Asia| Jul 13 2026

Asia| Jul 13 2026Economic Letter from Asia: The AI Underbelly

In this week's Letter, we examine the underbelly of the AI boom, the risks that sit beneath its optimism. Start with the public mood: American concern about AI has grown alongside adoption over the past three to four years (chart 1). Those worries span mass job displacement, misuse of top-end models by bad actors, and fears of being left behind. The first of these is already surfacing: in June, AI was again the most cited reason for announced US layoffs, with year-to-date AI-linked cuts above 100,000 (chart 2). Technology led all sectors in overall cuts, though the data do not isolate how many were AI-driven. Among those hit, the young are arguably the most exposed to these labour effects. They enter a labour pool swollen by displaced professionals, just as AI masters the entry-level tasks where they would start. India and Indonesia illustrate the stakes on youth NEET, the share not in education, employment, or training, both above 20% and among Asia's highest (chart 3). Beyond the labour market, the same optimism reshapes asset prices. The rally has lifted AI-related valuations to historic highs and concentrated a few names in cap-weighted indexes (chart 4). That raises correlation and the risk of a sharper index fall should the rally unravel. The same concentration runs through economies via exports, from Taiwan's advanced chips to South Korea's memory (chart 5). Its footprint is physical too, and cuts both ways: data-centre investment has lifted growth in Johor, Malaysia (chart 6) while straining local power and water. None of this argues against riding the AI wave, which still promises real productivity and welfare gains. Rather, these are caveats that investors and policymakers must keep in view, since the story is not all upside.

AI-related concerns AI adoption has exploded over the past three to four years, and Americans' concerns have risen alongside it (chart 1). That is understandable, given how advanced and broad AI's proven applications have become. They now span everyday tasks and subject-specific work across fields such as finance and production, as well as tech and development, the sector AI was born in. Major concerns run from mass AI-induced job displacement to a more recent fear, that top-end models fall into the wrong hands and are used by bad actors. A further worry is distributional: AI advances are powerful and could deliver leaps in productivity, yet they may also leave many people behind. Those most exposed include workers already displaced from their jobs and people facing scarcer basic resources as AI demand competes for them. Others simply lack equitable access to AI tools or their benefits.

