Import and Export Prices: Firm in May

Summary

- Petroleum products led import prices higher, but capital goods also had an influence.

- Petroleum was also a factor on the export side; some stirring in food and capital goods.

The headline index on import prices rose 1.9% in May, close to the blistering pace in April and the fourth consecutive high-side reading. This recent pressure has pulled the year-over-year change to 6.7%, a distinct shift from last year when import prices showed no change over the 12 months of 2025.

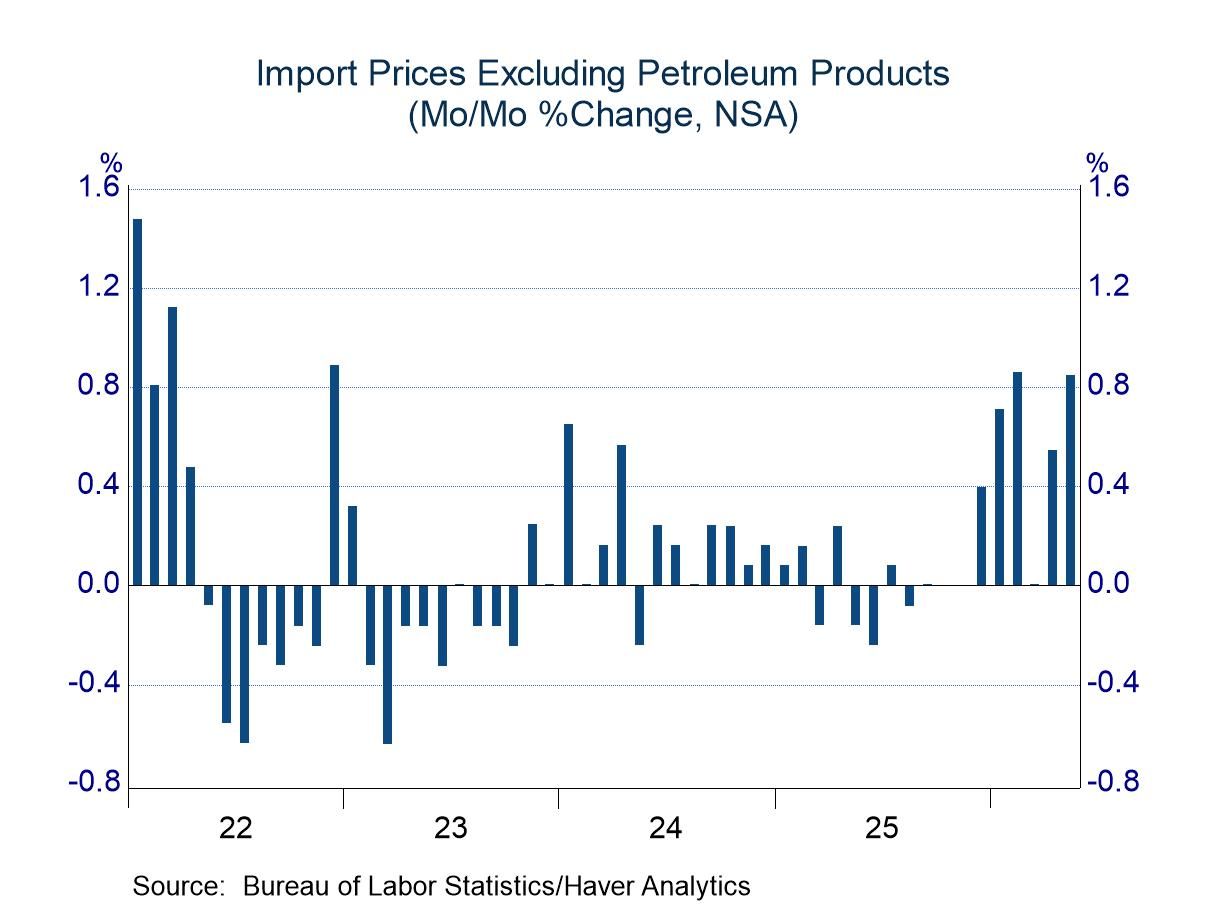

Prices of petroleum products have been the most important factor behind the recent surge, increasing 13.0% in May after an average of 17.8% in the prior two months. However, prices excluding petroleum products also have stirred this year, as they have increased more than 0.6% in each of the past five months. May posted the firmest increase in this string of brisk readings (1.3%). Prices of consumer goods had been increasing moderately in early 2026, but they jumped 0.5% in May. The changes in capital and consumer goods led to an increase of 0.8% in nonpetroleum prices in May and an average of 0.6% in the first five months of the year.

