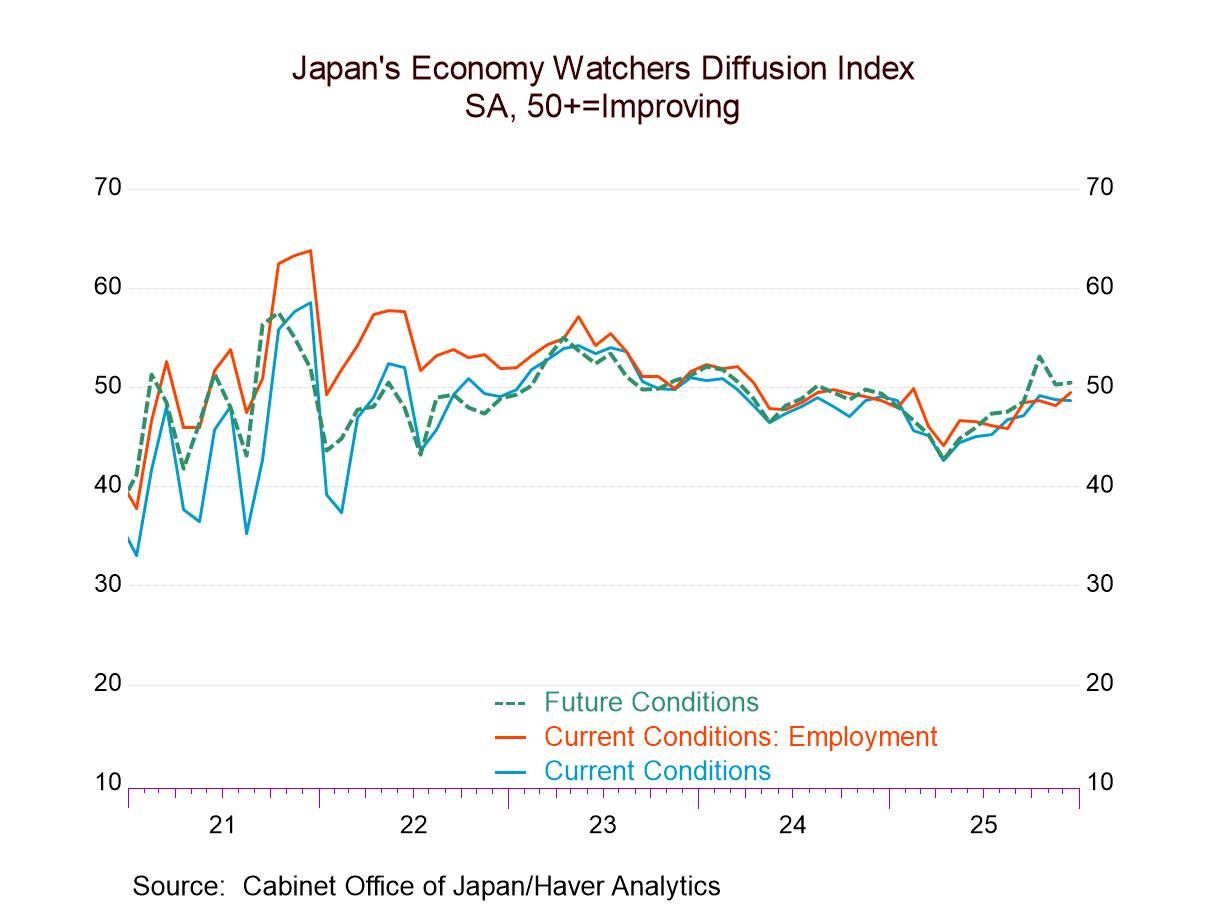

Japan’s Economy Watchers Survey in December 2025

Japan’s economy watchers index at year-end weakened slightly, but the future index strengthened slightly to counterbalance the drop-off. The December current index is weaker than it was in October as well, as is the headline for the future index. But the queue, or rank, standings of these indexes show the current index at a 60th percentile standing and a queue standing for the future index at its 70th percentile. Despite the end of year give back, the index headline readings are still, for the most part, firm-to-solid.