Chart 1: Americans’ views about AI

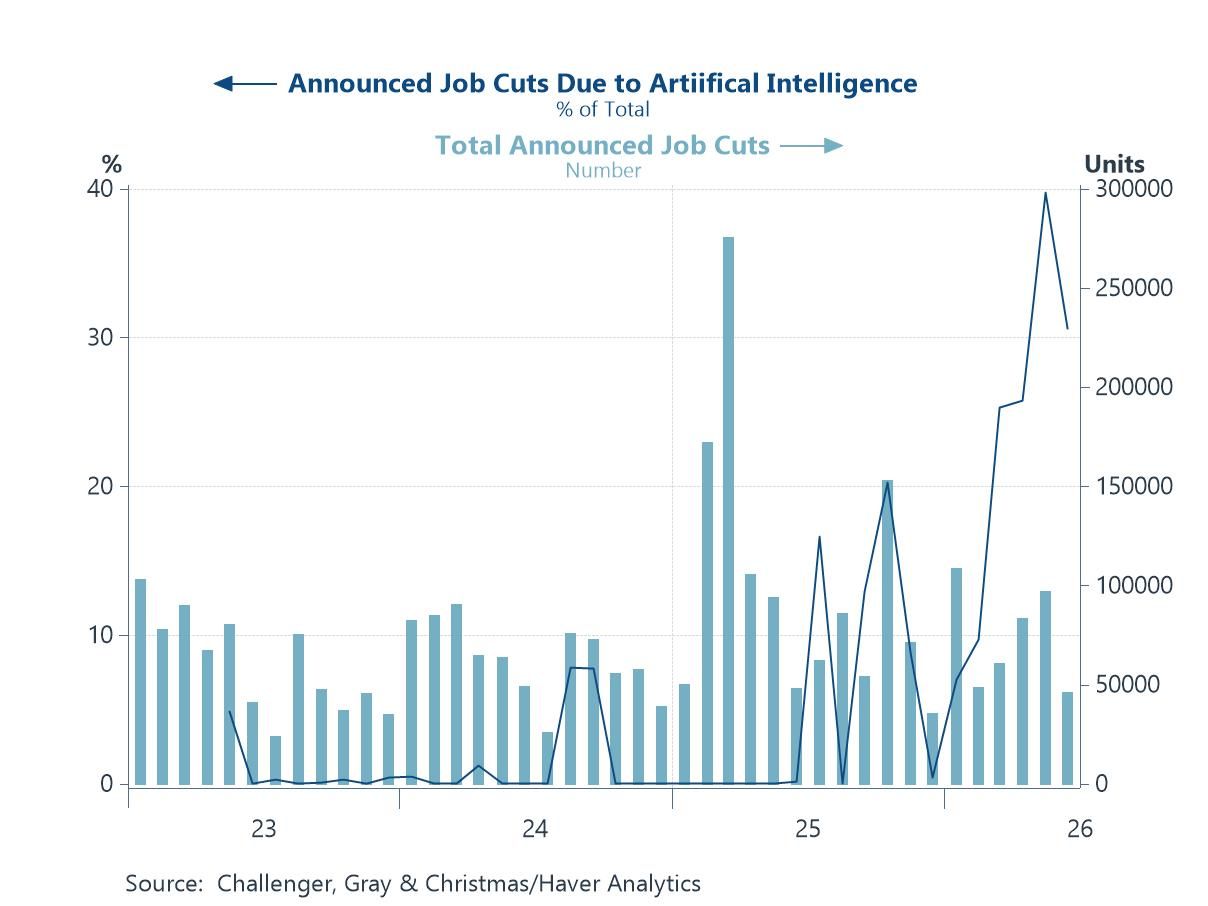

AI-driven job displacement Some of the fears US workers first had about AI-driven job displacement are already playing out. In June, AI was again the most cited reason for announced job cuts in the US (chart 2). That pushed year-to-date job cuts attributed to AI above 100,000, more than half of all AI-tagged cuts since AI became a selectable reason in 2023. The data come from the latest survey by Challenger, Gray & Christmas. This likely reflects AI's disproportionately heavy impact on certain industries such as technology, which again led all sectors in cuts. At the same time, announced hiring plans stayed subdued, leaving laid-off workers with limited opportunities to find new roles. All of this is occurring even as market valuations remain elevated on the broader wave of AI optimism.

Chart 2: US job cuts due to Artificial Intelligence

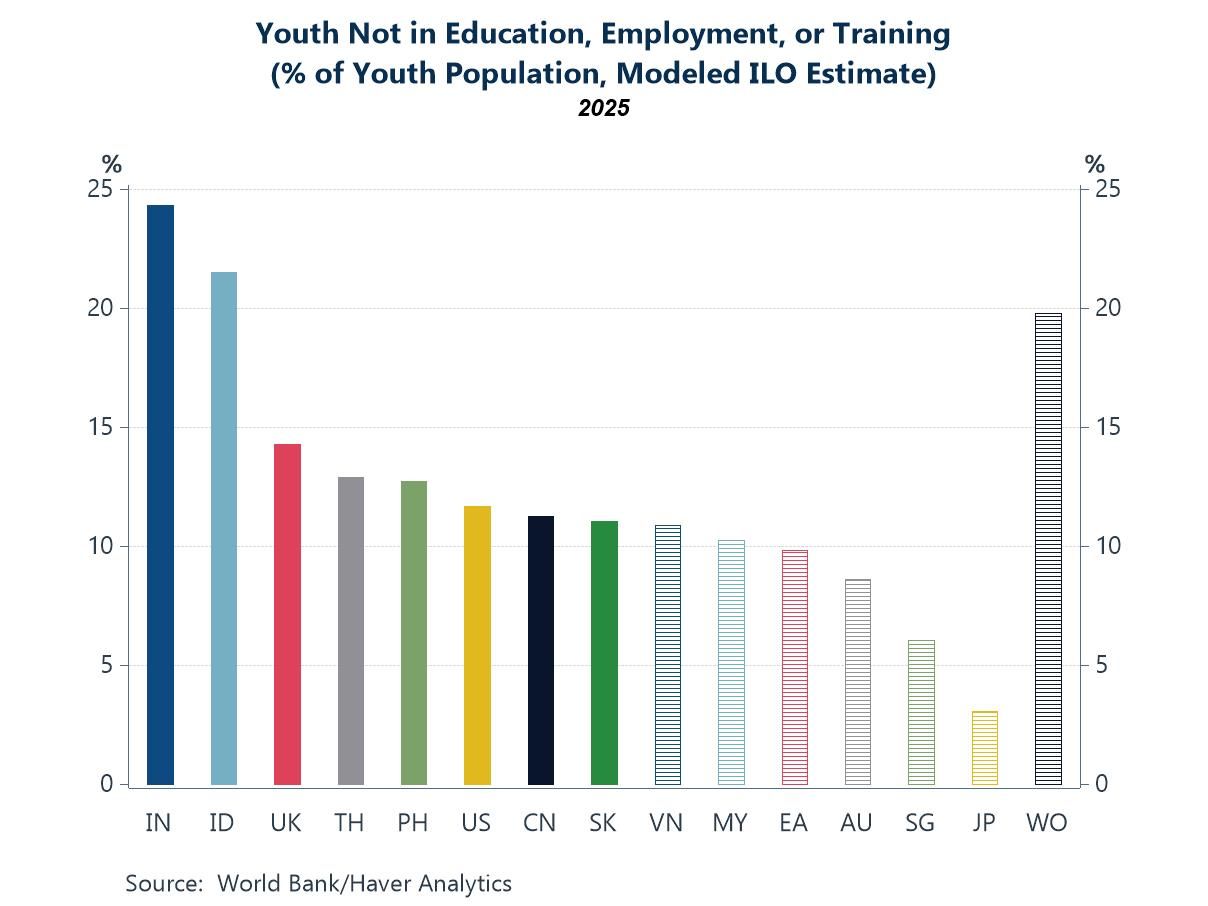

AI and youth unemployment Arguably among those bearing the brunt of these labour-related effects are the youth. Many have graduated on a curriculum built largely for a pre-AI era. They now enter a labour pool swollen by experienced professionals whom AI has displaced. At the same time, AI is proving especially capable at the entry-level tasks on which young workers usually start. An elevated youth unemployment rate only intensifies the competition young people face for gainful employment. On the broader NEET measure, which also captures youth who are neither working nor studying, India and Indonesia stand out. On the latest available WDI data, both have youth NEET rates above 20%, among the highest in Asia and above the global average (chart 3). Should employers in these economies adopt AI aggressively across processes and production, including physical AI such as humanoid robots, the problem could worsen. Yet firms that stay purely labour-intensive risk losing out to rivals using more efficient, and perhaps cheaper, AI-driven methods.

