Global| Feb 20 2026

Global| Feb 20 2026S&P PMIs Are Mostly Stronger in February

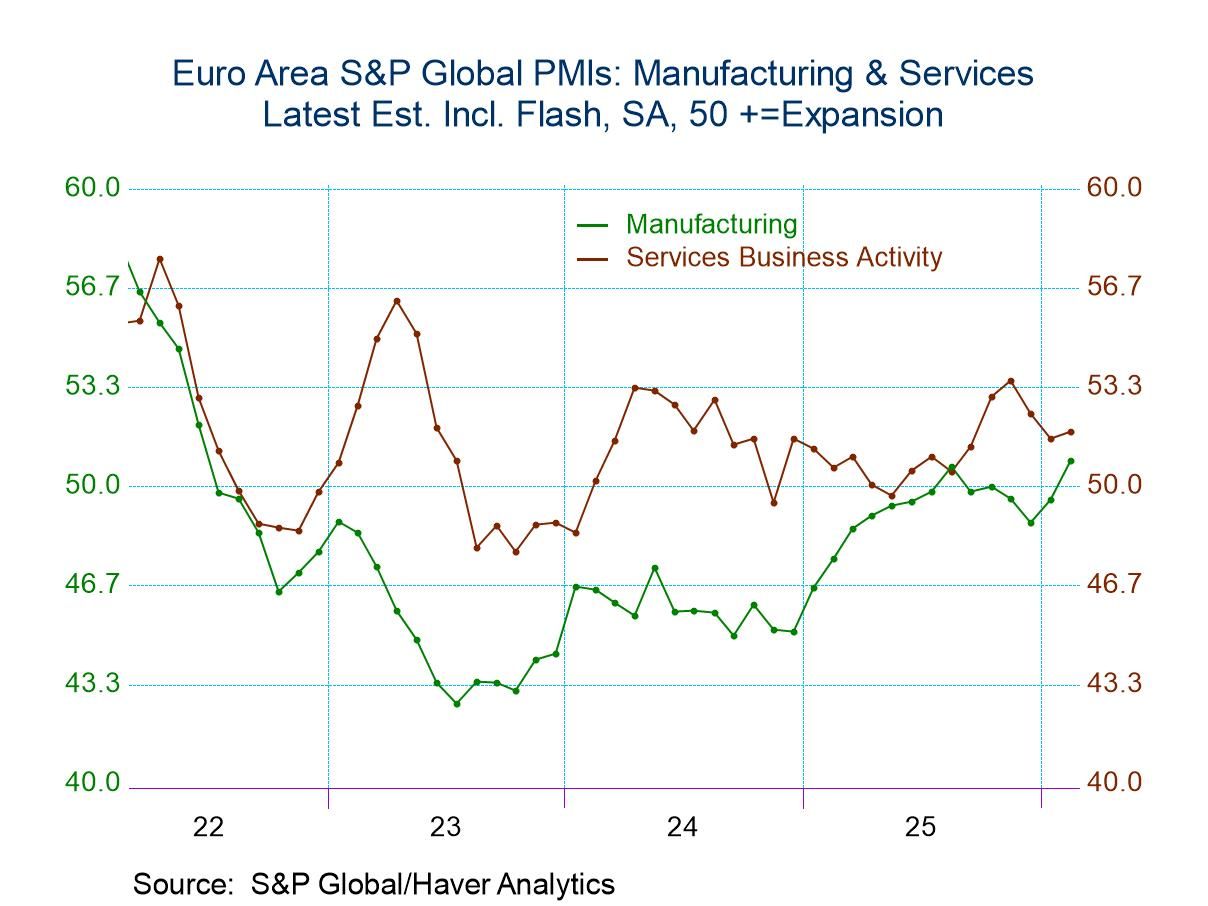

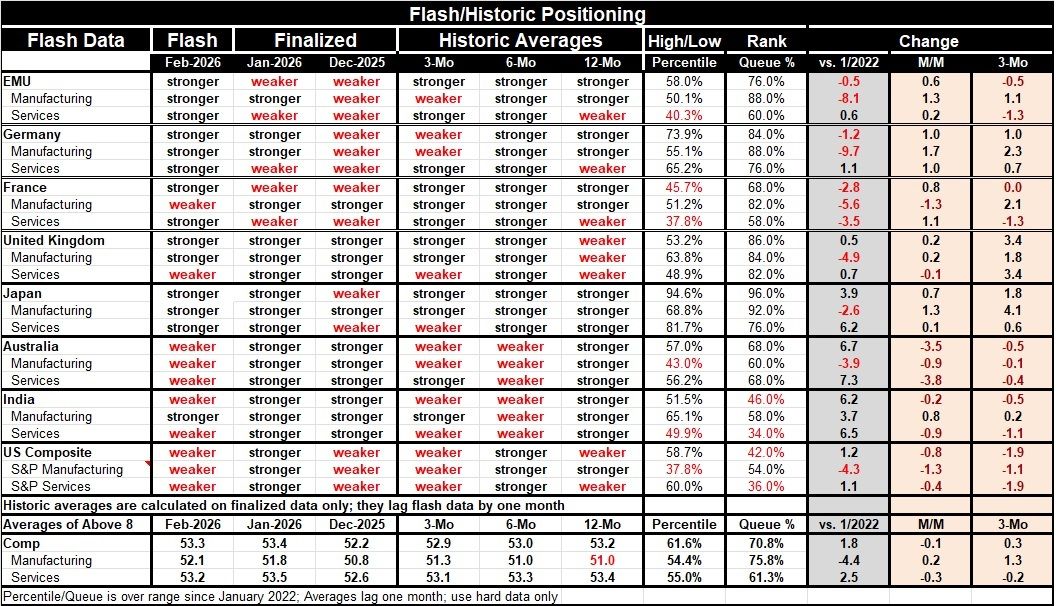

PMI data for February, issued by S&P on a flash basis, show relatively broad improvement PMI performance in February, with the exception of Australia, India, and the United States. The European Monetary Union shows improvement in its composite index as well as for manufacturing and services. This pushed to higher ratings, supported by Germany and France with the exception that French manufacturing took a step back in February. In the United Kingdom, the composite and manufacturing indexes moved ahead but services weakened. In Japan, the composite, manufacturing and services all improved on a month-to-month basis. However, Australia saw a step back in all three sectors after several months of continued strengthening. India also saw a step back in the composite and services after a recent string of improvements being reported. The United States shows uneven conditions, with a weakening across the board month-to-month in February vs. an across-the-board rebound in January, and then across-the-board weakening in December. This leaves the U.S. in a weakening and volatile situation

An unweighted average of the monthly composite, manufacturing, and services indexes shows a one-tick step back for the composite, a small step up for manufacturing, and a small step back in services for February compared to January. January had made across the board improvements relative to December.

Sequential comparisons where data are lagged by one month and the calculations are made only off of hard data (not off of flash or preliminary data) show mixed economic conditions and unclear trends. EMU shows sequential strengthening in the composite as do France and Japan; Japan also shows persistent strengthening in manufacturing, as the yen has been dropping. And while there is a lot of weakening sequentially, there is no persistent weakening reported for 12-months to 6-months to 3-months.

Over three months, there's a split in what is reported with 12 of the 24 sectors weakening compared to six months ago and 12 of them strengthening. Over six months, only six of the sectors are weakening; the remainder strengthening over 12 months; eight of the sectors are weakening over 12 months compared to a year ago, with the remainder strengthening. While it's not a clear path to deterioration, there is a clear tendency to deterioration over three months compared to six months. However, an unweighted comparison of the three sectors shows that composite manufacturing and services still demonstrate a bit of muddy water with the composites weakening over three months only by a tick to 52.9 compared to 53 while manufacturing improves slightly and services weakens slightly compared to six months. Over six months, there's only a slight step back from the statistics reported over 12 months.

Not a lot of shifting, but some good news and bad news The bottom line is there's not a whole lot of change going on according to the PMI data. On a breadth basis, there has been some improvement, but the magnitudes involved seem to wash out some of that improvement, neutralizing when expressing as average comparisons. However, one place where there does appear to be evidence of more solid performance is in the queue percentile standings. Among these 8 reporters involving 24 sectors, only four sectors report current standings below their median on data back to January 2022. One of those countries is India, with a weaker composite and services sector; the other is the United States, with a weaker composite and services sector. The U.S. composite has a queue percentile standing at its 42nd percentile, below its neutral position of 50%. The U.S. services sector is even weaker with a 36-percentile standing, close to the lower third of all the U.S. PMI values that have shown for services since 2022 on a monthly basis.

U.S. economy has been cranking out some reasonably strong economic numbers across the board including consumer spending and GDP figures, allowing for a disappointing fourth quarter that is being attributed to the government shutdown. However, what's been lacking on the U.S. side has been strong job market performance and, of course, because of mortgage rates being high, there has been a weak construction sector in the U.S. economy. Still, the queue standing across the board for other countries should be reassuring. The average composite ranking for this group of countries is in the 70th percentile, with manufacturing in the 75th percentile and services in their 61st percentile. These are relatively firm readings and should be reassuring. At the same time, central banks have made progress on inflation and tightening cycles have not been engaged or easing cycles are being extended for all central banks except for the Bank of Japan, which has been experiencing growth and inflation in different measures from the rest of the G7 countries. On balance, however, global growth appears to be moving forward and now we'll have to see what happens with the U.S. Supreme Court having overthrown the imposition of tariffs that the Trump administration put in place without Congressional backing. We could see some considerable shifting in the months ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief