Industrial Sector Remains Under Pressure in EMU

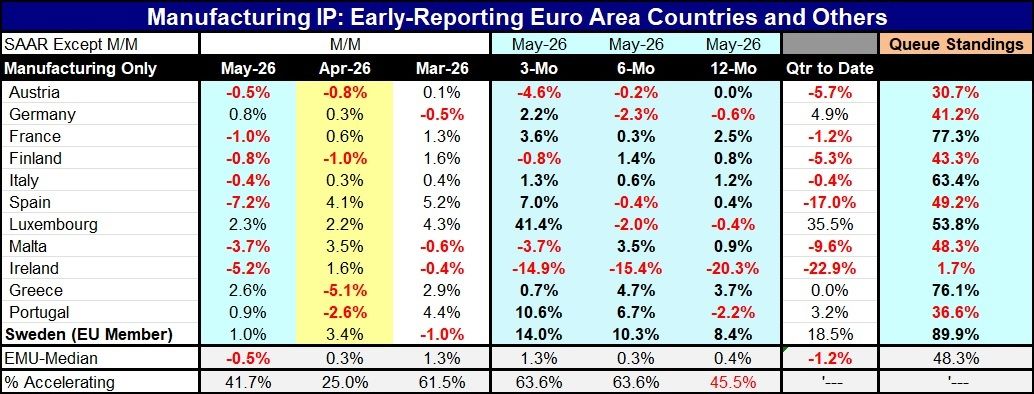

Manufacturing output in the countries of the European Monetary Union continues to underperform. The median change for the 11 countries reporting on the table is a 0.5% decline in May following a 0.3% increase in April. However, only 41.7% of the reporters are accelerating in May, compared to 25% in April, although in March over half of the reporters had showed some acceleration, with output at 61.5%.

In May, of these eleven early reporters, seven showed month-to-month declines in output. This compares to four showing declines in April and four showing declines in March.

Sequential trends Over 12 months, output is declining in four of these eleven countries: Germany, Luxembourg, Ireland, and Portugal. Over six months, output declines in five of the eleven countries. Over three months, output declines in four of the eleven countries. Over these broader sequential periods, output is increasing in most cases; only one country, Ireland, shows consistent declines in output over three months, six months, and 12 months. However, among EMU countries, only Italy shows output expanding on all three timelines, although Sweden, an EU member country, also shows output increasing in all three periods.

Amid the output weakness in May, the quarter-to-date calculation for industrial production growth is also broadly weak. In May, seven of the eleven quarter-to-date changes in industrial production are negative. Positive results, increases in the quarter-to-date, are registered by Germany, Luxembourg, Greece, and Portugal.

The ranking of the year-over-year growth rates shows seven countries with output growth rate rankings below 50%, marking them as below their respective medians. The comparisons for output growth are taken back to 2006, a period of about 20 years.

Four EMU countries rank above their twenty-year medians: France, Italy, Luxembourg, and Greece.

The snapshot of industry in the monetary union is consistent, showing little momentum, little strength, and relatively low rankings for current growth rates; only a minority of reporters show an acceleration in growth in May compared to April. With the situation in the Strait of Hormuz deteriorating again, the outlook for industrial production has to remain guarded.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global