Chart 3: Youth not in education, employment, or training

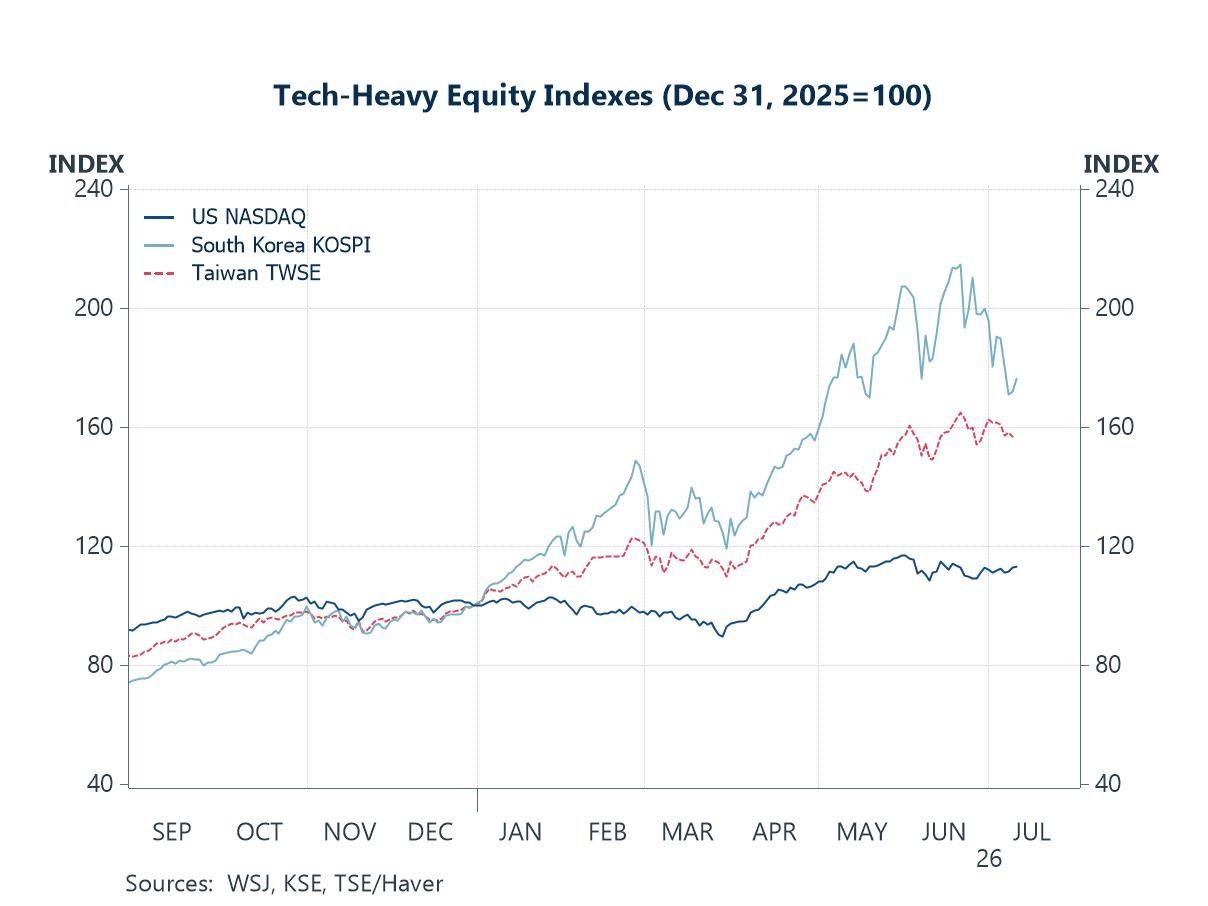

Concentration risk The recent wave of AI optimism has pushed the equity valuations of major AI developers and AI-related goods producers to historically high levels. These gains are partly backed by strong earnings and upbeat forward guidance. Most major indexes are weighted by market capitalisation, so a counter's weight tracks its price. As these counters have outperformed their peers (chart 4), their index weight has risen close to mechanically, when holding the number of shares constant. This raises concentration risk, since a small group of counters now carries more of the index and moves it more closely. So, if the rally in these counters were to unravel deeply, it would drag the broader index down more heavily with it.

