Personal Income, Consumption, and Prices: Higher Prices Dampen Real Gains

Summary

- The energy component contributed to a high-side reading on the price index for personal consumption expenditures; the core component was firm as well.

- Consumer spending showed signs of slowing.

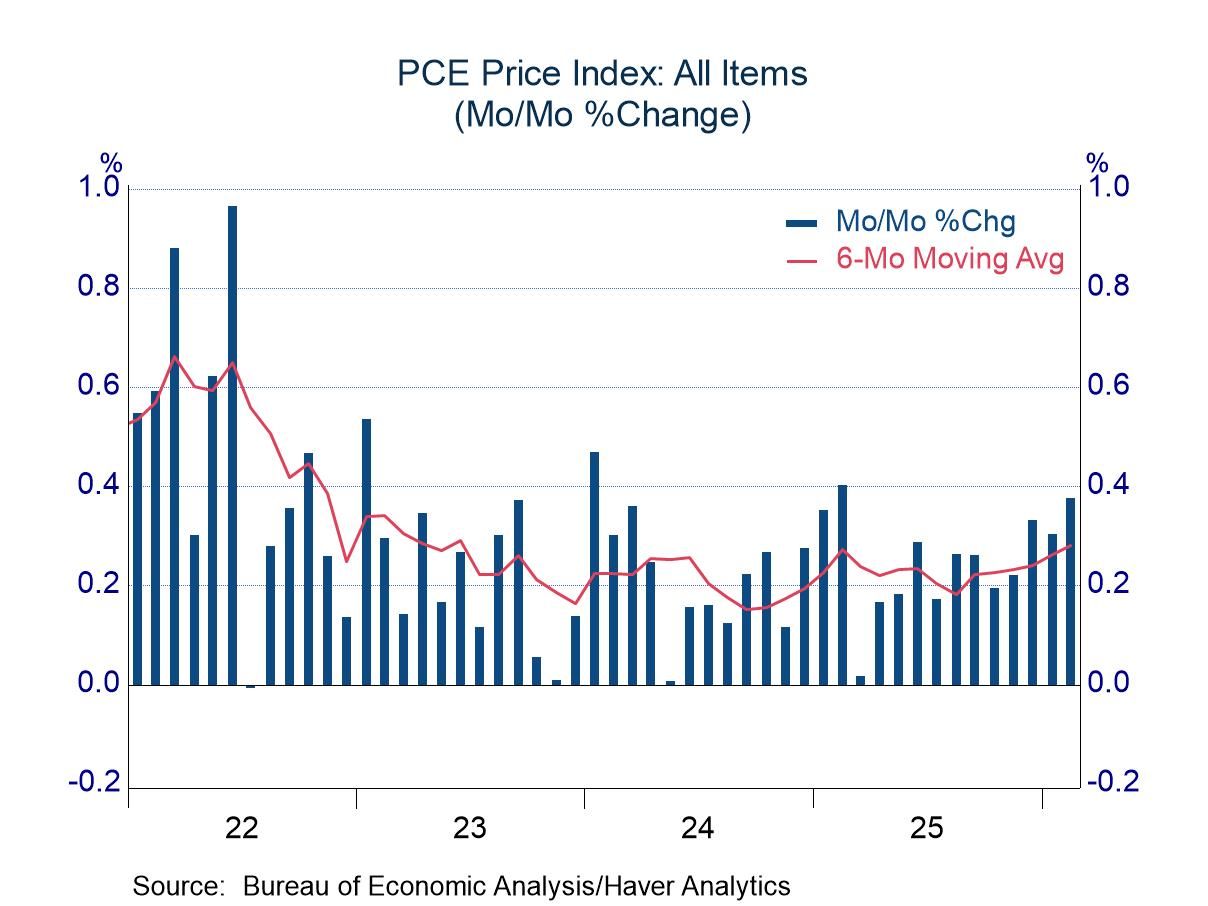

This monthly report is always packed with information relating to the household sector. At this time, most observers will probably be most interested in price developments, and the results for February were a bit unsettling. The headline price index rose 0.4%, influenced by a jump of 0.8% in energy prices. This increase was largely anticipated and not especially troubling when viewed in isolation. Energy prices have shown little net change in the past two years, and the latest reading of the index was comfortably within the recent range of observations. However, given developments in the Middle East, energy prices undoubtedly will surge out of that recent range in the months ahead.

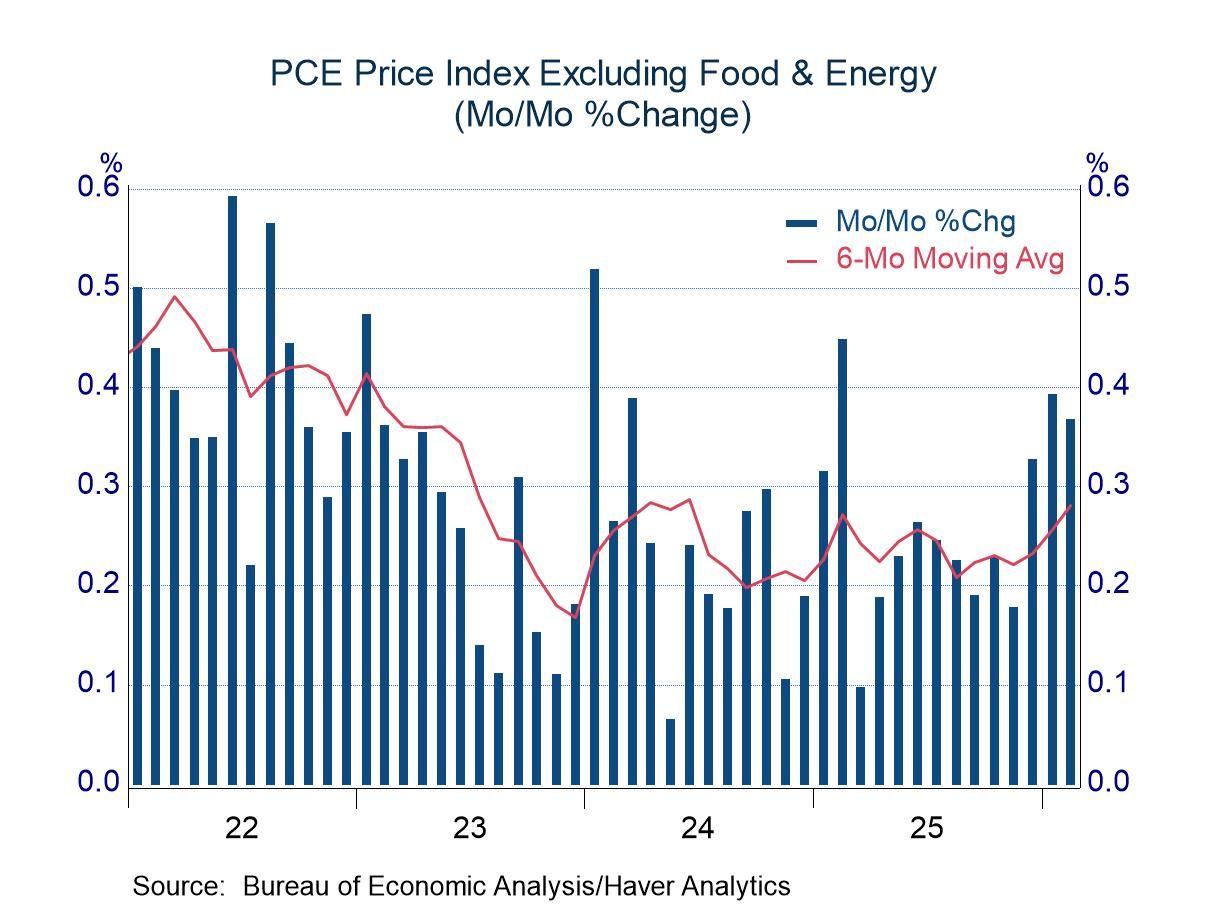

Core PCE prices also rose 0.4%, a touch firmer than the expected increase of 0.3%. An increase of 0.4% in core inflation is a quick pace even when viewed in Isolation, but this advance followed a similar increase in January, and the December reading almost rounded to 0.4%. These recent changes pulled the year-over-year increase in core prices to 3.0%, a full percentage point above the Federal Reserve’s target.

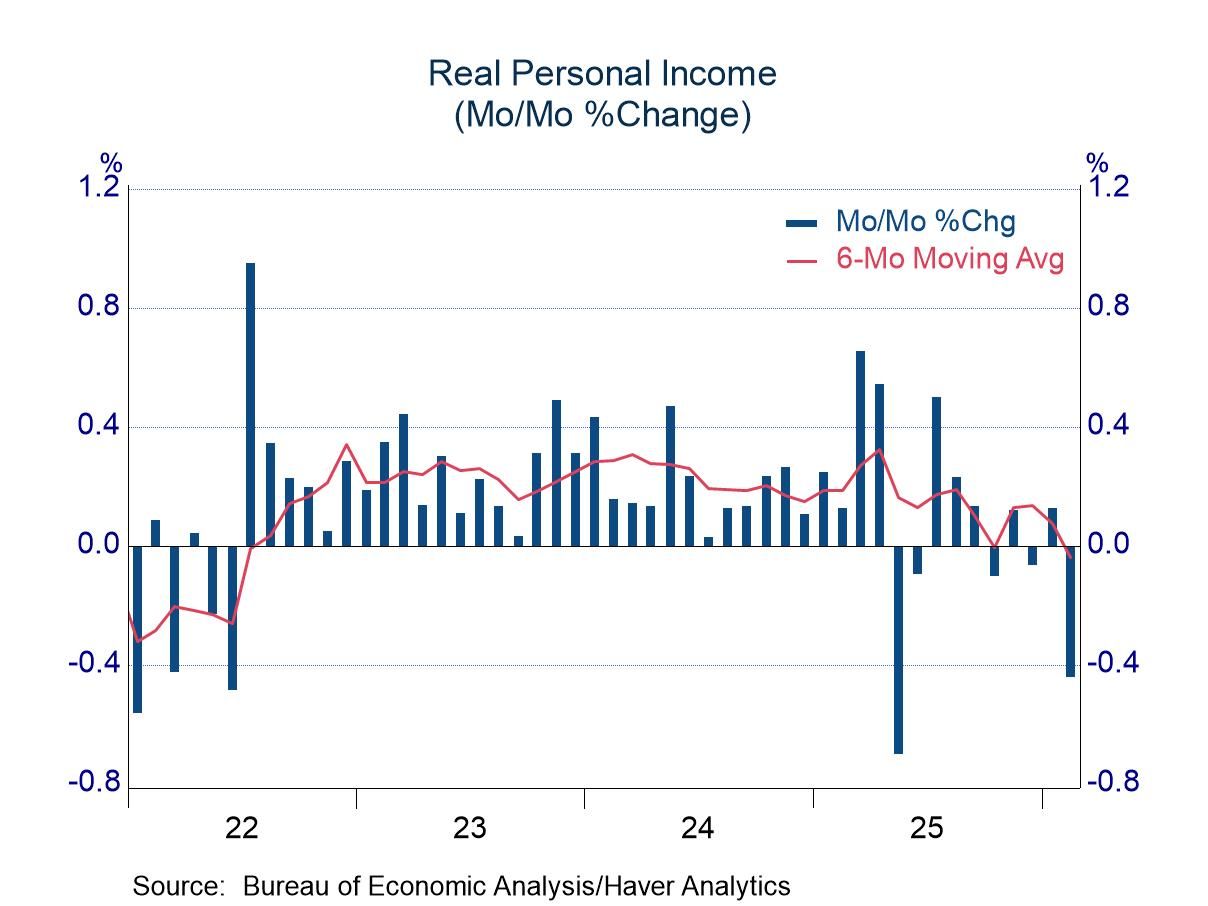

Nominal personal income dipped 0.1% in February, which translated to a decline of 0.4% after adjusting for inflation (almost rounding to -0.5%). The softness is striking, but a review of the detail suggests that special factors played a role. Much of the weakness reflected a decline of 1.7% in dividend income, which followed a jump of 1.9% in January. Dividend payments in the prior two years followed the same pattern, leaving one to suspect that seasonal adjustment has gone awry. Government transfer payments also declined, with the miscellaneous category accounting for most of the drop. Medicaid payments also fell, marking the fifth consecutive decline, most likely driven by the tightening of provisions included in the One Big Beautiful Bill Act.

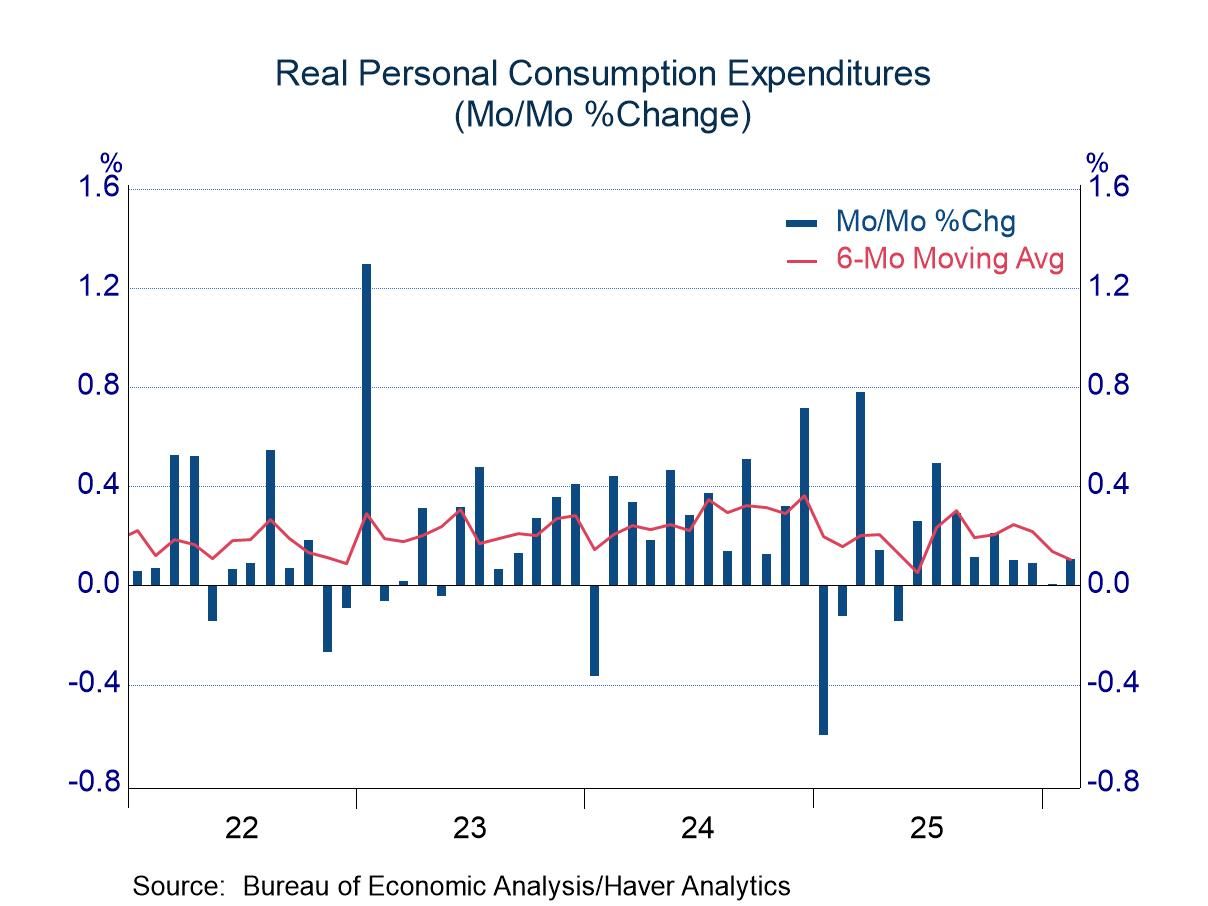

Nominal consumer expenditures rose 0.5%, a seemingly strong result, but the change amounted to only 0.1% in real terms. The small increase followed a flat reading in January and increases of only 0.1% in November and December. Consumers spent actively in the second and third quarters of last year, but they have become cautious recently. The data in hand suggest real outlay growth of approximately 1.0% in the first quarter, slower than the average pace of 3.0% in the middle of last year and 1.9% in 2025-Q4.

The personal income and consumption figures are available in Haver’s USECON database with detail in the USNA database. The Action Economics forecasts are in AS1REPNA.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global