Q4 GDP: Constrained by Federal Spending

Summary

- Non-federal activity was lighter than expected, but still respectable.

- PCE inflation remains stubborn.

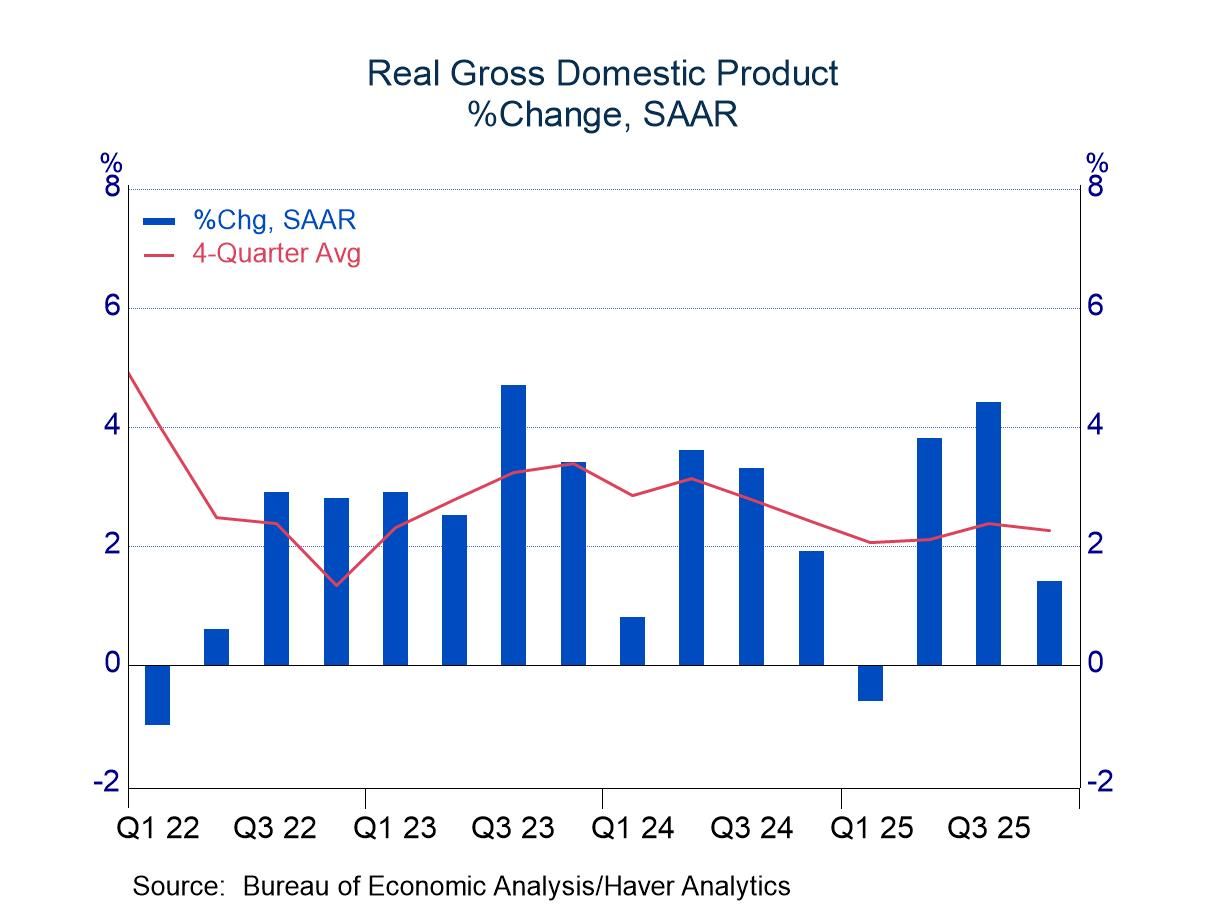

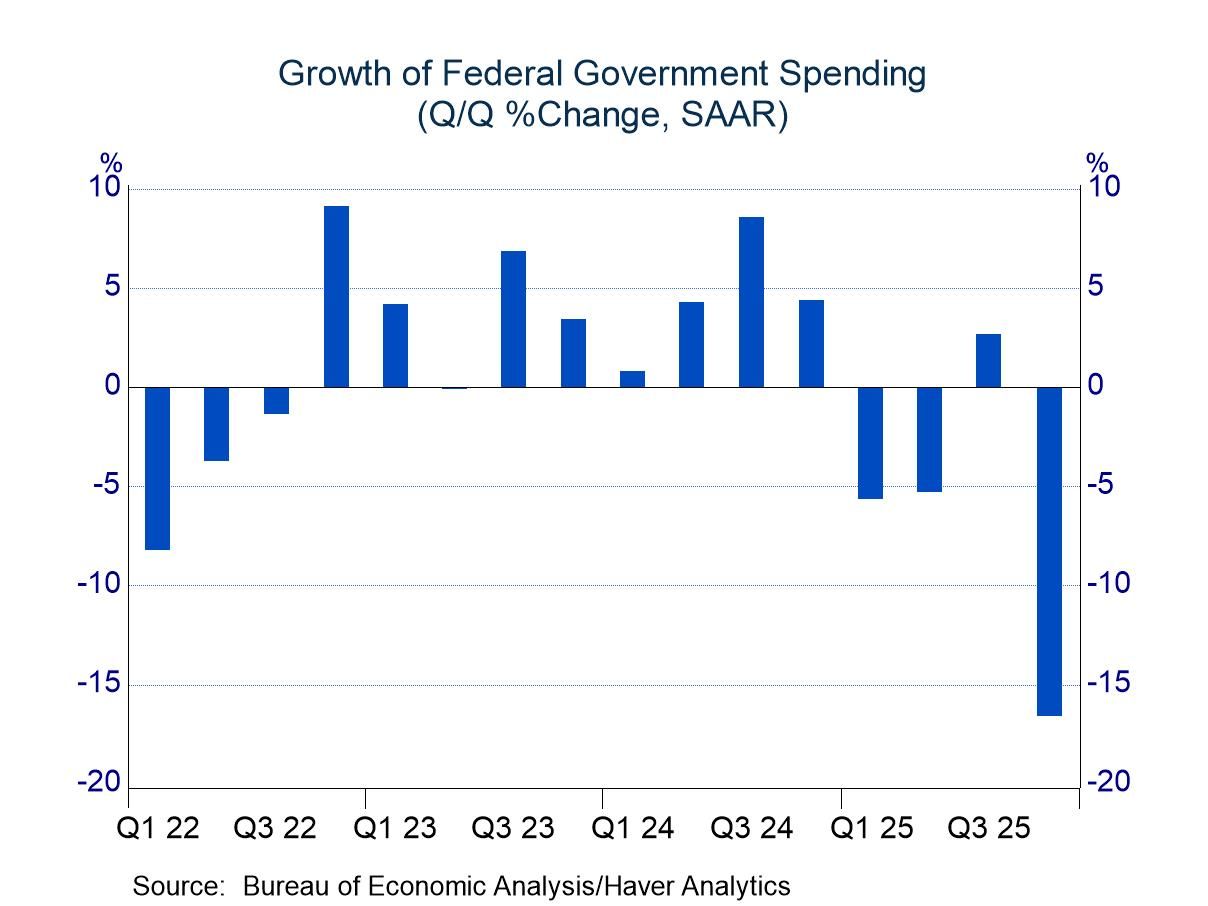

Real Gross Domestic Product rose 1.4% in the fourth quarter of 2025, slower than the recent average but no doubt influenced by the government shutdown. Federal spending often moves erratically, but the tumble of 16.6% in the final months of last year was unusually large. Indeed, one has to go back to 1972 to find a sharper decline (and to the 1950s before that), and these results were only slightly weaker than the Q4 decline.

Even allowing for the government shutdown, the latest results were a bit shy of expectations. Without the drop in federal outlays, which subtracted 1.2 percentage points from GDP growth, the economy would have expanded 2.6% in Q4, still shy of most surveys that showed consensus forecasts in the neighborhood of 3.0%. A downside surprise of sorts occurred in net exports. Monthly figures through November had suggested that international trade would provide strong support, but this sector added only 0.1 percentage point to GDP growth.

Other areas posted nondescript results. Consumer spending and business fixed investment were less vigorous than the best results of the past two years, but the latest growth rates were comfortably within recent ranges. Housing activity remained soft, making the sixth negative contribution to GDP growth in the past seven quarters. However, the constraints from housing over this span have generally been small.

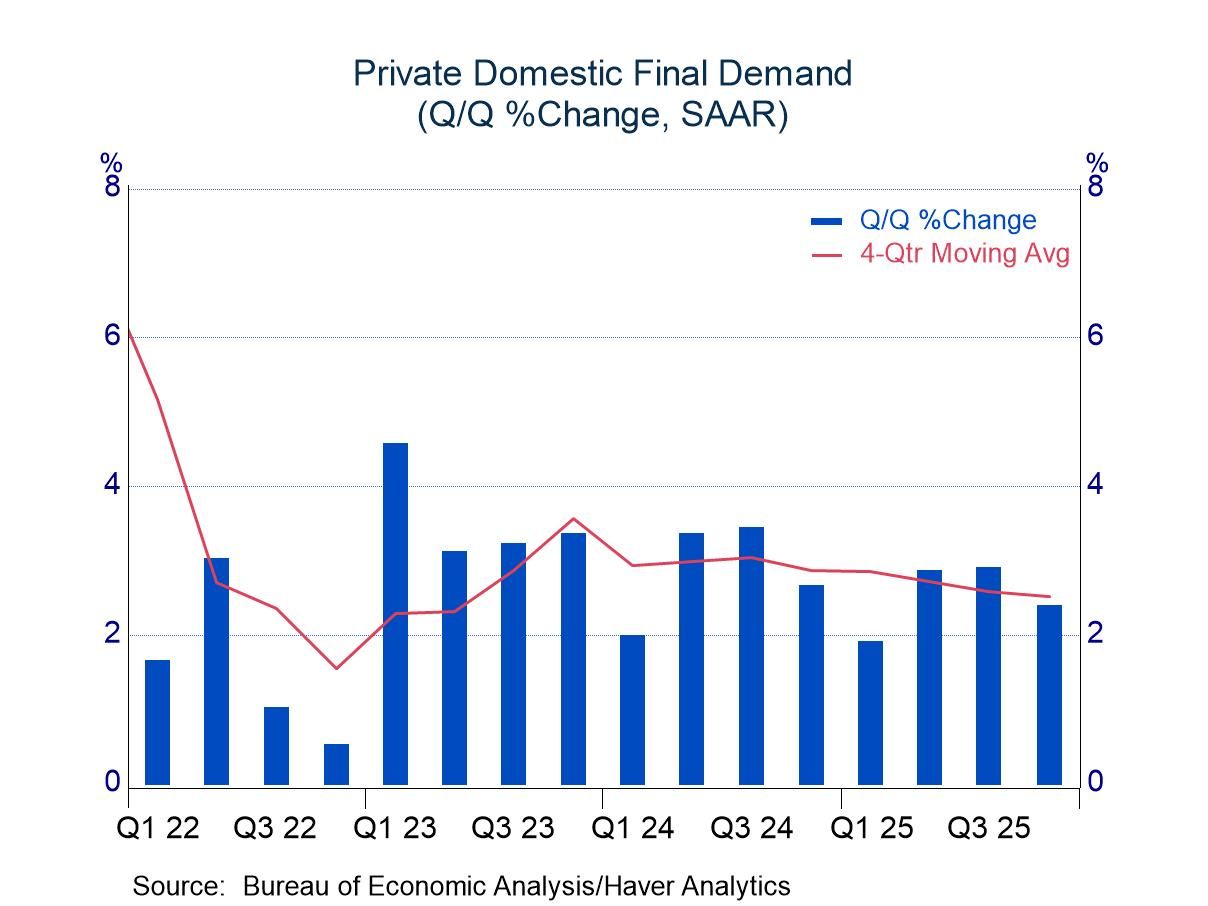

The fourth quarter, and most of last year, were oddities because of the government shutdown in Q4 and the imposition of tariffs in April followed by marked adjustments in subsequent months. Such changes can lead to pronounced swings in economic activity and leave a muddled picture on underlying trends. In such environments, a different perspective on economic output can be helpful. Specifically, private domestic final demand (PDFD, GDP less government spending, net exports, and inventory investment) excludes areas that often move erratically, thus removing random shifts and reducing volatility.

PDFD was especially useful last year because tariffs generated pronounced shifts in net exports and inventory investment, and the government shutdown distorted activity in the fourth quarter. As shown in the chart below (left), quarterly variations in private domestic final demand were modest last year. The underlying trend decelerated, but the slowing was modest and growth in the fourth quarter was respectable at 2.4%.

The GDP price index rose at an annual rate of 3.6% in the fourth quarter of the year, one of the heftier advances of the past three years. A surge of 15.6 percent in the prices paid by the federal government had a strong influence on this result (shutdown related?), but readings of 3.9% for business equipment and 2.9% for consumer goods and services also were suggestive of an inflation impulse in the economy.

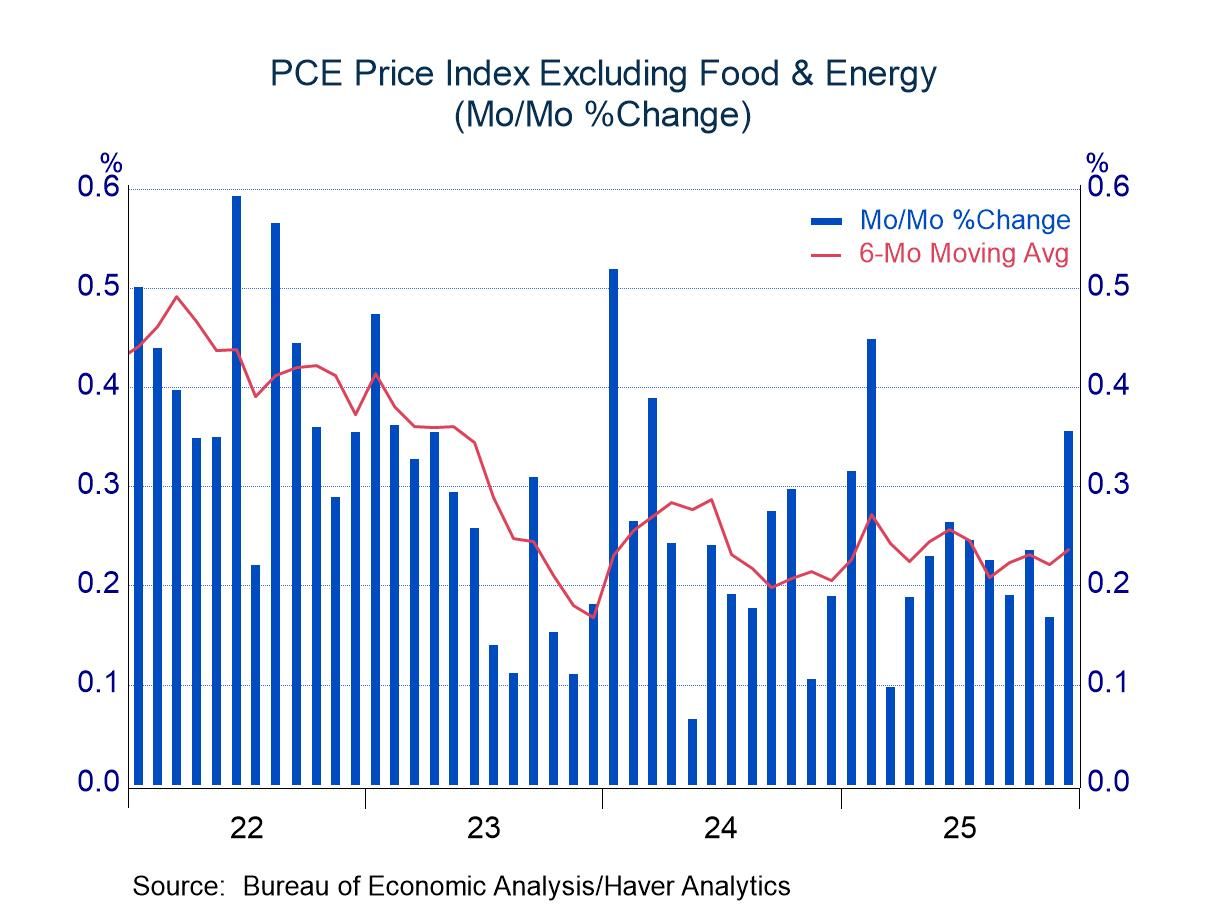

The increase in consumer prices was evident in the December report on personal income and consumption, which showed month-to-month increases of 0.4% for both headline and core price indexes for personal consumption expenditures. Year-over-year readings inched higher to 2.9% for all items and 3.0% for prices excluding food and energy. The latest results will no doubt leave Fed officials uncomfortable.

The GDP data can be found in Haver’s USECON and USNA databases. USNA contains virtually all of the Bureau of Economic Analysis detail in the national accounts. The Action Economics consensus estimates can be found in AS1REPNA.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Asia

Asia