Chart 4: Tech-heavy equity indexes

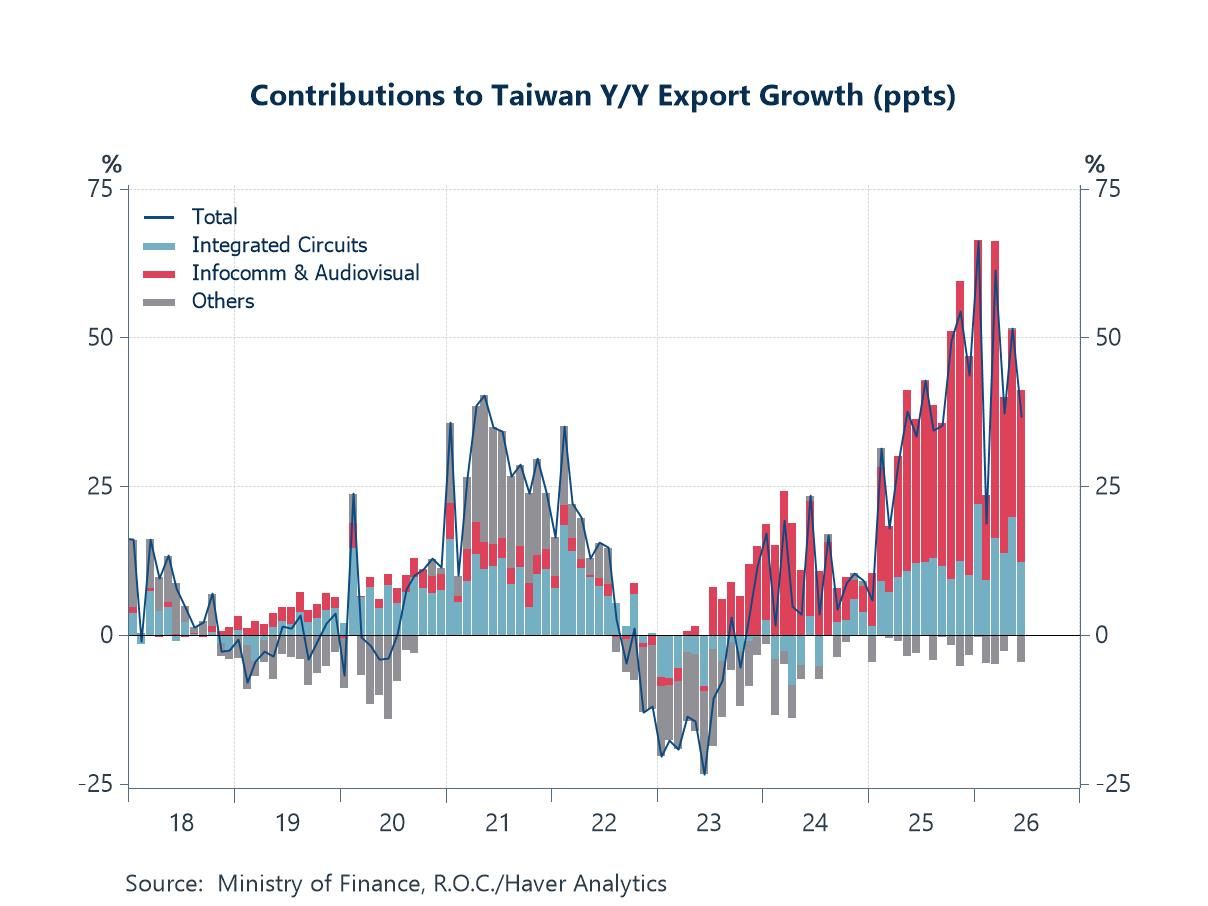

AI-related concentration risk is not confined to equity indexes; it also shows up in the growth of major economies. In Asia, that risk usually runs through a country's exports. Take Taiwan, the world's largest advanced semiconductor exporter, as an example. As chart 5 shows, its recent export growth has come more than entirely from integrated circuits and from infocomm and audiovisual equipment. Other goods categories have often contributed negatively in recent months. This is good news for the Taiwanese economy, which sits right at the centre of the global AI boom. Yet it is also a source of concentration risk, should AI-related goods demand collapse or substantial alternative supply emerge elsewhere. A similar story applies to South Korea, through its role in supplying high-end memory chips.

