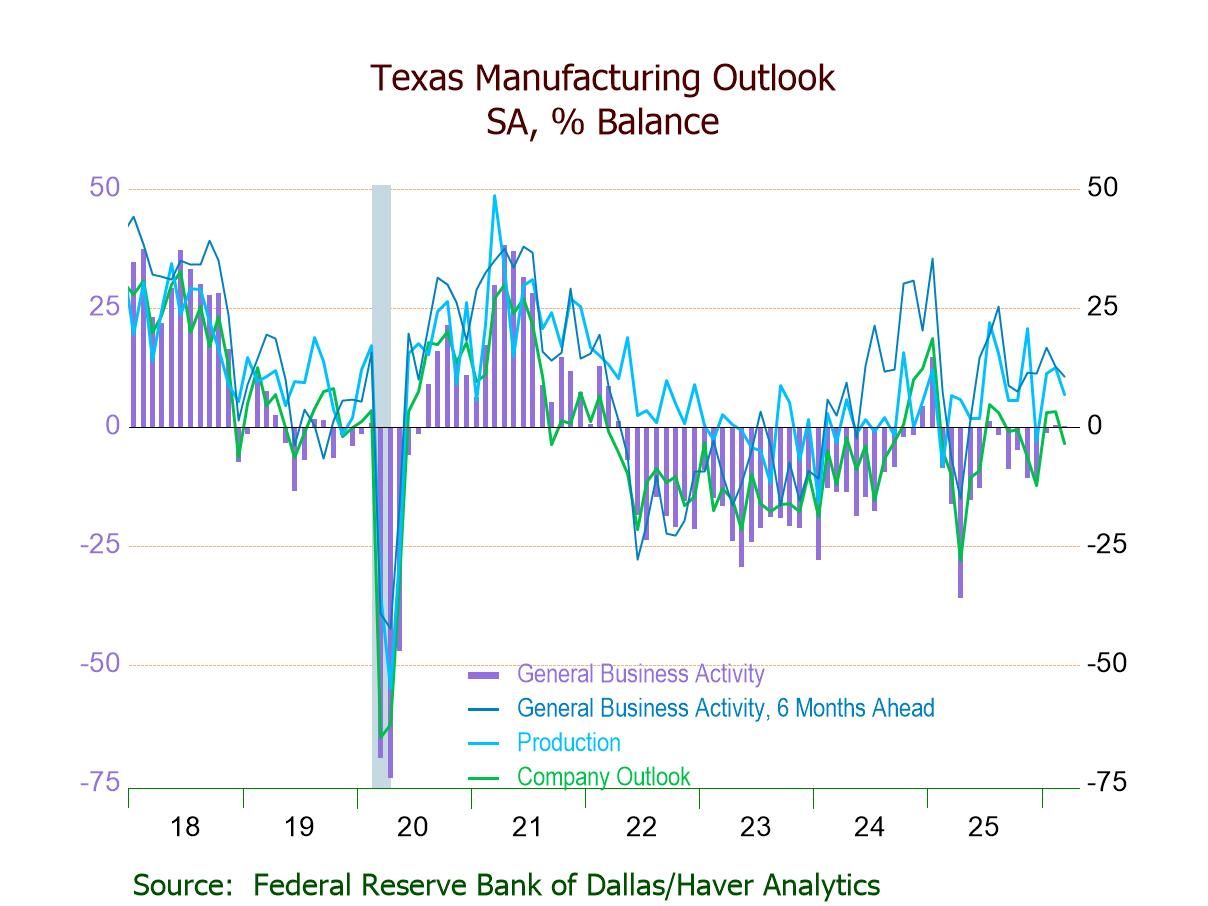

Texas General Business Activity Slightly Negative in March Amid Uncertainty; Expectations Still Positive

Summary

- General Business Activity -0.2 in Mar. vs. +0.2 in Feb.; negative for the 12th time in 14 mths.

- Company Outlook (-3.5) and Production (6.8) at three-month lows.