Some observers might seek to look for the effects of tariffs on import prices, but these figures would not be especially helpful in this regard, as prices are recorded before the imposition of tariffs. However, if foreign producers wished to absorb the tariff burden to remain competitive in the US market, they could reduce invoiced prices to keep post-tariff prices steady. Indeed, nonpetroleum prices softened after April of last year following the announcement of President Trump’s Liberation Day tariffs. The subsequent easing of some of the draconian tariffs and the nullification of tariffs imposed under the International Emergency Economic Powers Act might be factors leading importers to return to original prices this year. Given that the pressure on import prices ex-petroleum has been concentrated in the capital goods area, there does not seem to be a rush to return to pre-tariff pricing.

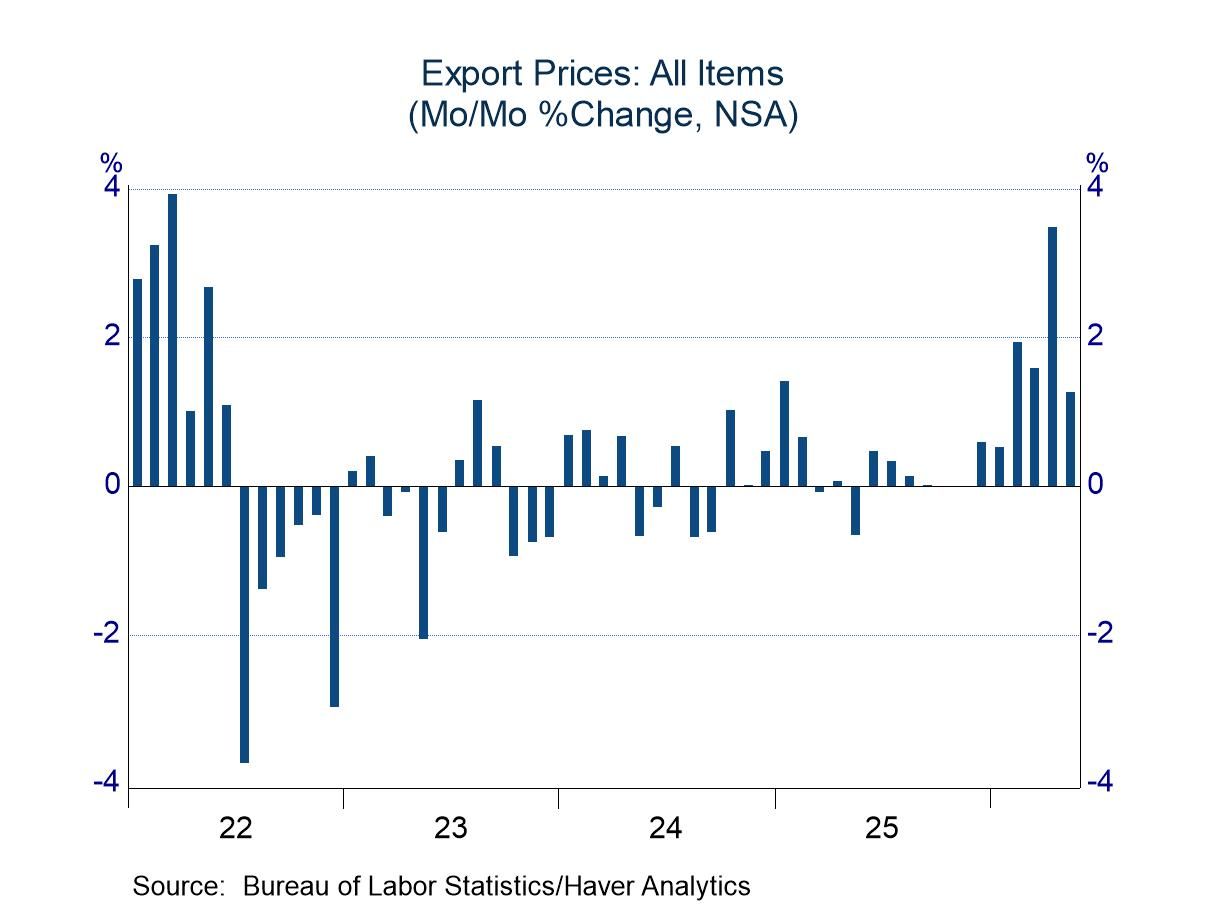

On the export side, prices rose 1.3% in May, continuing the firm pace seen in the preceding four months. Petroleum prices have played a role in this pressure, as shown by an increase of 2.4% in the industrial supply category (petroleum prices alone are not available on the export side). Food prices also have jumped this year, increasing 0.8% in May after an average of 1.2% in the prior three months. Prices of capital goods were tame in the early months of the year, but they have firmed in the past two months (0.5% in April and 0.7% in May).

These import and export price series are not seasonally adjusted; they can be found in Haver’s USECON database. Detailed figures are available in the USINT database. The expectations figure from the Action Economics Forecast Survey is in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Asia

Asia