Chart 5: Contribution to Taiwan export growth

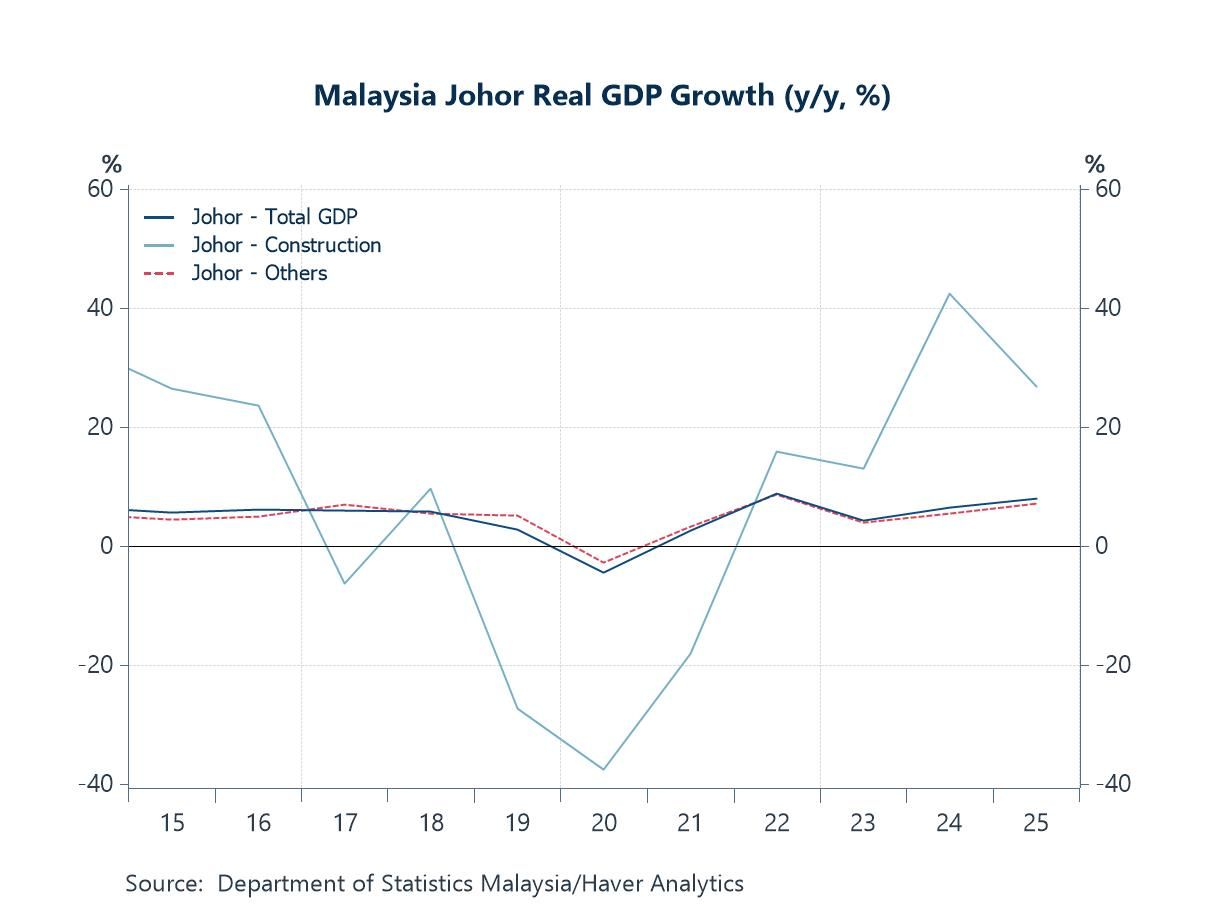

Data centres, energy, and water Finally, rapidly advancing AI promises major productivity gains and broad improvements to daily life. Yet AI infrastructure rests on resource-intensive inputs: the energy needed for data centre compute, and the water needed to cool those centres. Both may deprive real people of the very resources they need to survive. One recent hotspot is Malaysia, which has courted a wave of foreign direct investment to expand its data centre footprint in the state of Johor. These capital inflows are welcome, and have lifted state-level growth through the construction sector (chart 6). But they have also raised concerns about straining local grids and water supplies, possibly leaving less for residents. Among estimates, a recent one puts data centres at around 40% of Johor's electricity demand by 2035. That is pressuring the state to expand generation capacity and grid access to match the data centre pipeline already in place. Its neighbour Singapore faced similar strains earlier, and has since repositioned itself as a hub for the most advanced and efficient data centres, partly because of its severe land constraints.

Chart 6: Malaysia Johor State real GDP growth

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief