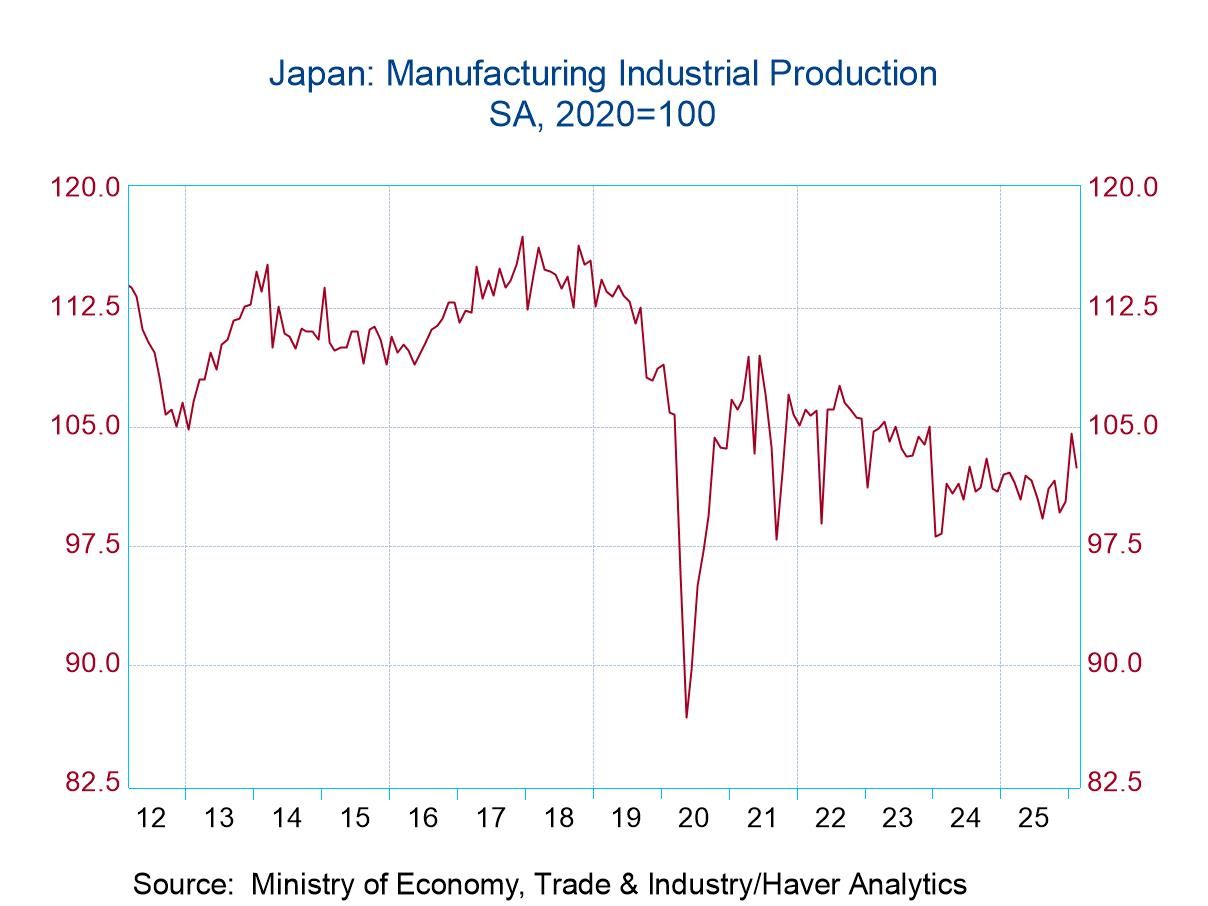

Japan’s IP: A Step Back in February

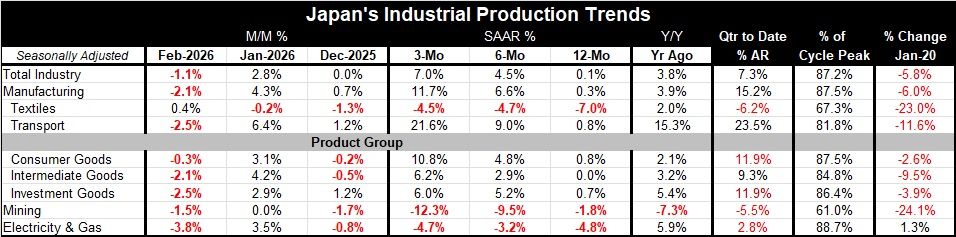

Japanese industrial production in February declined by 1.1%, led by a 2.1% drop in manufacturing output. By sector, consumer goods output fell by 0.3%, intermediate goods output fell by 2.1%, while investment goods output dropped by a strong 2.5%, all on a month-to-month basis. Mining sector output fell by 1.5% in February, while utilities output fell by 3.8%.

Sequentially, however, Japanese output had been accelerating, up by 0.1% over 12 months, at a 4.5% annual rate over six months, and at a 7% annual rate over three months.

Manufacturing Manufacturing output is up at 0.3% over 12 months, at a 6.6% annual rate over six months, and by 11.7% annualized over three months.

Within manufacturing, consumer goods output is expanding at a strengthening pace, rising by 0.8% over 12 months, at a 4.8% annual rate over six months, and then at a 10.8% annual rate over three months. Intermediate goods output is flat over 12 months, rising at a 2.9% annual rate over six months, and at a 6.2% annual rate over three months. Investment goods output is up at a 7% annual rate over 12 months, at a 5.2% annual rate over six months, and at a 6% annual rate over three months. However, mining output is down year-over-year; output changes get progressively worse from 12 months to three months. Utilities show a 4.8% decline over 12 months, decline by 3.2% at an annual rate over six months, and then fall at a 4.7% annual rate drop over three months. Mining and utilities sectors are experiencing more in the way of contracting effects.

Quarter-to-date Reported on a quarter-to-date basis (two months into Q1), total industry output is up at a 7.3% annual rate, with manufacturing up at a 15.2% annual rate on the same basis. For sectors, however, the strength is in consumer goods and investment goods where output is increasing at an 11.9% annual rate in the quarter; intermediate goods output is up at a 9.3% annual rate quarter-to-date. Mining output shows a decline at an annual rate in the quarter-to-date, while utilities output posts an increase.

The trends are good...but The trend data provide an upbeat assessment for Japanese output despite the setback in February. However, we know this isn't going to last. The global economy has run into a buzz-saw since then. Global PMI survey data took a sizable step back in March as the war with Iran began, and with oil prices spiking, all past trends are basically off the books, and we have to recalibrate everything. What we can see is that the Japanese economy was on a run and was doing better. It was beginning to make inroads before the Iran war took place.

Japan has a history of locking up oil supplies long in advance, so the economy may continue to have more resiliency to oil prices than other economies and compared to what people expect. On the other hand, if Japan has contracts to supply oil at a price and supplies cannot get out of the Middle East, those contracts may not count for much. However, there still are going to be perceptions and expectations for the future and concerns about what's going to happen to global demand—nobody is out of the woods yet. For now, trend-based data in Japan look extremely good; however, we know not to believe it will last. At this point, we're not sure what to expect next, except something that will be much worse.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global