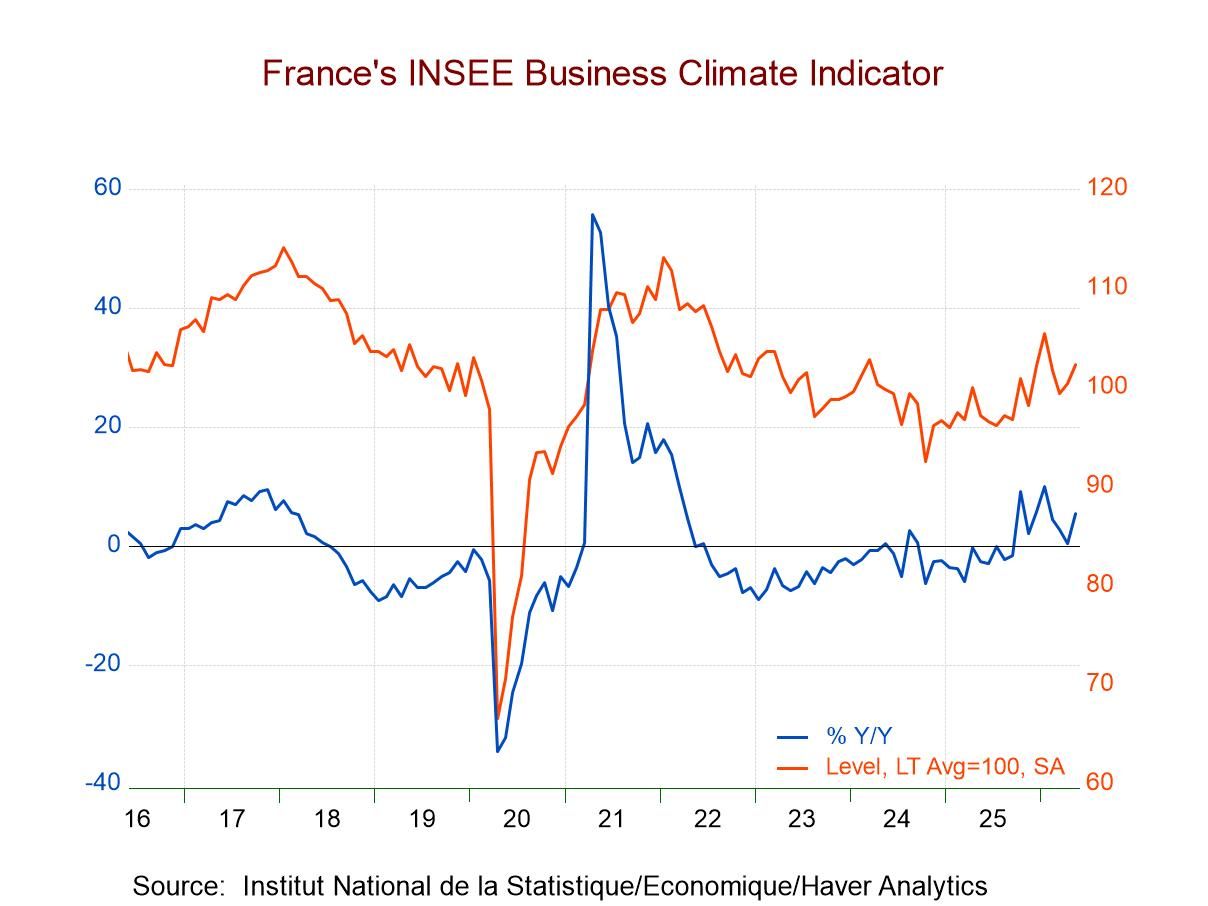

INSEE: French Manufacturing Rebounds Amid Weakness

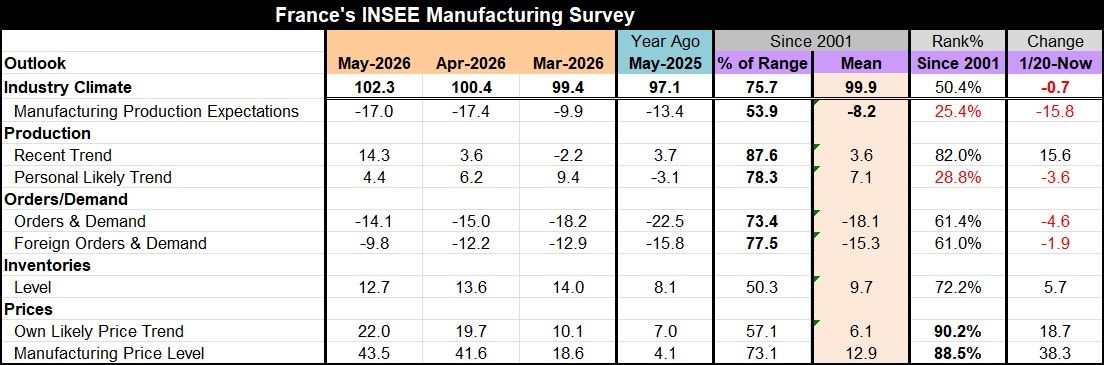

The French manufacturing climate index improved in May, rising to 102.3 after climbing to 100.4 in April from 99.4 in March.

Despite the improvement, the standing of the climate index is only at its 50.4 percentile, leaving it just slightly above its historic median on data back to 2001. Industry climate now is still slightly lower than it was in January 2020, just before COVID hit.

The survey components tell a mixed story about prospects for industry in France. Manufacturing production expectations improved slightly in May, moving to -17.0 from -17.4 in April; however, both readings were sharply weaker than the value in March. The standing of production expectations in May is at its 25.4 percentile, marking it as just a hair above its lower quartile when ranked on data back to 2001. This is a weak and uninspiring showing.

The recent trend of production is much more upbeat, rising to 14.3 in May from 3.6 in April. It also shows a sharp improvement compared to a year ago, when the value was 3.7. Its standing is significantly above its historic mean, and the ranking for this May observation is at its 82nd percentile—a solid showing. It is the strongest response in the survey among demand and activity variables. But can that trend hold?

The personal likely trend, in which survey respondents respond to prospects for their own firms and industries, shows much less ebullience, with the May reading of 4.4 and a steadily diminishing trend from March to April to May. The personal likely trend is still stronger than a year ago, when it was -3.1, although it is significantly below its historic mean, with a ranking at its 28th percentile. It is a reading that is nearly completely decoupled from the recent trend responses in this same survey.

