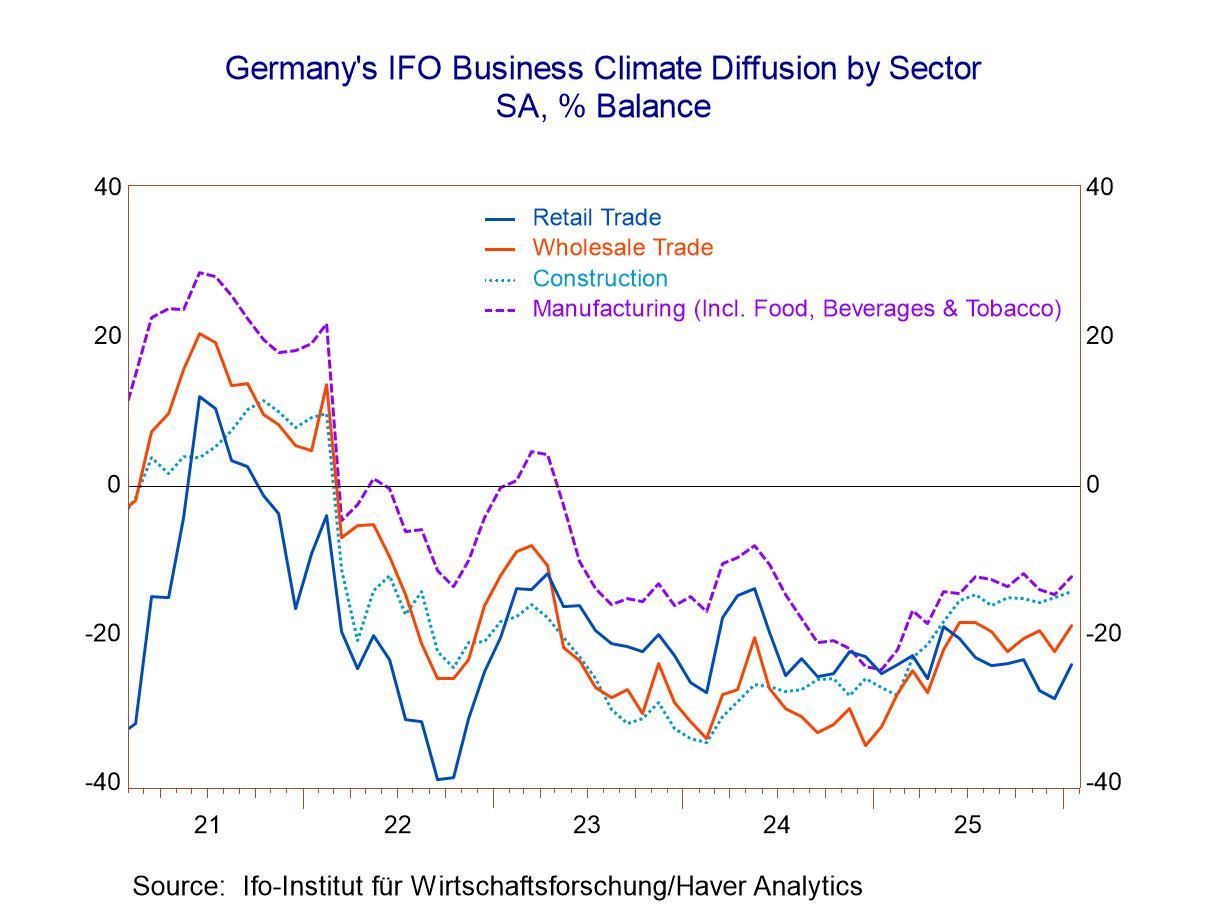

IFO Readings for Germany Mostly Waffle; Services Lag

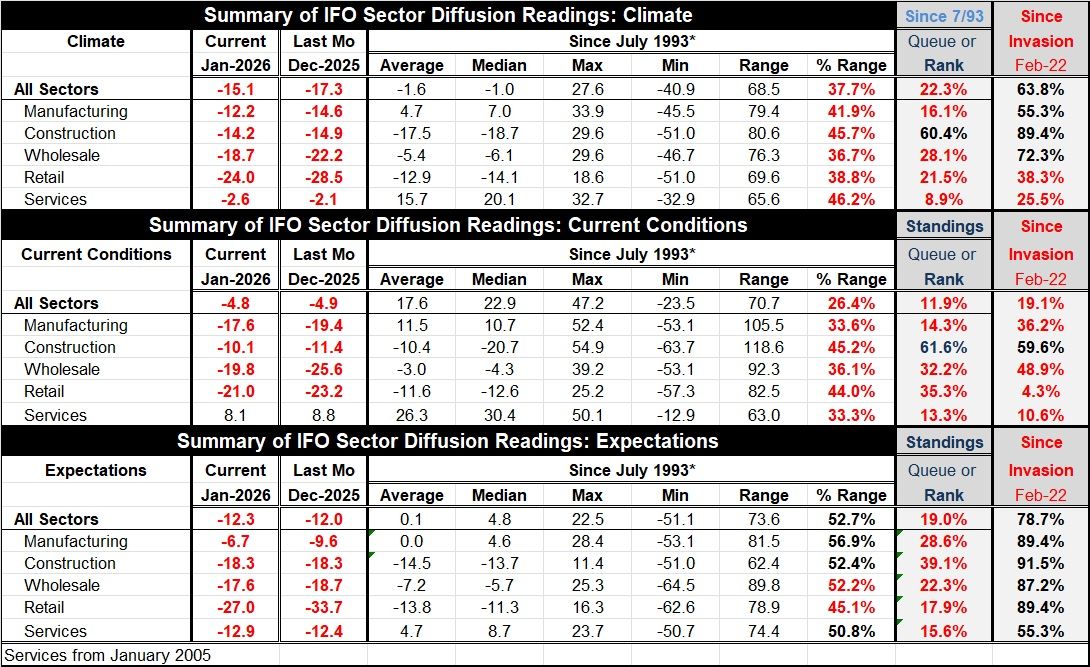

Germany’s IFO readings in January show a bit more strength in the climate reading, nearly unchanged current conditions, and nearly unchanged expectations. These readings that tend toward small changes or unchanged readings are - and have been - characteristic of the IFO survey for most of 2025 where the various sector readings basically made some improvement through about the first quarter of the year and then pretty much flatlined for the rest of the year. Growth Dynamics in Germany have become fairly stagnant. The question is when something will occur that will light a fire under growth or, more unfortunately, send the economy back into a tailspin.

The climate readings on long-dated rankings are all weak with only one reading for construction above its 50th percentile and data back to 1993. However, on a shorter timeline looking at conditions just since February 2022 that marks the invasion of Ukraine, we have the climate reading at a 63.8 percentile standing, construction at an 89.4 percentile standing and wholesaling at a 72.3 percentile standing. Manufacturing also manages a positive standing at its 55.3 percentile.

Month-to-month in January, there are small changes afoot across the five sectors and all of them show some modest improvement except for services that backtrack slightly moving from a reading of -2.1 in December to -2.6 in January.

Current conditions show almost no change at all with a -4.8 reading in January compared to a -4.9 reading in December. Across sectors in January, there's about a two-point improvement in manufacturing, a small improvement in construction and more sizable improvement in wholesaling, a small improvement in retailing, and a step back for services.

For current conditions, the percentile standings on the long-view to 1993, again, show only construction with a reading above its 50th-percentile - that is, above its historic median - at 61.6%. The all-sector reading has only a 11.9 percentile standing which is quite weak and generally weaker than the individual sectors. That fact simply underpins the notion of how this