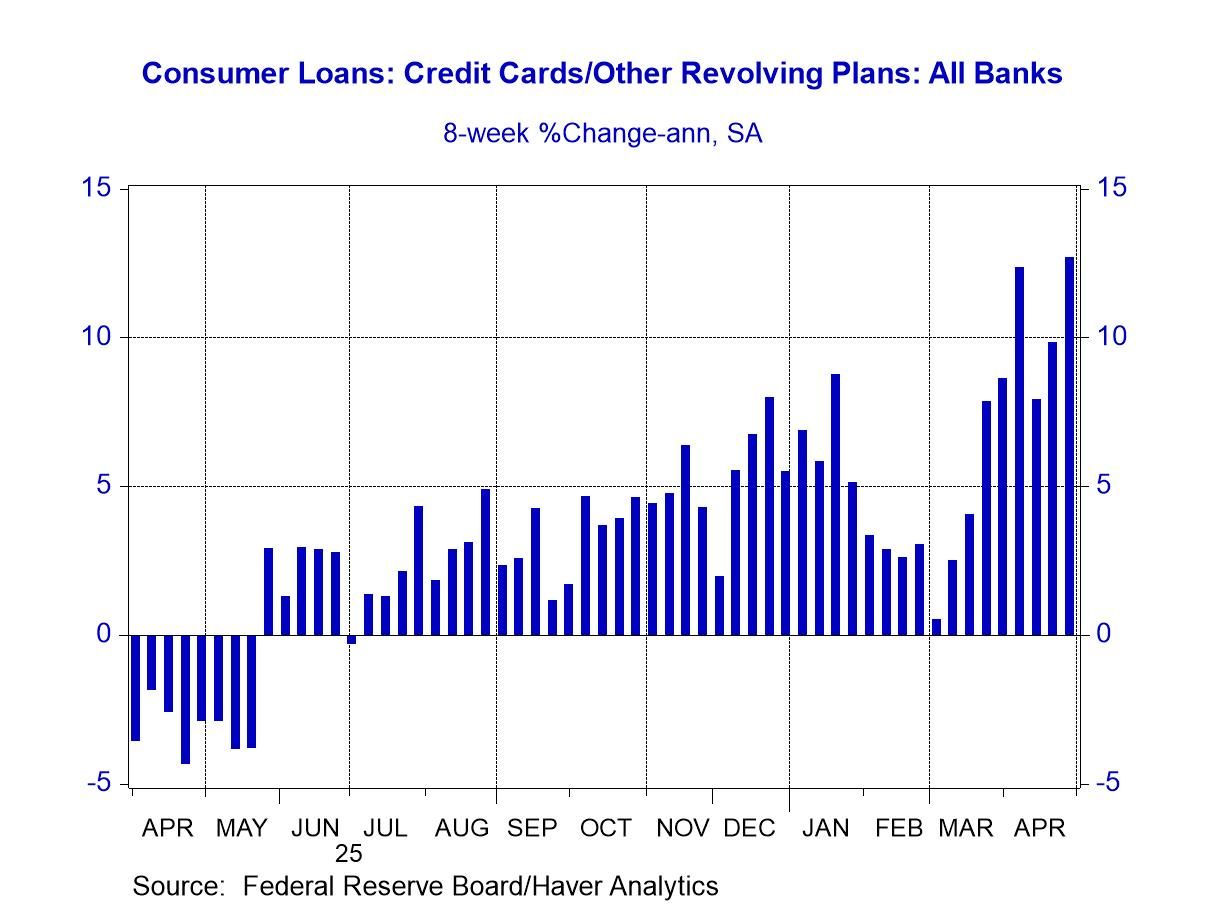

Let’s look at some data that are consistent with Hassett’s credit-card spending hypothesis. Plotted in the chart below are the observations of the eight-week annualized percent changes in commercial bank credit card and other revolving loans. In the eight weeks ended April 29, these loans grew at an annualized pace of 12.7%. So, this is consistent with Hassett’s happy hypothesis about households running up their credit card balances.

But Hassett might not be grinnin’ so much if the higher energy prices start to be associated with higher prices for other goods and services. Why might this occur with the increase in household credit card borrowing? If households did not increase their credit card borrowing, all else the same, they would have to cut back on their nominal purchases of non-energy goods and services as they spend more of their nominal income on higher-priced energy goods and services. Sellers of non-energy goods and services would try to pass on their higher costs of production due to higher energy prices. But again, if households did not increase their credit card borrowing, they would have less nominal income left over to purchase non-energy goods and services. With a decline in the demand for non-energy goods and services, sellers of these would have difficulty passing on their higher energy costs of production. This would keep the prices of non-energy goods and services from rising.

But, if households maintain their nominal purchases of non-energy goods and services along with their higher nominal purchases of increased-price energy goods and services by running up the credit card balances, then the prices of non-energy goods and services need not remain the same. These prices would go up as sellers of these non-energy goods and services are able to pass on their higher energy costs of production. In sum, by households increasing their nominal spending in the face of higher energy prices by running up their credit card balances, not only will energy prices go up, but so, too, will the prices on non-energy goods and services.

Why do I say in the title of this commentary that Kevin Hassett is right for once? In September 1999, Hassett and his co-author, James Glassman, published a book entitled Dow 36,000: The New Strategy for Profiting From the Coming Rise in the Stock Market. The authors believed that the US equity market was significantly undervalued and would rise in value dramatically. At the end of September 1999, the Dow Jones 30 Industrial Stock Index closed at 10,337. In September 2009, the Dow closed at 9,712. The Dow did not hit 36,000 until December 2021. Hassett and Glassman followed the forecasting rule that if you forecast a number, don’t give a date associated with the forecast number. So, to be fair, to Hassett, he was not wrong. The Dow eventually did hit 36,000. All right, turn about is fair play. Hassett can remind me of one of my errant forecasts.

Paul L. Kasriel

AuthorMore in Author Profile »Mr. Kasriel is founder of Econtrarian, LLC, an economic-analysis consulting firm. Paul’s economic commentaries can be read on his blog, The Econtrarian. After 25 years of employment at The Northern Trust Company of Chicago, Paul retired from the chief economist position at the end of April 2012. Prior to joining The Northern Trust Company in August 1986, Paul was on the official staff of the Federal Reserve Bank of Chicago in the economic research department. Paul is a recipient of the annual Lawrence R. Klein award for the most accurate economic forecast over a four-year period among the approximately 50 participants in the Blue Chip Economic Indicators forecast survey. In January 2009, both The Wall Street Journal and Forbes cited Paul as one of the few economists who identified early on the formation of the housing bubble and the economic and financial market havoc that would ensue after the bubble inevitably burst. Under Paul’s leadership, The Northern Trust’s economic website was ranked in the top ten “most interesting” by The Wall Street Journal. Paul is the co-author of a book entitled Seven Indicators That Move Markets (McGraw-Hill, 2002). Paul resides on the beautiful peninsula of Door County, Wisconsin where he sails his salty 1967 Pearson Commander 26, sings in a community choir and struggles to learn how to play the bass guitar (actually the bass ukulele). Paul can be contacted by email at econtrarian@gmail.com or by telephone at 1-920-559-0375.