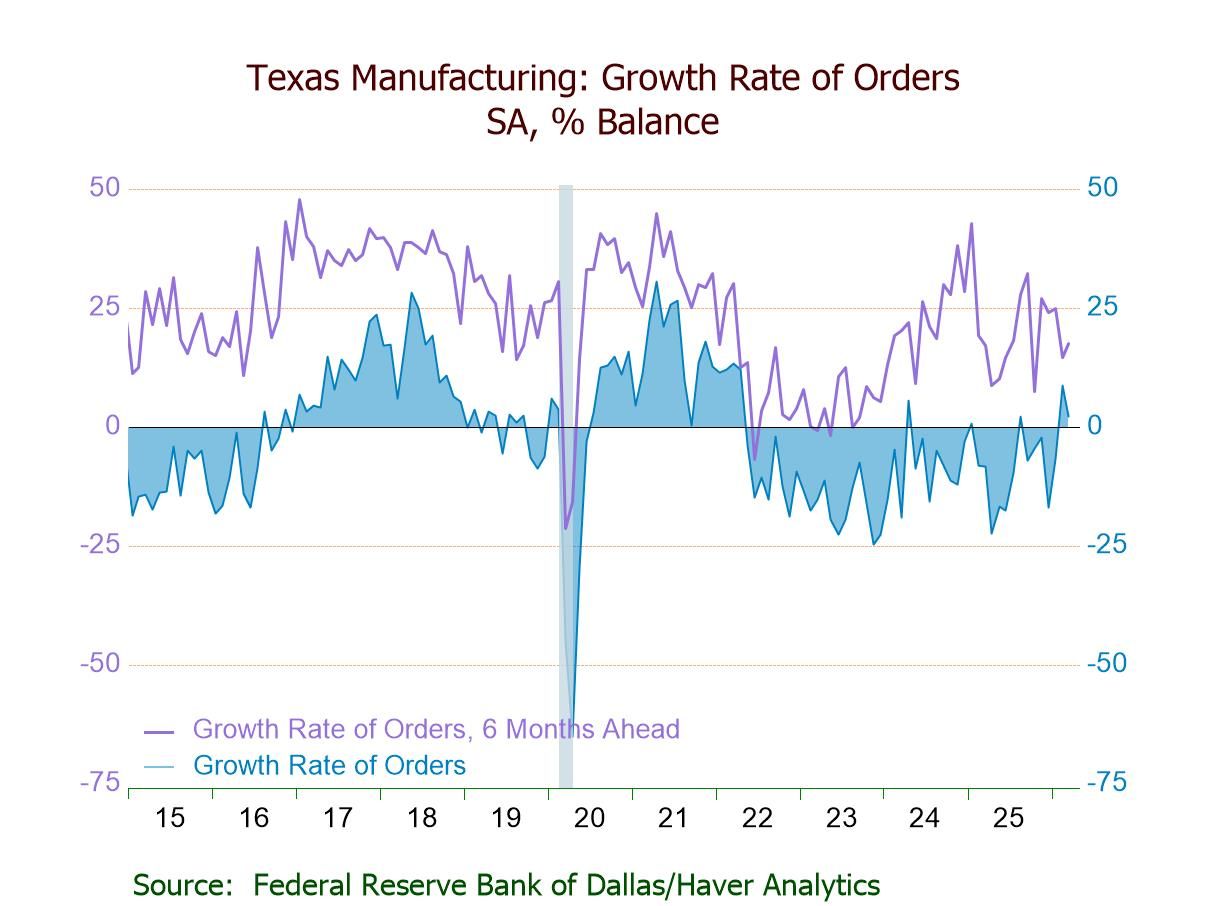

- New Orders Growth (2.2) positive for a second mth.; New Orders (6.1) lowest since Dec.