coincident-weakness across all the sectors is unusual because the all-sector index has a weaker ranking than any of the individual industries or sectors on the long timeline. On the shorter timeline, construction, again, is at a 59.6 percentile reading, above its 50th percentile, wholesaling comes close at a 48.9 percentile, reading retailing is exceptionally weak at a 4.3 percentile reading, and services are at a 10.6 percentile rating also quite weak. The current index is dominated by weakness.

Expectations in January show a step back for the overall reading and that's based on weakness in services. There are nearly 3-points of improvement in manufacturing, unchanged readings in construction, a slight improvement in wholesaling, a sizeable 6-point improvement in retailing, and a weaker reading from services, which back off by half a point on the month. The percentile standings when data are ranked over the long period to 1993 show everything below the 50th percentile; all rankings are below their historic medians on that timeline. However, when compared to February 2022, marking the invasion of Ukraine, all of the readings are above their 50th percentile, generally in about the 80th or 90th percentiles, except for services that only manage a ranking in the 55th percentile.

Summing up Across these three different concepts of climate, current conditions, and expectations, we see the most consistent firmness from the construction sector. We also see improvement in manufacturing, and generally from wholesaling, and more substantial improvement from retailing. The weakness stems from the services sector which shows a step back on all three of the concepts. Services are particularly weak when we rank them on the long-time horizon although current conditions are also quite weak for services in January alone and on the short-time horizon (relative to other sectors). What's encouraging in this survey is the improvement in sectors outside of services, but the services sector is the job creating sector and so having it as the lagging reading across all these dimensions is a problem. It is something that should hold back an optimistic view of the future.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global