Orders and demand in May improved to -14.1 from -15 in April; in April, the index had improved from -18.2 in March. There is a similar trend and improvement for foreign orders and demand as well. Both overall and foreign demand are improved compared to a year ago; both are stronger than their historic means, and each of the series has a ranking in its 61st percentile—above their respective historic medians with some margin, enough to say the responses look firm. Yet, there is not enough to say they look strong. Both readings are still below their levels in January 2020, before COVID struck.

The INSEE survey also includes two observations on prices: the own-likely price trend and the manufacturing price trend. Both have been moving up sharply from March to April to May; both are significantly above their year-ago levels and relatively strong compared to their historic means. Both series also have high percentile rankings, with the own-likely price trend at a 90.2 percentile ranking and the manufacturing price level at an 88.5 percentile ranking. Both are also substantially above their levels of January in 2020, before COVID struck.

Summing up What we're seeing in this survey is some signs of strength from the recent production trend; however, pessimism by respondents about their own industry is an offset to that. There is some firmness in overall orders & demand and foreign orders & demand, but it's not yet strong and the outlook for prices and inflation is a considerable negative. With rising oil prices, the outlook for inflation is not surprising, and we're going to have to wait and see what tactics the European Central Bank takes in order to have an idea how hard this might hit the economy. Industry climate and order demand have been creeping up, but the weakness in manufacturing production expectations is a sharp counterpoint to keep in mind. In short, the INSEE manufacturing survey has a number of contradictions and significant question marks that should make us wary about the outlook.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Asia

Asia