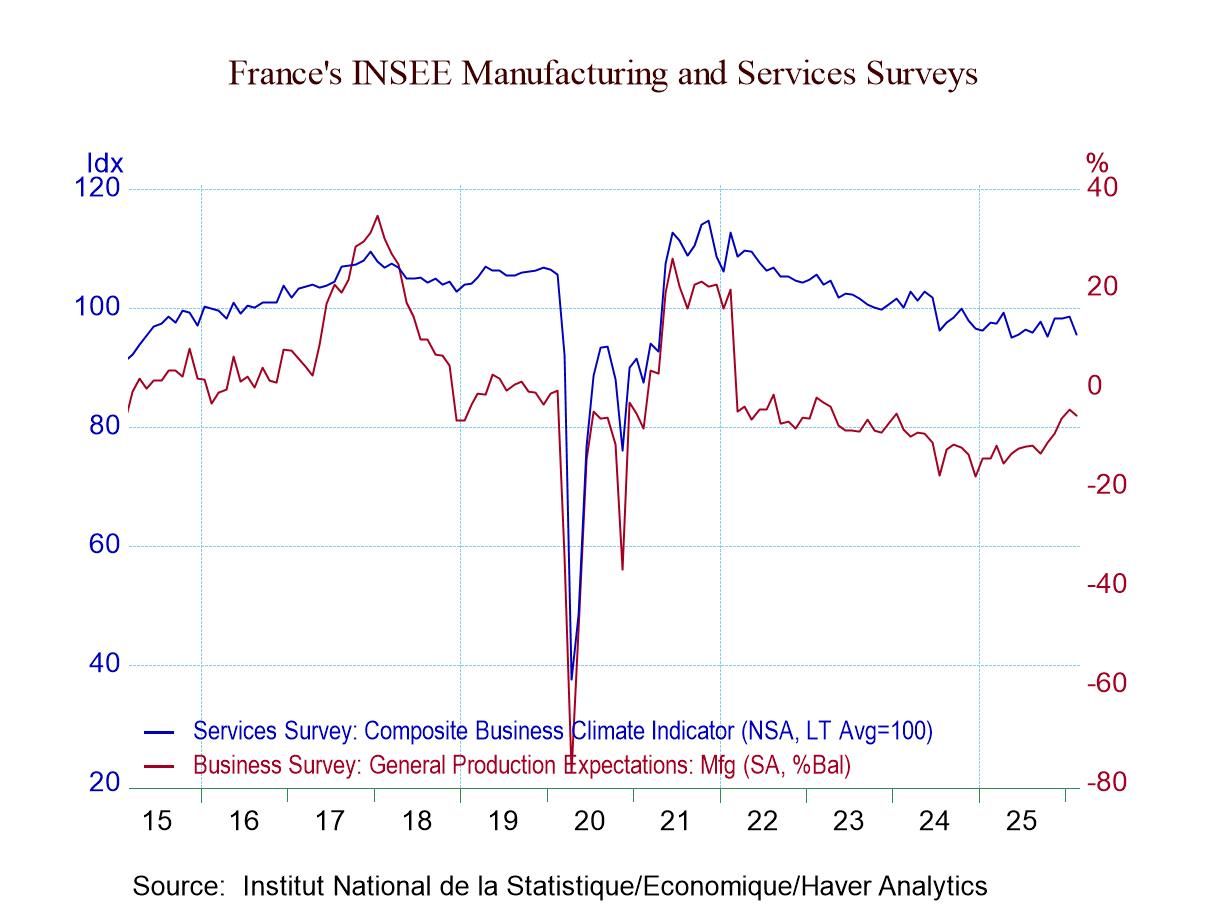

French Manufacturing and Services Surveys: Two Sectors, Two Different Trends, and Lingering Weakness

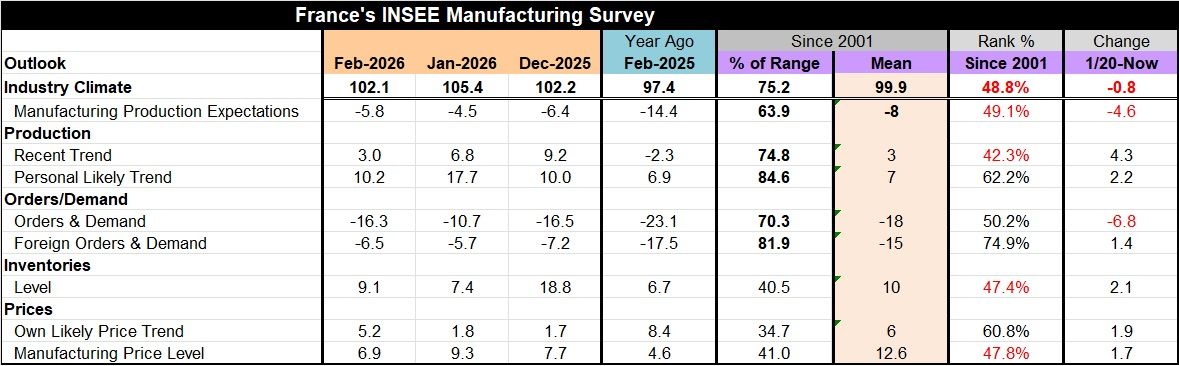

Neither the service sector nor the manufacturing survey value is particularly strong. The services climate headline has a 25-percentile standing; it has been higher about 75% of the time. That is not a good result. For manufacturing and industry, the standing is just short of the 50% mark which leaves it quite close to its historic median. That is not strong, but it is not weak either; it’s a modest middle ground. But February’s reading gave up ground, falling to 102.1 from 105.4 in January, back essentially to its December 2025 level. Even so, the February value has not been exceeded persistently until we go back to August 2022—three and one-half years ago.

The rebound in manufacturing is nascent; we can question its sustainability. And it is also only a modest step up after February’s erosion. Orders and demand flared higher in January and backed down in February. Orders and demand have a 50-percentile standing, with foreign orders much stronger at a 75-percentile standing. While production has a sub-median, 42-percentile standing, responses, when aggregated, show an ‘own-personal’ response standing at 62.2%. Maybe there is more granular, industry-level confidence that is being restrained by macroeconomic pessimism. This two-tier response is recreated compatibly for prices where firms see high own price trends stronger than their whole-economy trend. The own-price trends are elevated with a ranking over their 60th percentile while the macro price expectation is at a 48-percentiel standing. Production expectations are a classical representation of this month’s survey, falling back this month after some improvement last month and sporting a 49.1 percentile standing – a near median result. The manufacturing survey does not suggest any trouble; it exhibits near normal behavior, with orders at a midstream level/ranking.

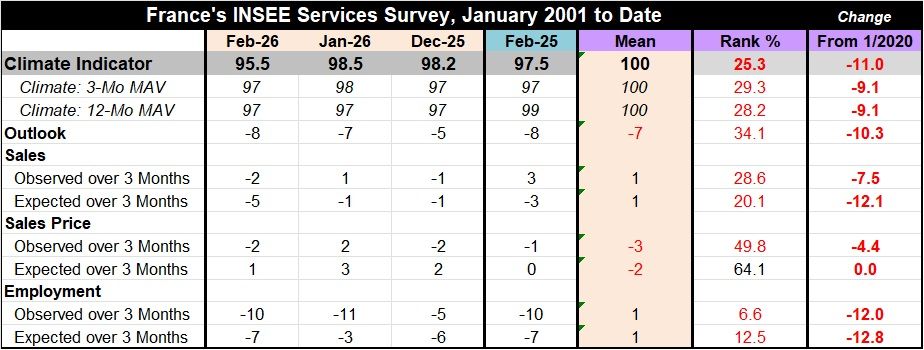

The services survey also backs off in February, but its ranking is weak, at the 25-percentile level. The 3-month and 12-month averages, when ranked, are ‘similarly’ weak—a clear sign that this services weakness is a real phenomenon. Only one-entry among the ten in the table has a ranked percentile standing over the 50-percent mark—that is the sales-price expected over the next three months. And that is not particularly reassuring. Employment trends, as observed and expected, rank in their 6th to 12th percentiles. Observed and expected sales trends are very low-ranking, and they weaken in February. The formal outlook is a lower one-third phenomenon, and it has been weakening.

France’s trends play out on the chart. There are issues revealed here that are only made clear by looking at the chart and the ranking, and tying-in those trends with what was reported this month. The broadest view of the manufacturing & services sectors is upsetting. The medium-term view is more constructive, but only because of the industrial rebound. Yet, looked at up close, that rebound is too nascent to trust. The short term remains expensive for industry, but unreliably so. The French economy has been struggling for a while, and France has severe budget problems that are also creating political issues. French policy is under pressure, and remember that, as an EMU member, there is no central bank to dedicate policy to resolving its issues. EMU-wide inflation is more or less under control, but rate cutting stimulus is unlikely.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global