Oil Price Spike: Temporary Boost to Inflation, but for How Long?

|in:Viewpoints

As is well known, the oil price spike is a negative supply shock that dents the real economy and generates a one-time rise in the general price level that temporarily raises the monthly inflation data but is not inflationary. How long are these temporary impacts expected to last? This depends largely on how long the oil prices stay high. But so far, the rapid responses of retail energy prices to the spike in crude oil prices suggest that the impact on the monthly inflation data will run their course quickly, in 2-3 months. The monthly inflation data should subsequently simmer down to their pre-Middle East conflict pace of increase, while the year-over-year percentage increases in measured inflation absorb the temporary bulge. If oil prices fall back to their pre-conflict $65/barrel, then the monthly changes will turn negative and the general price level will recede to the level its pre-conflict rate of increase would have taken it.

The oil price spike raises costs of energy, so consumers will spend more for energy products (historically, the demand is fairly price inelastic in the short run) and will have less to spend on non-energy goods and services. The oil price bulge and Middle East conflict has hit confidence and raised uncertainty (the University of Michigan consumer sentiment index fell sharply in its latest April meeting) and interest rates a bit. In addition, the higher energy costs will raise business operating costs, which may raise the prices of selected consumer products a bit. As a result, the oil price spike will generate a deceleration of nominal GDP. A larger portion of that aggregate demand will be inflation and a lower portion real.

The Fed properly recognized the oil price spike as a negative supply shock and wisely decided to keep monetary policy on hold at its March FOMC meeting. The Fed funds futures market expects the Fed will be on hold at its late April meeting, which is scheduled to be Chair Powell’s last. The Fed rarely admits mistakes, but it largely acknowledges that its accommodation of the oil price shocks of the 1979s contributed to persistently excess demand and dangerously high inflation and inflationary expectations and bond yields.

Two observations are important about the recent spike in oil prices. First, reflecting the U.S. shale revolution and surge in production of oil and natural gas, which has made the U.S. net energy independent in the aggregate (even though certain regions in the nation have regulations that constrain oil drilling and refining and distribution, forcing them to rely heavily on imported energy—particularly California), gasoline and other energy sources remain in ready supply—only at higher costs. That’s starkly different than the 1970s, when gasoline was scarce and rationed.

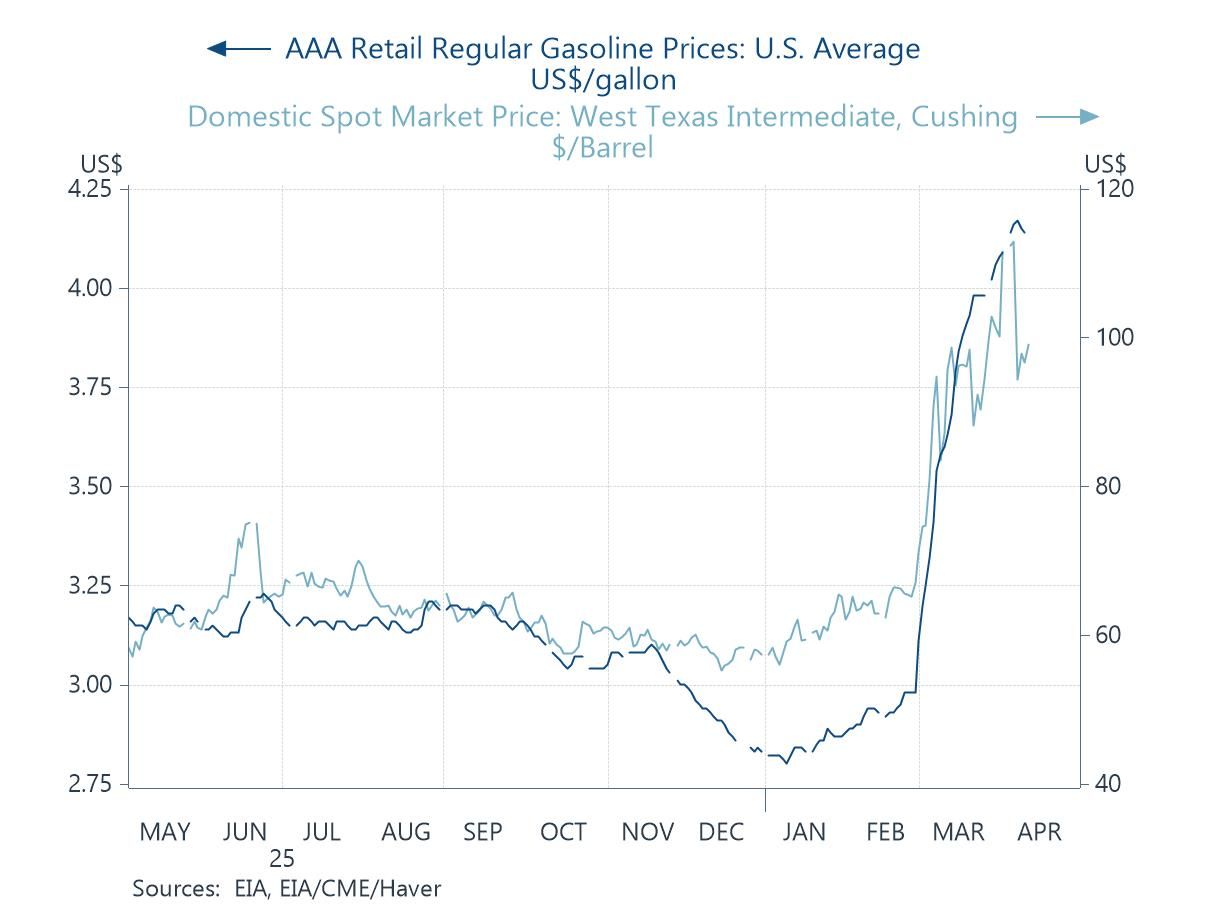

Second, retail energy prices have been adjusting quickly to the higher oil prices. As shown in Chart 1, through April 10, while oil prices have risen to $96.50/barrel from $65, a 48% increase, retail gasoline prices nationally have risen to $4.15/gallon, up from $2.97, a 40% rise. Before the Middle East conflict, there was backwardation in the oil price futures curve—the markets had priced in a gradual decline in oil prices from their then-current prices. (After the oil price surge, markets have priced in expectations that prices will fall back toward their earlier price level by later in 2026, but maintain a risk premium.) Prices of other refined oil products have risen even faster: diesel fuel have risen from $3.75/gallon to $5.68, a 51% increase.