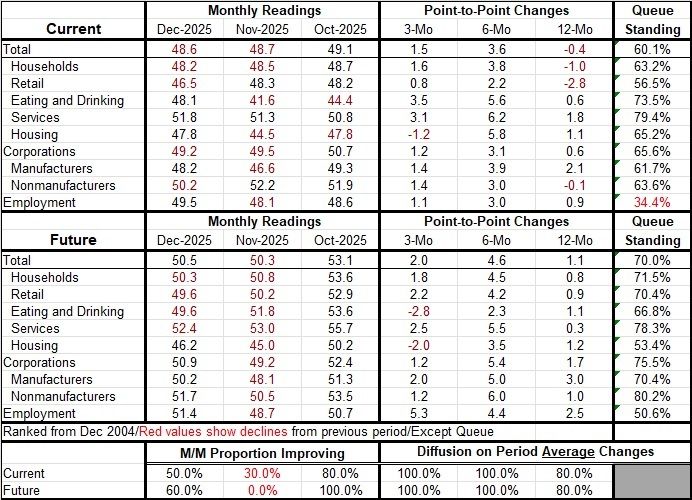

The Current Index That is an assessment about the rankings of the December data compared to their respective histories back to end 2004- a twenty-year period. However, in terms of the diffusion values of the index per se, the current index has only two readings above the 50 mark indicating actual expansion. Expansion is the rule in current services industries and in nonmanufacturing, a broader sector dominated by services. Employment and readings for corporations overall both show readings close to neutral with diffusion at 49.2 or better, but still short of 50. Current retail at 46.5 is the weakest sector and shows the second weakest diffusion reading.

The current index standings on employment has a reading below 50%- and that is despite having a diffusion reading near 50 -nearly unchanged employment month-to-month. That diffusion reading for December is a low relative to its own history. The strongest two sectors on rankings are services and eating & drinking places with standings in the 70-percentile range. Apart from the weak employment standing, the weakest rankings are in the range of the lower sixty percentiles with only retailing lower, in its 56.5 percentile, manufacturing at its 61.7 percentile.

The Future Index The Future index has a slightly higher queue standing than the current index as noted above, but it is not vastly different. No future components rankings are below their 50%, but again, employment is weakest with a ranking in its 50th-percentile and with housing in its 53rd percentile. Nonmanufacturing and services have the highest queue standings.

In terms of diffusion readings as opposed to standings, the future index headline is above 50 unlike for the current headline. Six of nine observations in December have future readings in their respective 50.6 percentiles. The weakest future reading, housing, with a 46.2 reading, is followed by retailing and eating & drinking places, each at 49.6. But the above-50 readings ae not strong per-se either. The strongest is the services sector at 52.4, then nonmanufacturing at 51.7, followed by employment at 51.4 (and it has the weakest queue standing among future readings). Corporations have a diffusion reading at 50.9, households at 50.3, and manufacturers at 50.2. And that 50.2 reading for manufacturers has a 70.4 percentile standing.

Always remember that diffusion and the rank standings are different things and very different concepts even though they are both measured as percentages; they can be quite different. Various series have different histories and tendencies. Not too surprisingly the current and future diffusion readings are highly correlated (0.96) while the standings are not so well correlated in December between the current and future (0.37). The correlation I speak about above between diffusion and standing is at 0.20 for the current readings in December but is higher at 0.53 for the December future components.

Summing up The differences in the diffusion values tell us that retailing, households and employment are expected to pick up over the next six months. But housing is expected to weaken.

Japan is still in a fragile state with a relatively new PM still getting adjusted (but rumored to be considering an early snap-election). And with the economy generating excess inflation even with a shrinking population, addressing inflation in Japan is trickier since the Bank of Japan does not want to slay inflation at the cost of bringing back deflation. So, policy is Japan walks on eggshells.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief