German Output Scores Unexpectedly Strong Gains in October

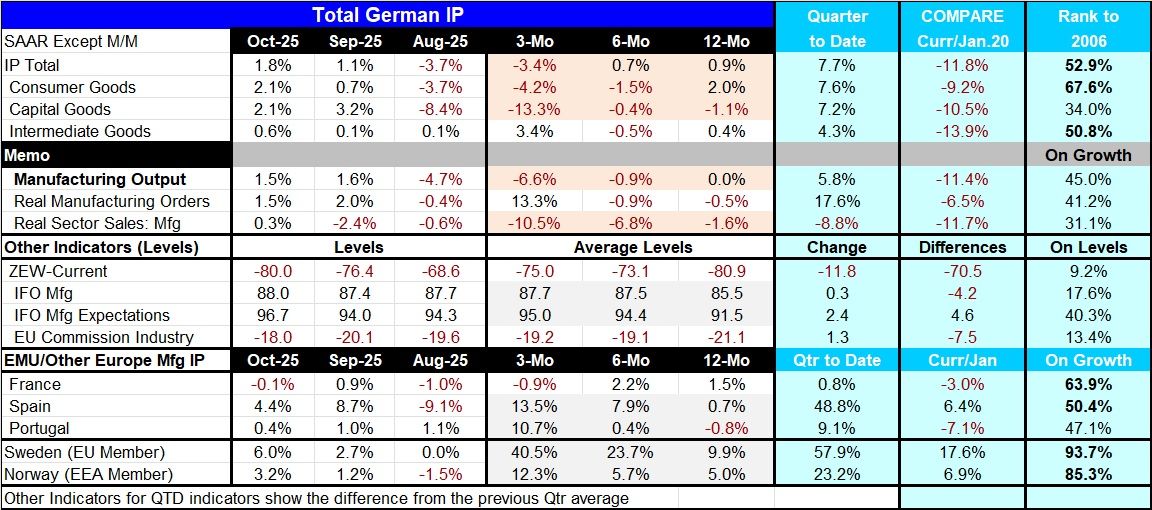

German growth brought a surprise to the upside in October when industrial production rose by 1.8% after rising 1.1% in September and falling by 3.7% in August. German output saw gains of 2.1% in consumer goods output, 2.1% in capital goods output, and 0.6% in intermediate goods output on a month-to-month basis in October. Each of these categories saw output increase in the last two months in a row. However, for most of these sectors’ output declined and fell rather sharply in August.

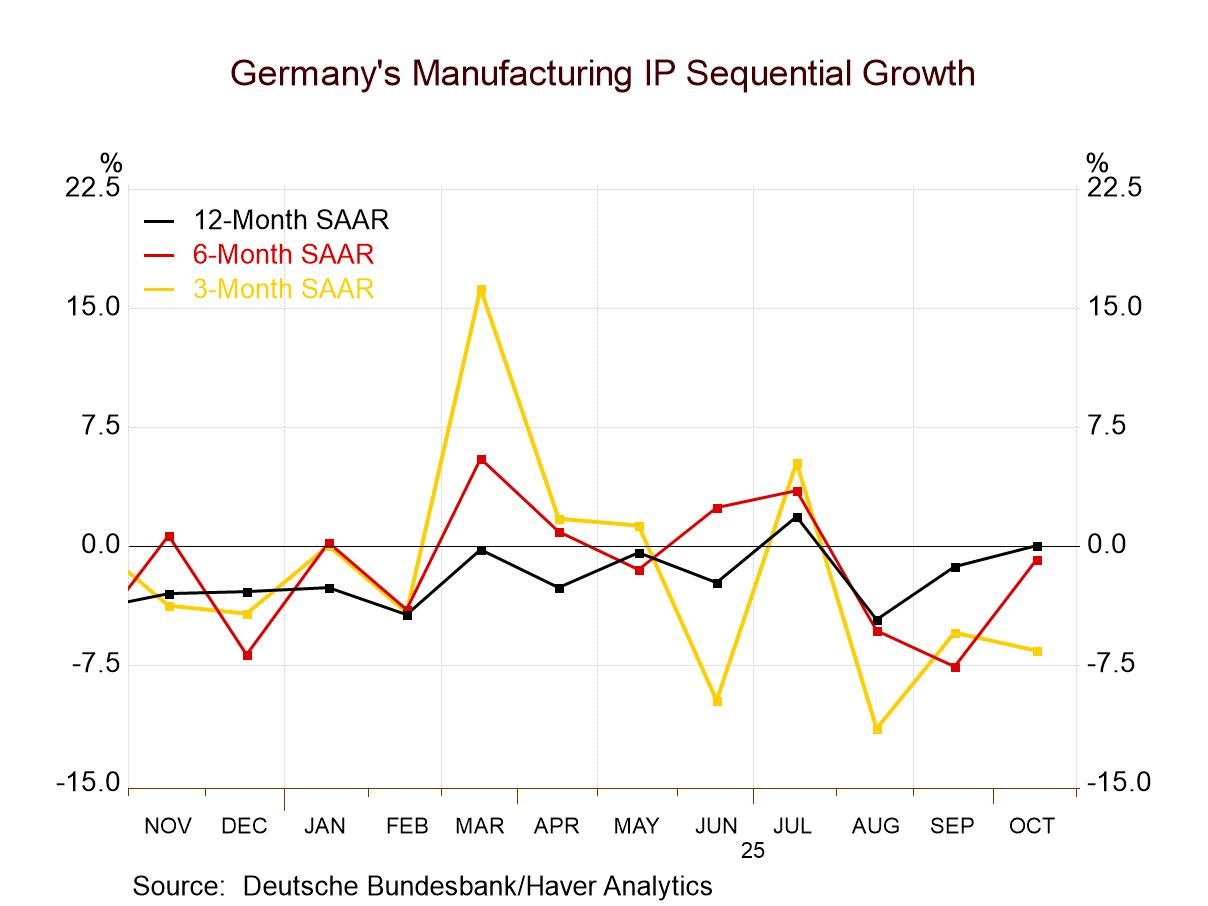

As a result, of these monthly gyrations, we're staring at somewhat unusual and mixed trends. The monthly trends are encouraging. However, the sequential trends from 12-months, 6-months and 3-months show a steady deceleration in total industrial production growth, a steady deceleration in consumer goods production’s pace, a steady deceleration in the output of the capital goods sector as well, all of those contrasted to a mixed sequential performance with a strong three-month gain for intermediate goods output. The manufacturing sector as a whole, apart from total industrial production, also shows output on a decelerating path from 12-months to 6-months to 3-months. Near-term strength has not been able to override a negative overall trend.

Industrial orders are showing a mixed performance with some strength tagged on at the end over three months. Real manufacturing orders fall by 0.5% over 12 months. They fall by a slightly faster 0.9% annual rate over six months, but then they rise at a 13.3% annual rate over three months. The three-month pickup is reassuring, but it's still not strong enough to drive the year-over-year change into positive territory.

Real sales of manufactured goods are also weak, falling by 1.6% over 12 months, falling to a 6.8% annual rate over six months and then accelerating their drop to a 10.5% annual rate decline over three months. The decline in inflation-adjusted sales growth pace is a disturbing trend, and it mirrors the underlying decline in manufacturing output.

Industrial indicators from the ZEW group, the IFO, and the EU Commission send a somewhat mixed picture monthly. Three of these metrics the IFO manufacturing survey, IFO expectations and the EU Commission index improved in October although the ZEW current index fell relatively sharply in October compared to September. Sequentially the analysis changes with both of the IFO readings for manufacturing and for manufacturing expectations showing progressive improvement from 12-months to six-months to 3-months. However, for the ZEW current index and for the EU Commission survey, the patterns remain mixed although there is improvement in the sense that the 3-month readings are stronger than the 12-month readings.

Turning back to industrial output data, we have readings from five European economies, three of them are monetary union-even countries. Spain, Portugal, Sweden, and Norway, each show progressive improvement in industrial output as the expansion rate for output improves from 12-months to 6-months and from 6-months to 3-months. In France, output increases over 12 months, even steps up its growth pace over six months but then it logs a decline over three months.

Quarter-to-date all industrial output metrics are showing gains of sone sort for the German sectors and for the European economies. German real orders are rising strongly early in the new quarter while real sales are falling. As for the indicators, the ZEW current index is dropping in Q4 compared to Q3, but the other industrial metrics show gains.

For more perspective, the queue rankings of indicators are generally below their midpoints. However, German sector industrial production and the country-level production in manufacturing are generally showing year-on-year growth rate above their historic medians on data back to 2006. Exceptions are that capital goods output is below its median pace, while German total IP is above its median; the growth rate for Germany manufacturing is not. France, Spain, Sweden, and Norway show year-on-year growth above their historic median pace, but in Portugal the ranking is at its 47th percentile, slightly below its historic median.

The bottom line is that October is an upside-disturbing surprise. It dove-tails with the better performance from the Baltic dry goods index. But the longer-term trends in Germany are still negative, with output in the other European countries in the table is generally on an upswing. Germany is not out of the woods yet.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global