Sweden’s Trade; Exports Surge as Imports Recede

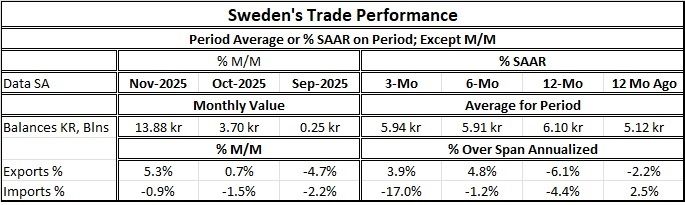

Swedish exports advanced month-to-month for the second month in a row while imports continued on a losing streak declining by 0.9% in November.

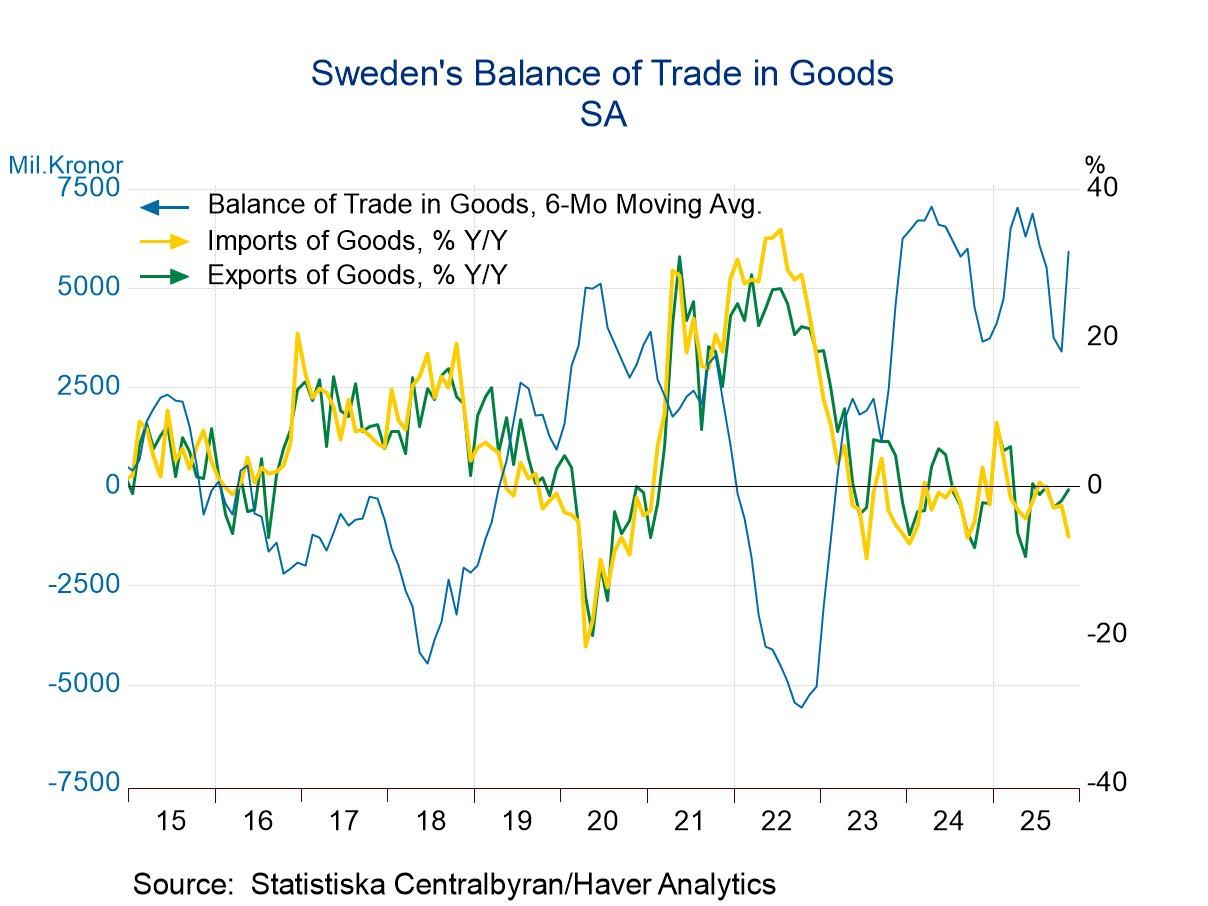

Exports have gradually been firming with exports falling by 6.1% over 12 months, rising at an annual rate of 4.8% over six months, and then rising at a 3.9% annual rate over three months. Exports are not on a steady acceleration path, but they have transitioned from a year-over-year growth rate that's negative to moderate positive short-term rates of growth.

Swedish imports, on the other hand, are weakening relatively sharply. Imports were down 4.4% over 12 months, down at a 1.2% annual rate over six months, and falling at a 17% annual rate over three months.

The global trade picture remains somewhat mixed. The Baltic Dry goods index, which is an indicator of global trade volume, has backed off of its highs but continues to post relatively steady volume indications. However, the S&P global manufacturing survey has been showing weakness; when manufacturing is weak, typically international trade is weak as well. Swedish trade may be picking up some of that weakness as well.

On balance, Sweden's trade surplus has continued to recover and hold to a relatively high level over recent months as exports have maintained momentum better than imports.

Swedish domestic barometers of economic growth have remained relatively upbeat including orders and industrial production as well as employment growth and GDP. There is no reason there to expect weak imports based on the recent data we have seen. But then sometimes trade data show economic weakness first.

At this time, the yearend weakness in Sweden’s imports is without a specific cause. Year-end flows can be surprising. Domestic demand, however, does not appear to be weak. But there is a good deal of weakness in Europe and the Ukraine-Russia war is still a nagging factor – a cloud that hangs over all of Europe with no certain end date or result in sight.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global