Spanish Inflation Flares at Year-End

When inflation numbers come hot off the griddle, some part of them might stick to the pan. That's the case this month with Spain’s release of inflation in December. It provides us with the headline for the HICP measure, a headline to the domestic measure, and the domestic measure excluding energy. But it does not release the sector detail for the rest of the report.

However, based upon what's been released, it’s clear that inflation in Spain has picked up. The part of the core that we have in-hand, which is just the portion excluding energy, still appears to be fairly well behaved; however, its gain is still slightly excessive.

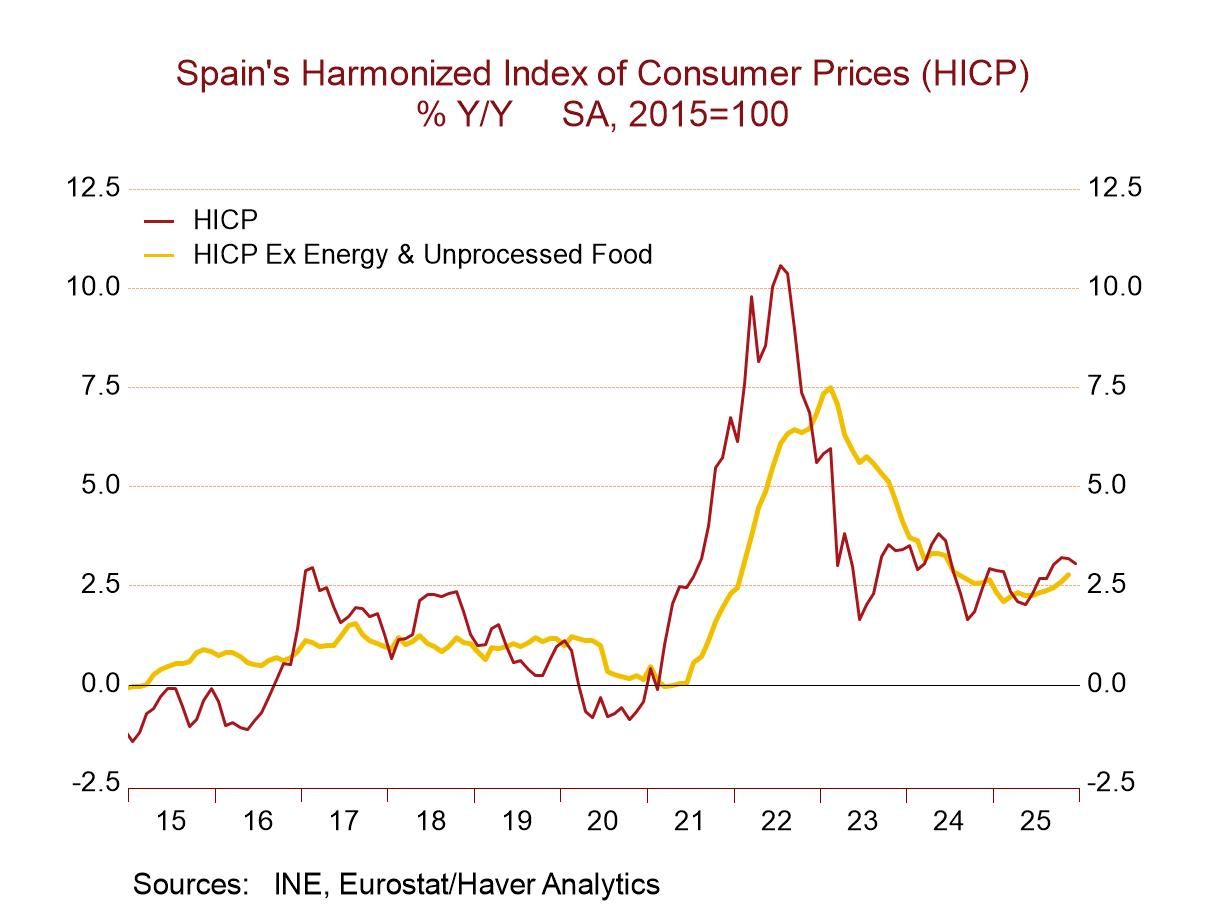

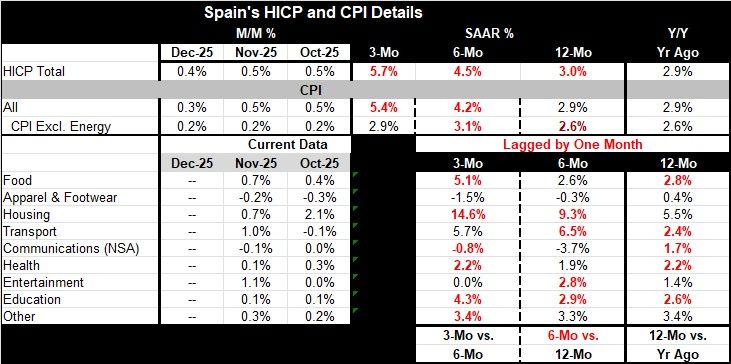

HICP trend Spain’s HICP measure in December rose 0.4% after rising by 0.5% in both October and November; those are hot numbers. That translates into a 5.7% annual rate over three months which is hotter than its pace of 4.5% over six months which in turn is hotter than the 12-month increase of 3%. The HCP headline for Spain has clearly been accelerating, the year-over-year rise is too-hot, and the shorter-term metrics are hotter still. This is not good news, and this is not a welcome progression.

Domestic inflation Looking at Spain’s domestic CPI conditions, we find that they are still on the hot side with December showing a headline gain of 0.3% but gains in October and November of 0.5% each, producing a three-month annual rate of 5.4%, which is hotter than its 4.2% over six months, which, in turn, is hotter than the year-over-year gain at 2.9%. And these patterns/results are very similar to the pattern and the readings for the HICP. The domestic inflation picture is too hot over 12 months and accelerating over the shorter periods.

Domestic inflation ex-energy: The CPI excluding energy is not as bloated as the HICP or the domestic headline, but it is still a reading on rough terrain. Over 12 months, inflation excluding energy rises at a 2.6% annual rate; that's above the 2% pace sought by the ECB for the community as a whole. Over six months, the reading ramps up to a 3.1% annual rate, again moving the wrong direction and a reading at 3.1% is simply too hot. Over three months, there's a slight deceleration compared to six months but still a rate that is too hot, at 2.9%, and stronger than the 12-month pace. Core inflation is better behaved than headline inflation and both the domestic and the HICP frameworks, but inflation is unruly overall and, for the most part, showing either acceleration or at least a 3-month pace stronger than its 12-month pace. None of this is what the ECB is looking for or trying to achieve.

Beyond the missing details The details of the Spanish report are missing for December because the data are too preliminary for the authorities to post. However, if we look at the sequential pace of inflation over 12 months, six months, and three months on a lagged basis, it is looking at data that are up-to-date through November rather than through December what's the numbers that are generally excessive and they show too much acceleration moving from 12-months to 6-months to 3-months. Over 12 months compared to a year ago, five of nine categories show inflation accelerating. Over 6 months compared to 12 months, four categories are accelerating. Over 3 months compared to 6 months, six of the nine categories are accelerating. These acceleration tendencies are worrisome.

In addition, over 12 months, six of nine categories have a pace above 2%. Over 6 months, six of nine categories have annualized gains above 2%, and over 3 months, the lagged data show six of nine categories with gains above 2%. Only apparel shows inflation tempered on all horizons (at or below 2%). Food, housing, transport, education and other all show above 2% inflation on all horizons.

Summing up-challenging times ahead? Is Spain past its best inflation performance? Is the inflation worm going to begin to turn more broadly? These are trends we will need to watch. Inflation broadly has slowed or stopped its declines and largely done that in Europe as well as in the United States. Inflation is now hovering at a pace that is too strong- maybe tolerable or maybe not. Central banks need to decide and tell us what a 2% target means. Then, the question of what’s next hangs in the air. U.K. inflation remains excessive but has stepped down as the economy has begun to experience some significantly weaker economic data. Is that the future? Is it stagflation? Is it recovering from a slowdown and higher rates of interest and inflation? Or will there be continued inflation progress? Open the door on 2026…the envelope… please.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global