Chart 1. WTI Oil and Retail Gasoline Prices

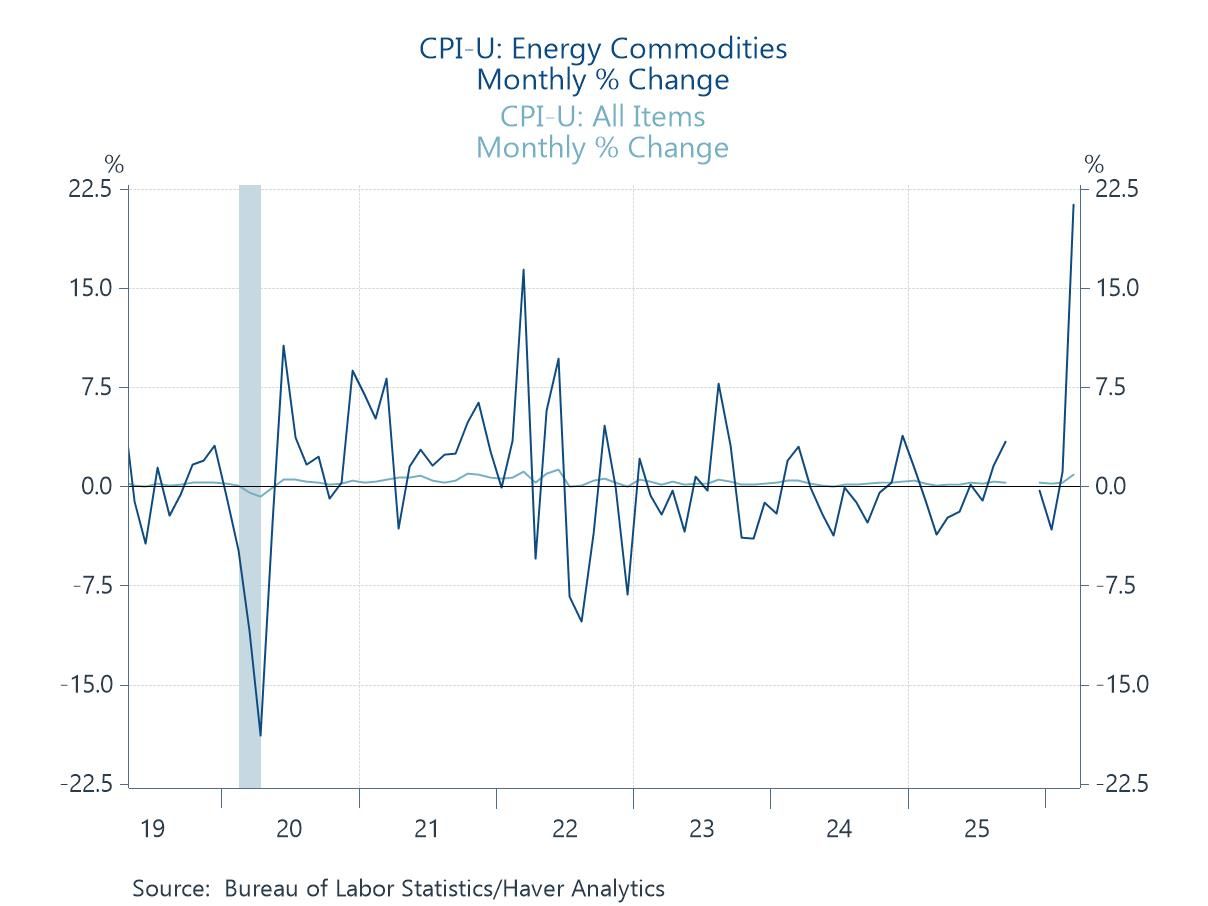

The CPI inflation jumped 0.9% in March, lifting its yr/yr rise to 3.3% from 2.4%, while the core PCI excluding food and energy rose only 0.2%, lifting its yr/yr to 2.6% from 2.5%. As shown in Chart 2, overall energy commodity prices in the CPI rose 21.3% in March. This is bigger than its largest monthly jump in 2022 when WTI oil prices spiked to a high of $125/barrel. The U.S. Bureau of Labor Statistics collects data for the CPI throughout the month, so another large increase is expected in April.

Chart 2. CPI Energy Commodities, monthly % chg

This dramatic rise in gasoline and diesel prices point to a very quick adjustment of retail prices. This suggests that the impact of the surge in crude prices on the CPI will be temporary, with the bulk of it in 2 months. I expect the residual impact will be relatively modest. Businesses will face some increases in operating costs, but the slowdown in aggregate demand growth--the anticipated outcome of a supply shock--is expected to constrain the pass through of higher operating costs to consumers. That is, a deceleration in aggregate demand will constrain the ability of businesses to raise product prices, and result in a one-time squeeze on select business margins. The residual impact of the oil price shock on the CPI beyond a several month temporary impact may be elongated a bit by the tax cuts of the OBBBA, which by increasing after-tax disposable income, may mitigate the impact of the negative oil shock on aggregate demand.

The caveat and uncertainty, of course, is the future pattern of oil prices.

Mickey D. Levy

AuthorMore in Author Profile »Mickey Levy is a macroeconomist who uniquely analyzes economic and financial market performance and how they are affected by monetary and fiscal policies. Dr. Levy started his career conducting research at the Congressional Budget Office and American Enterprise Institute, and for many years was Chief Economist at Bank of America, followed by Berenberg Capital Markets. He is a Visiting Fellow at the Hoover Institution at Stanford University and a long-standing member of the Shadow Open Market Committee.

Dr. Levy is a leading expert on the Federal Reserve’s monetary policy, with a deep understanding of fiscal policy and how they interact. He has researched and spoken extensively on financial market behavior, and has a strong track record in forecasting. Dr. Levy’s early research was on the Fed’s debt monetization and different aspects of the government’s public finances. He has written hundreds of articles and papers for leading economic journals on U.S. and global economic conditions. He has testified frequently before the U.S. Congress on monetary and fiscal policies, banking and credit conditions, regulations, and global trade, and is a frequent contributor to the Wall Street Journal.

He is a member of the Council on Foreign Relations and the Economic Club of New York, and previously served on the Panel of Economic Advisors to the Federal Reserve of New York, as well as the Advisory Panel of the Office of Financial Research.

Dr. Levy holds a Ph.D. in Economics from University of Maryland, a Master’s in Public Policy from U.C. Berkeley, and a B.A. in Economics from U.C. Santa Barbara.