Japan’s Tankan Ticks Higher for Large Manufacturers

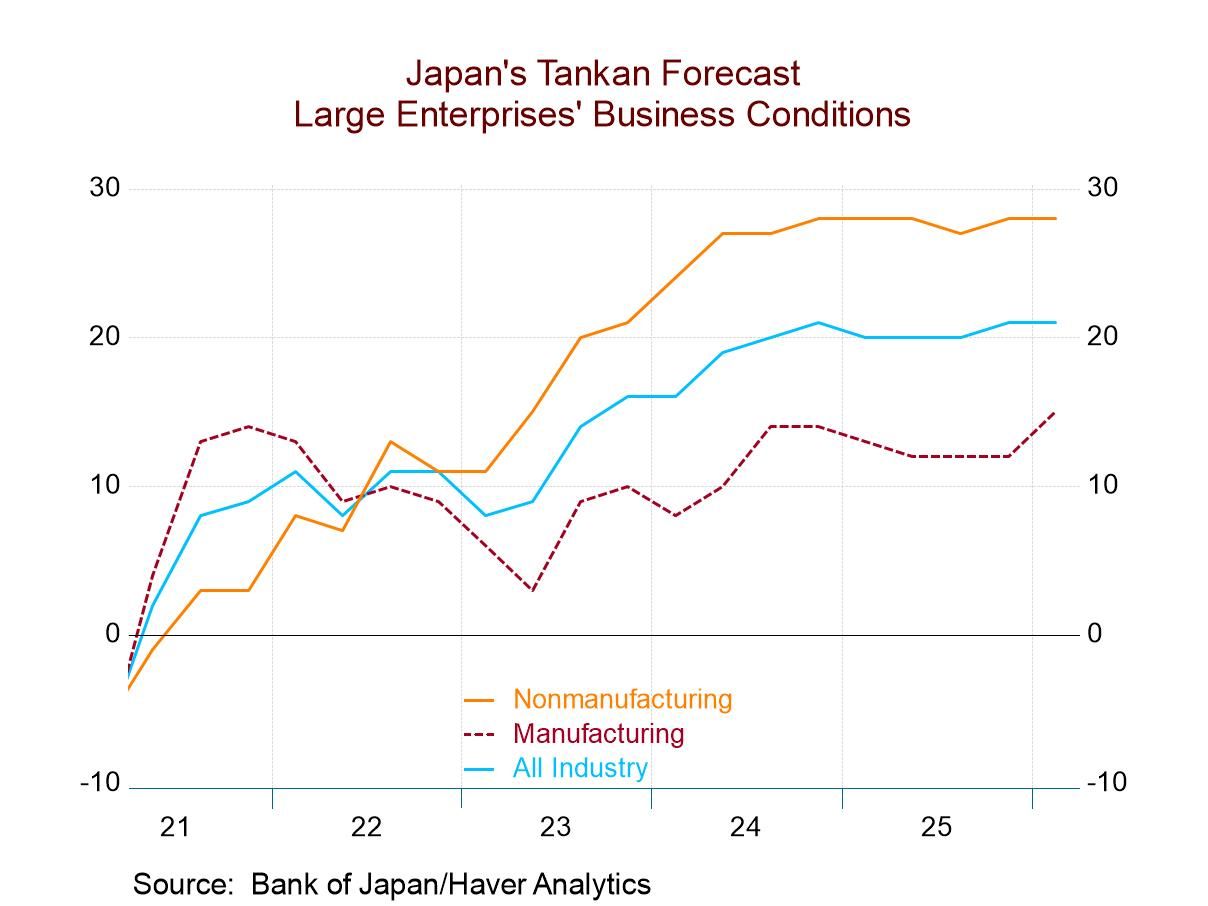

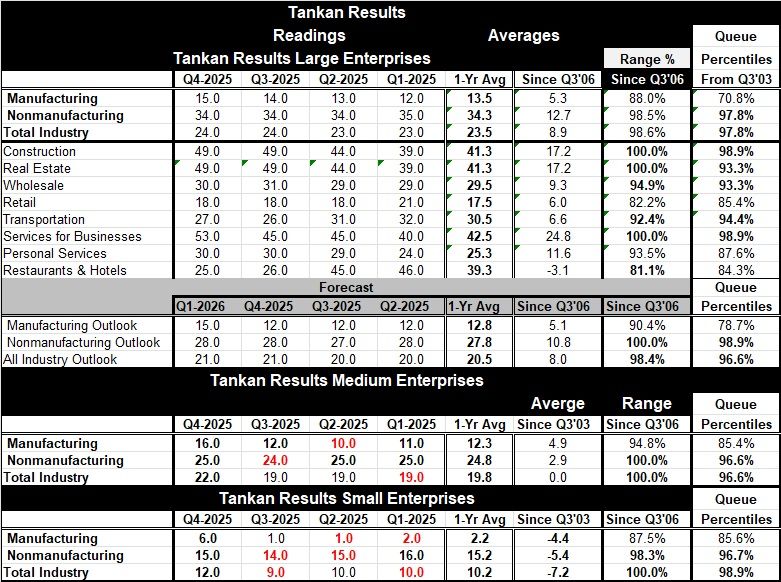

Tankan overview: Japan's Tankan report is an important quarterly assessment and outlook of the Japanese economy. Historically, the performance of manufacturers is considered to be the bellwether in this survey for performance of the economy. In the fourth quarter of 2025, the manufacturing index moved up to 15 from 14 in the third quarter. This compares to a value of 12 in the first quarter and a four-quarter average of 13.5. Since late-2006, the manufacturing index has averaged 5.3, marking the performance in 2025 as a substantial improvement from the long period where Japan struggled with deflation. On dated back to 2003, the manufacturing index has a standing in the queue of data in its 70.8 percentile, a reasonably firm reading.

Nonmanufacturers: The index for nonmanufacturers logged a reading of 34 in the fourth quarter compared to 34 in the third quarter and a reading of 35 in the first quarter of 2025; the one-year average for nonmanufacturers is 34.3, marking that sector as little changed over the course of the year. Nonmanufacturing in the fourth quarter has an index standing at its 97.8 percentile, marking it as an extremely high standing on data back to late-2003.

Nonmanufacturing details: Readings across the nonmanufacturing sector are above their respective one-year averages for all subsectors except transportation where the fourth quarter index backs down to 27 from an average of 30.5 and for restaurants & hotels that back down to a reading of 25 from an average of 39.3. The queue percentile standings for the subsectors show a good deal of strength with construction at a 98.9 percentile standing, services for businesses also at a 98.9 percentile standing, transportation - despite the back off from the average - is at a 94.4 percentile standing, and real estate and wholesaling are at 93.3 percentile standings on data back to 2003.

The Tankan outlook- The survey also produces an outlook. For large manufacturers for the first quarter of 2026, the outlook metric moves up to 15 from what had been 12 for the fourth quarter of 2025. The outlook for nonmanufacturers is flat month-to-month at 28, the same as in the fourth quarter. The outlook for manufacturing has a queue standing in its 78.7 percentile on data back to 2003, while nonmanufacturing has a standing for the outlook reading at its 98.9 percentile marking these outlooks as quite good.

The BOJ is watching- This is a survey the Bank of Japan will be looking at and assessing what policy should do and how strong the economy appears to be. On these data, the economy would appear to be firm, the outlook would appear to be solid, and if the Bank of Japan were to decide to pay more attention to inflation, the economy would seem to be in a position to absorb a rate hike without much difficulty.

Other-sized enterprises- Manufacturing: The survey also produces results for medium-sized and small-sized firms, as well as outlooks for medium-sized and small-sized firms (that are not presented in the table). The fourth quarter assessments of performance, however, show improvements for manufacturing in both medium- and small-sized enterprises; they also show rankings of medium-sized firms in manufacturing in their 85th percentile, the same as for small sized enterprises.

Nonmanufacturing: Nonmanufacturing for medium- and small-sized enterprises show improvements in the fourth quarter results and also demonstrates high rankings of those readings for those respective sectors.

Summing up: On balance, it's a solid Tankan report for Japan's economy and should provide reassurance to the Bank of Japan and to the current government that the economy is on solid footing as each looks at the situation and tries to assess the best policy options.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia