May Employment Report: Revival in the Labor Market

Summary

- Nonfarm payrolls post their third consecutive firm advance.

- Unemployment showed marginal improvement.

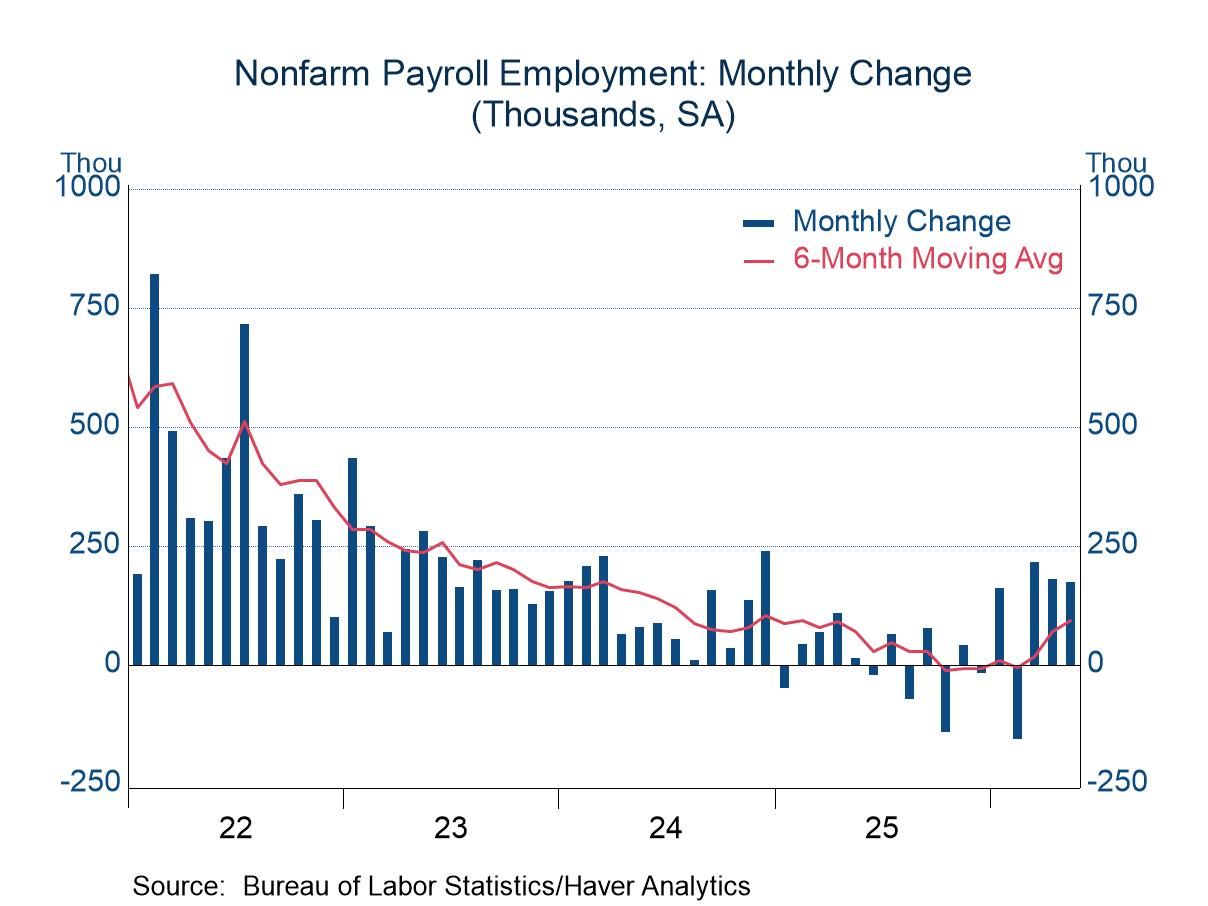

Nonfarm payrolls rose 172k in May, noticeably stronger than the expectation of 92k shown in the Action Economics survey. Moreover, results for the prior two months combined were revised higher by 93k. The gain in May does not appear to be an isolated event, as payrolls have now posted firm showings for three consecutive months (average advance of 188k). This performance represents a marked improvement from late 2025, when payrolls were showing essentially no net gain.

A good portion of the job growth in May occurred in the local government sector (55k), but the health care and leisure & hospitality sectors also were strong. The construction and manufacturing industries (highly cyclical areas) were both in the plus column. Soft spots were limited, with only the financial services sector showing notable job cuts (-22k).

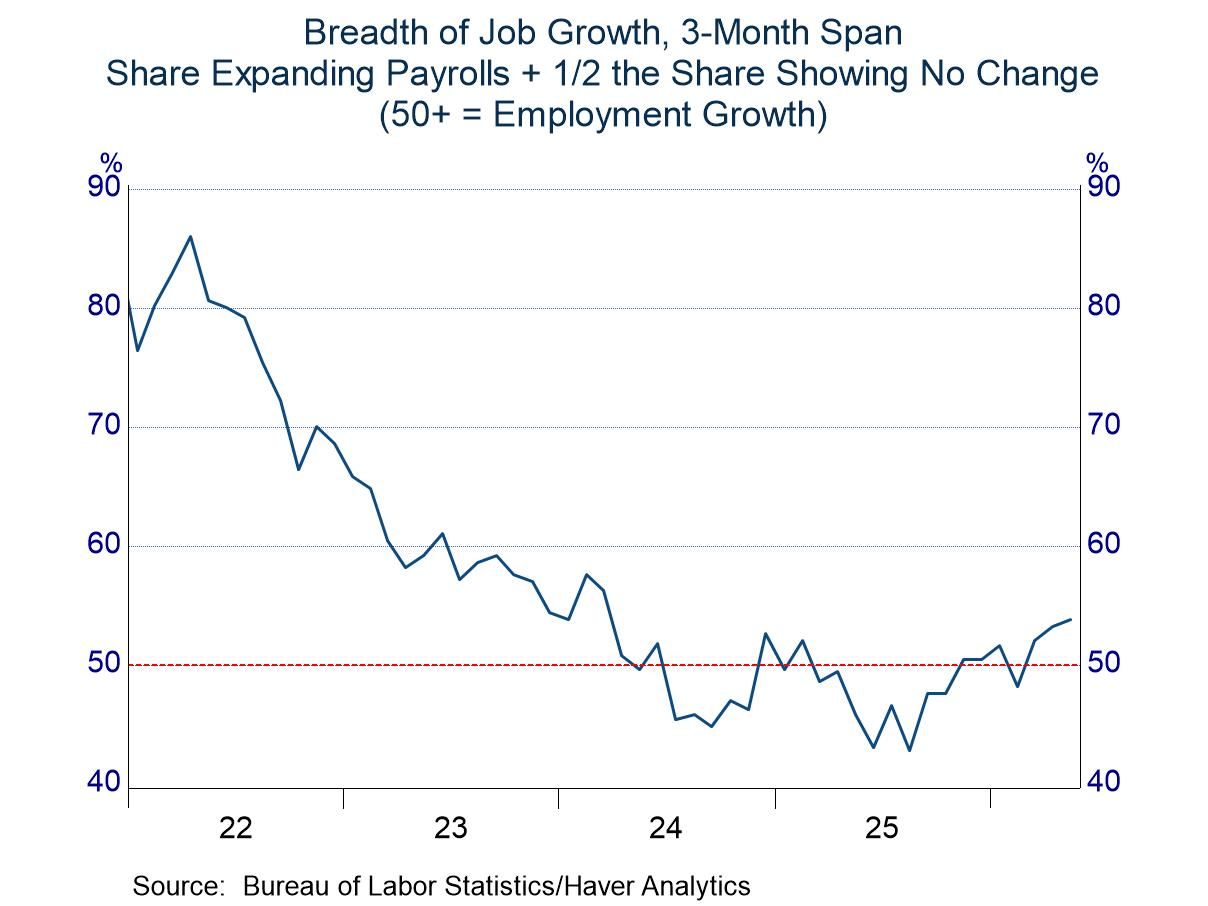

The improvement in the labor market also was evident in the payroll diffusion index. This measure shows the share of industries expanding payrolls plus one-half the share holding payrolls steady; a reading of 50 separates net expansion from contraction. This index was in sub-50 territory during much of 2024–25, but it moved into 50+ territory in March and climbed a bit higher in April and May (53.8 in May).