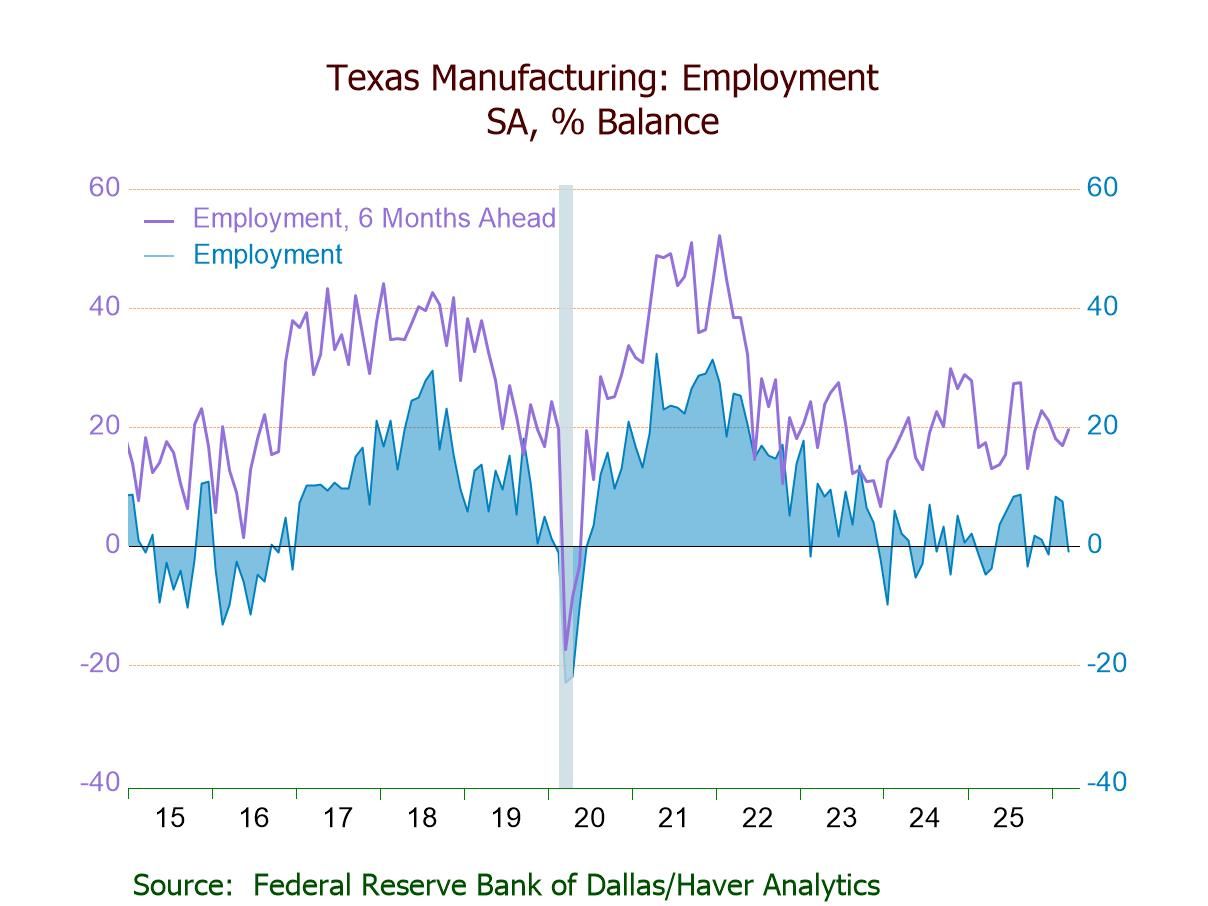

- Employment (-1.0) negative for the first time in three mths.

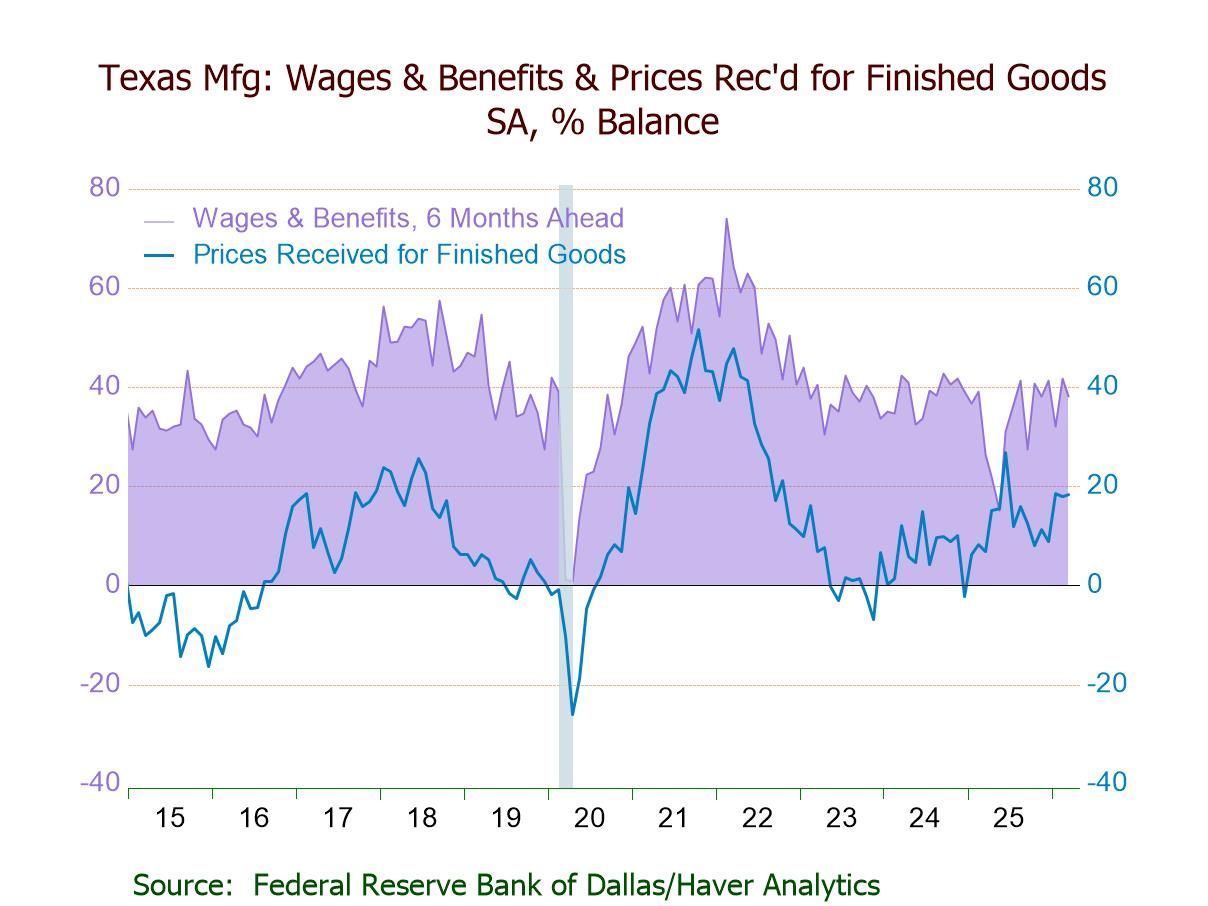

- Prices Received up 0.5 pt. to 18.4; Prices Paid up 1.0 pt. to 32.7.

- Future General Business Activity down 2.1 pts. to 10.6, still positive for the 11th straight mth.

General business activity in Texas eased in March after expanding in February, according to the Texas Manufacturing Outlook Survey conducted by the Federal Reserve Bank of Dallas. The overall measure—the general business activity index—was at -0.2 this month, compared with +0.2 in February, -1.2 in January, and -16.2 in March 2025. The March reading, while above a low of -35.9 in April 2025, was well below a high of +14.6 in January 2025. The index had been in negative territory since February 2025, with the exception of two positive readings in July 2025 (+1.2) and February (+0.2). In March, 21.0% of respondents reported improved business activity, down from 24.5% in February, while 21.2% of respondents reported worsened business conditions, down from February's 24.3%. The company outlook index fell to -3.5 in March, the lowest reading since December, after increasing to 3.1 in February. A lessened 14.0% of respondents expected improved company outlook this month while 17.5% expected deterioration. Data were collected between March 17 and 25 from 79 Texas manufacturers.

The production index, a key measure of state manufacturing conditions, dropped to 6.8 in March after a 1.3-point increase to 12.5 in February, indicating production expanded for the 12th time in 13 months but at the slowest pace in three months and at a below-average rate. Twenty-two percent of respondents reported higher production this month while 15.2% reported a decline. The capacity utilization index fell to 7.2 in March following a 4.7-point rise to 11.8 in February; it remained above a low of -15.5 in January 2024 but well below a record-high 46.6 in March 2021.

The growth rate of orders index declined to 2.2 in March after a 15.3-point jump to 8.6 in February, marking the second consecutive positive reading following five straight negatives. The index was above lows of -22.4 in April 2025 and -24.7 in November 2023 but significantly below a peak of 30.6 in April 2021. The new orders index fell to 6.1 this month from 11.1 in February, indicating an increase in demand for the fourth time in five months but at the lowest level since December. The index was above lows of -20.4 in April 2025 and -21.8 in November 2022 but well below a high of 22.6 in February 2022 and a record-high 39.9 in April 2021. The shipments index slid to 1.8 this month, the lowest of three successive positive readings, after easing to 9.9 in February. The unfilled orders index fell back into negative territory at -6.1 in March, the 18th negative reading in 19 months, after rising to 2.9 February. The index was below a high of 1.1 in August 2024 but above a low of -26.2 in July 2024. Meanwhile, the delivery time index declined to 2.8 this month after rising to 11.6 in February.

Labor market indexes showed employment growth stalled and workweeks were flat in March. The employment index fell to -1.0 this month from 7.5 in February, marking its first negative reading since December, with the near-zero level indicating little change in employment. The latest reading, while up from a low of -9.9 in January 2024, was far below a high of 17.7 in January 2023 and a record-high 32.3 in April 2021. A reduced 15.0% of respondents reported net hiring in March while a higher 16.0% reported net layoffs. The hours worked index declined to 0.9 this month, the fourth positive reading in five months, after rising to 6.1 in February. Meanwhile, the wages & benefits index decreased to 25.2 in March following a 14.5-point rebound to 31.9 in February, having been trending downward since a peak of 55.1 in March 2022.

Inflationary pressures were little changed this month. The index for prices received for finished goods rose to 18.4 in March following a 0.6-point decline to 17.9 in February; it was up from a low of -6.8 in November 2023 but meaningfully below a high of 47.8 in March 2022 and a peak of 51.6 in October 2021. In March, an increased 24.5% of respondents reported raising prices while only 6.1% reported lowering prices. The index of prices paid for raw materials edged up to 32.7 this month after a 5.4-point drop to 31.7 in February. The index was well above a low of 0.9 in June 2023 but significantly below 72.8 in March 2022 and a record-high 84.4 in November 2021.

Expectations on future manufacturing activity remained positive this month. The future general business activity index fell to 10.6 in March after a 3.9-point decline to 12.7 in February, signaling expansion for the 11th straight month but at the slowest pace since October. The future production index rose to 35.7, the highest level since August, from February’s 34.3. Other indexes of future manufacturing activity also rose in March (vs. February), signaling increased activity six months ahead: new orders (29.2 vs. 25.0), growth rate of new orders (17.5 vs. 14.5), employment (19.5 vs. 16.8), and capital expenditures (24.8 vs. 10.7). Meanwhile, future indexes for company outlook (18.2 vs. 25.7), capacity utilization (27.0 vs. 27.3), shipments (28.8 vs. 31.6), and wages & benefits (38.0 vs. 41.7) declined in March (vs. February), but they remained in positive territory.

Each index is calculated by subtracting the percentage reporting a decrease in activity from the percentage reporting an increase. When all firms report rising activity, an index will register 100. An index will register -100 when all firms report a decrease. An index will be zero when the number of firms reporting an increase equals the number reporting a decrease. Data for the Texas Manufacturing Outlook, conducted by the Federal Reserve Bank of Dallas, can be found in Haver's SURVEYS database.

Winnie Tapasanun

AuthorMore in Author Profile »Winnie Tapasanun has been working for Haver Analytics since 2013. She has 20+ years of working in the financial services industry. As Vice President and Economic Analyst at Globicus International, Inc., a New York-based company specializing in macroeconomics and financial markets, Winnie oversaw the company’s business operations, managed financial and economic data, and wrote daily reports on macroeconomics and financial markets. Prior to working at Globicus, she was Investment Promotion Officer at the New York Office of the Thailand Board of Investment (BOI) where she wrote monthly reports on the U.S. economic outlook, wrote reports on the outlook of key U.S. industries, and assisted investors on doing business and investment in Thailand. Prior to joining the BOI, she was Adjunct Professor teaching International Political Economy/International Relations at the City College of New York. Prior to her teaching experience at the CCNY, Winnie successfully completed internships at the United Nations. Winnie holds an MA Degree from Long Island University, New York. She also did graduate studies at Columbia University in the City of New York and doctoral requirements at the Graduate Center of the City University of New York. Her areas of specialization are international political economy, macroeconomics, financial markets, political economy, international relations, and business development/business strategy. Her regional specialization includes, but not limited to, Southeast Asia and East Asia. Winnie is bilingual in English and Thai with competency in French. She loves to travel (~30 countries) to better understand each country’s unique economy, fascinating culture and people as well as the global economy as a whole.

More Economy in Brief