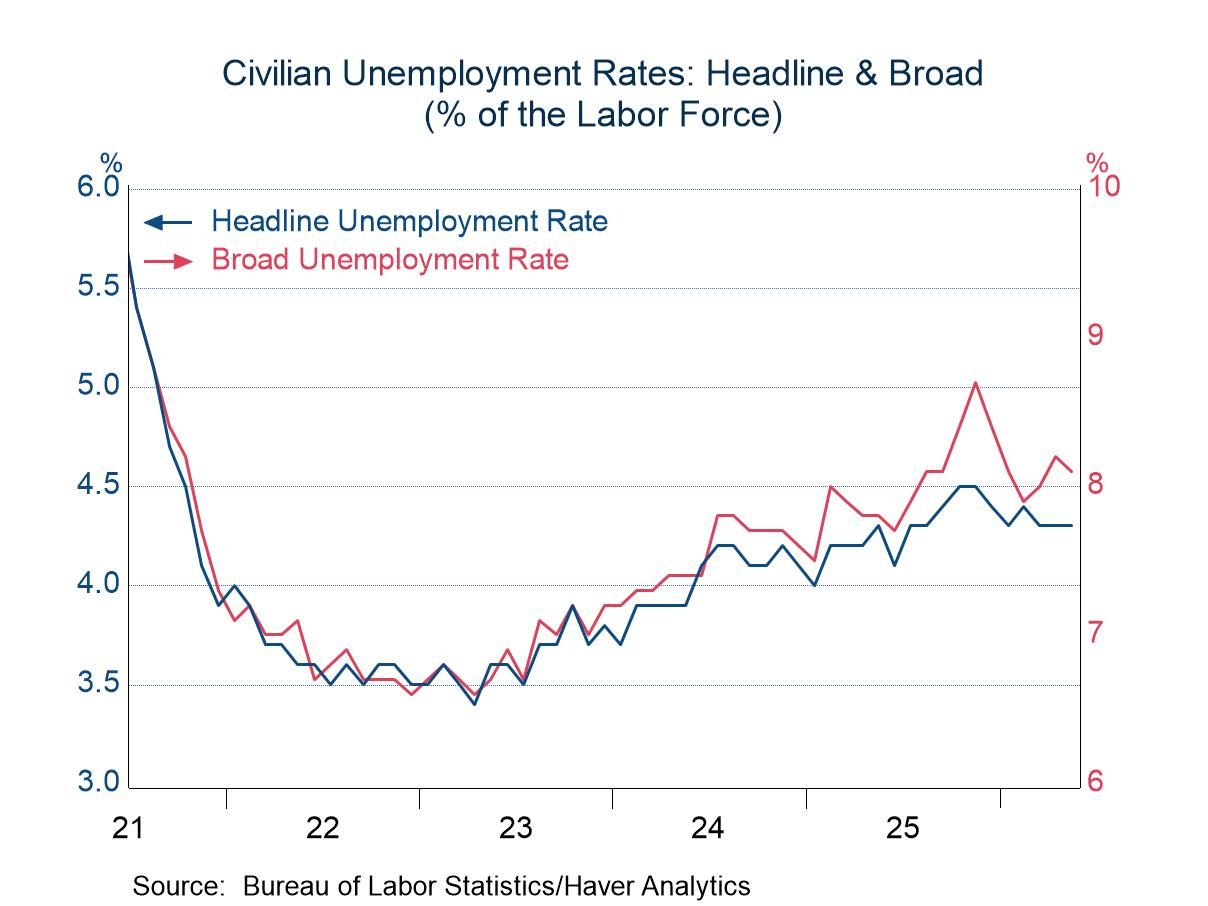

The unemployment rate was reported as steady at 4.3%, but a more precise calculation shows a slight improvement (4.296% versus 4.337% in April). Moreover, the dip was meaningful, as it was driven by employment growth as measured by the household survey (149k) that exceeded the increase in the size of the labor force (83k). The broad unemployment rate (the so-called U-6 measure) fell 0.1 percentage point to 8.1%. Both additional components of the broad unemployment rate contributed to the improvement (the number of individuals working part time involuntarily and the number of individuals who would like a job but are not actively searching).

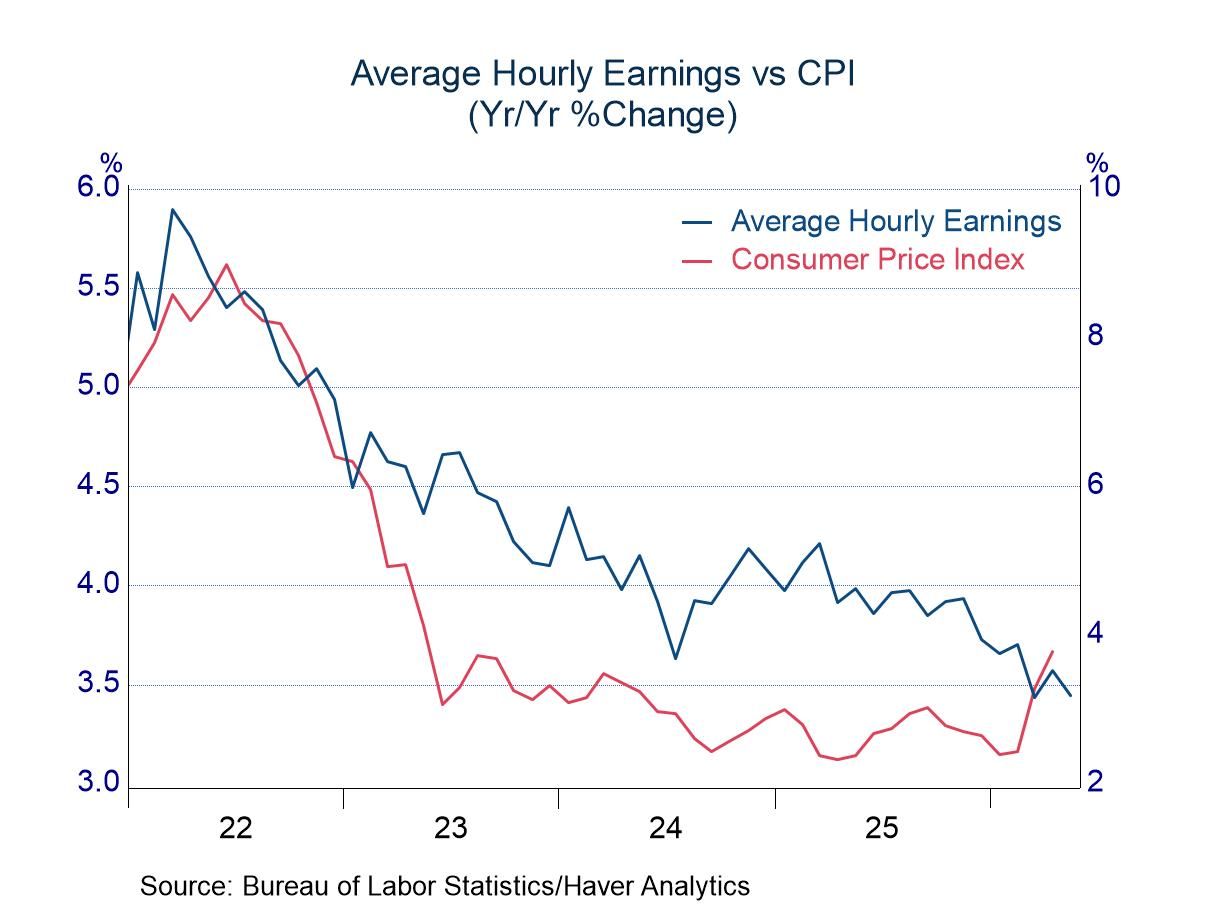

Average hourly earnings rose 0.3% in May, a touch firmer than readings of 0.2% in the prior two months. Although earnings posted a solid advance in May, the increase was lighter than the 0.4% gain in May of last year, and thus the year-over-year change eased to 3.4% from 3.6% in April. Year-over-year changes in average hourly earnings had been larger than those in the consumer price index, indicating that many workers were registering gains in purchasing power. However, with the pickup in inflation, individuals fell behind in April, and the CPI for May (to be published on June 10) could show additional slippage in purchasing power.

The employment and earnings data are collected from surveys taken each month during the week containing the 12th day of the month. The labor market data are contained in Haver's USECON database. Detailed figures are in the EMPL and LABOR databases. The expectations figures are in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global