Global| May 21 2026

Global| May 21 2026Charts of the Week: Surprise, Surprise

by:Andrew Cates

|in:Economy in Brief

Summary

Ongoing geopolitical tensions in the Middle East and the associated surge in energy prices have pushed inflation and bond market concerns back to the forefront of global financial markets. Investors are increasingly worried that central banks may now face even greater difficulty in bringing inflation fully under control, particularly in economies where underlying price pressures had already remained sticky prior to the latest energy shock. Recent upside surprises in US labour market and inflation data have already contributed to higher Treasury yields and a broader global backup in short-term government bond yields across the major economies (charts 1 and 2). Yet the picture is not entirely one-sided. Labour’s share of US national income remains historically weak, suggesting limited underlying wage bargaining power and helping explain why broader inflation persistence could ultimately remain contained (chart 3). Meanwhile, oil prices have remained elevated despite some moderation in broader geopolitical risk indicators, reflecting persistent supply-side disruption and ongoing stress surrounding key global energy and shipping routes (chart 4). Even so, recent core inflation data from economies including the UK, Canada and Austria suggest that pass-through from higher energy costs into broader underlying inflation has so far remained relatively limited (chart 5). At the same time, financial markets continue to be supported by an extraordinary AI-driven investment boom, with technology firms engaged in an unprecedented surge in spending on data centres, semiconductors and energy infrastructure (chart 6). Increasingly, the global economy appears caught between two powerful and competing forces: renewed supply-side inflation risks on one side and a historic wave of AI-driven technological investment on the other.

Inflation angst and renewed bond market jitters The recent rise in US Treasury yields has coincided with a renewed upswing in US economic surprises, particularly on the inflation and labour market fronts. As chart 1 illustrates below, our newly developed and combined Haver US Labour Market Surprise Index and Inflation Surprise Index (see methodological note at the end of this document) has moved back into positive territory, indicating that incoming data for labour market activity and inflation have, on balance, been coming in stronger than consensus expectations. This rebound has occurred against an increasingly fragile global backdrop marked by rising oil prices, shipping disruptions and renewed geopolitical tensions linked to the Middle East conflict. Markets are becoming increasingly concerned that higher energy costs could feed into broader inflation pressures at a time when underlying labour market momentum remains firmer than many expected.

Chart 1: Haver’s labour market and inflation surprise index versus US Treasury yields

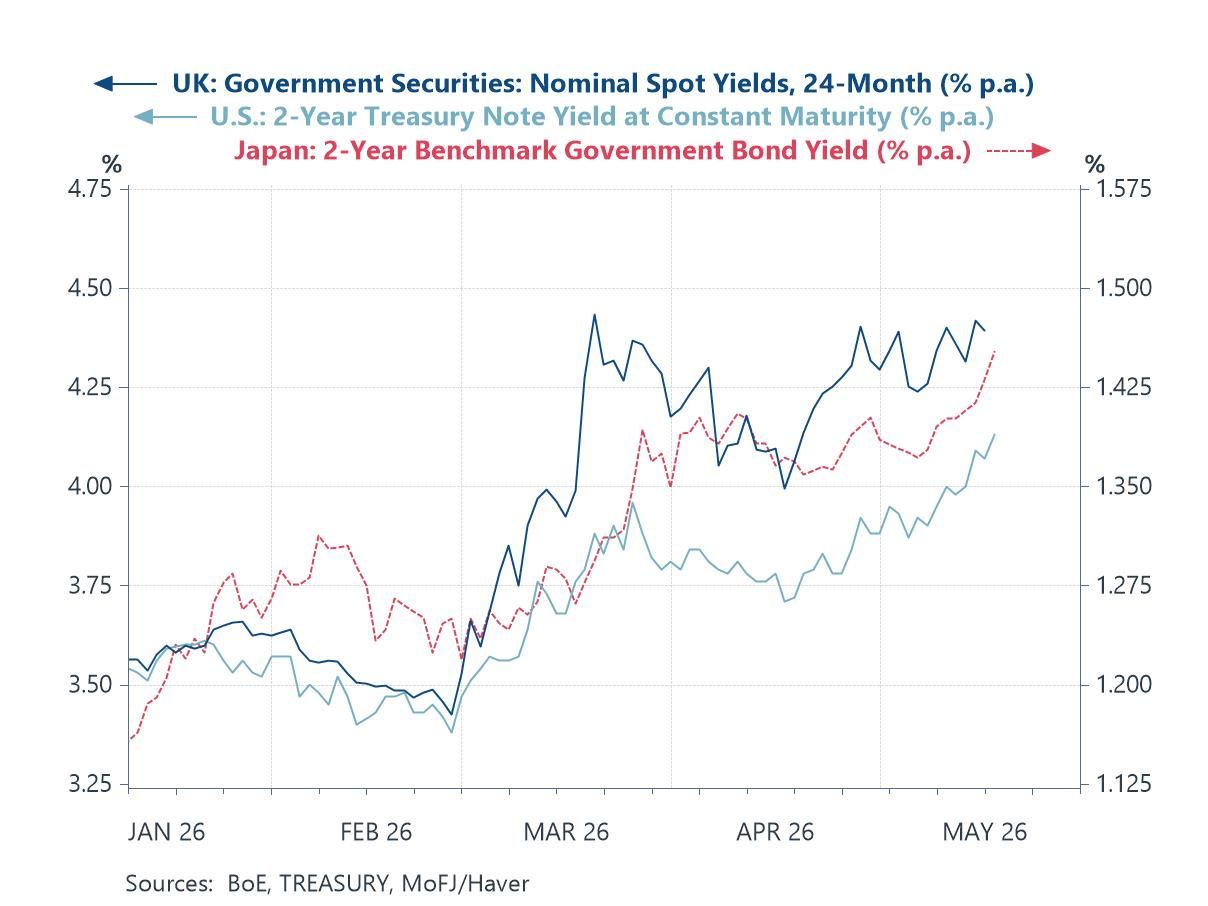

Central banks face renewed inflation concern A rise in short-term government bond yields has become increasingly broad-based across the major developed economies, with UK, US and Japanese two-year yields all trending higher in recent weeks. Investors are increasingly concerned that renewed geopolitical instability in the Middle East and higher energy prices could prolong global inflation pressures just as many central banks had been preparing for a gradual easing cycle. UK yields remain elevated amid persistent domestic inflation concerns, while Japanese yields have also continued to edge higher as markets reassess the outlook for Bank of Japan policy normalization in a world of rising imported energy costs. The synchronized move higher in front-end yields reflects growing unease that central banks may ultimately face a more difficult trade-off between supporting growth and containing another inflationary impulse.

Chart 2: Global 2-Year Bond Yields Continue to Climb

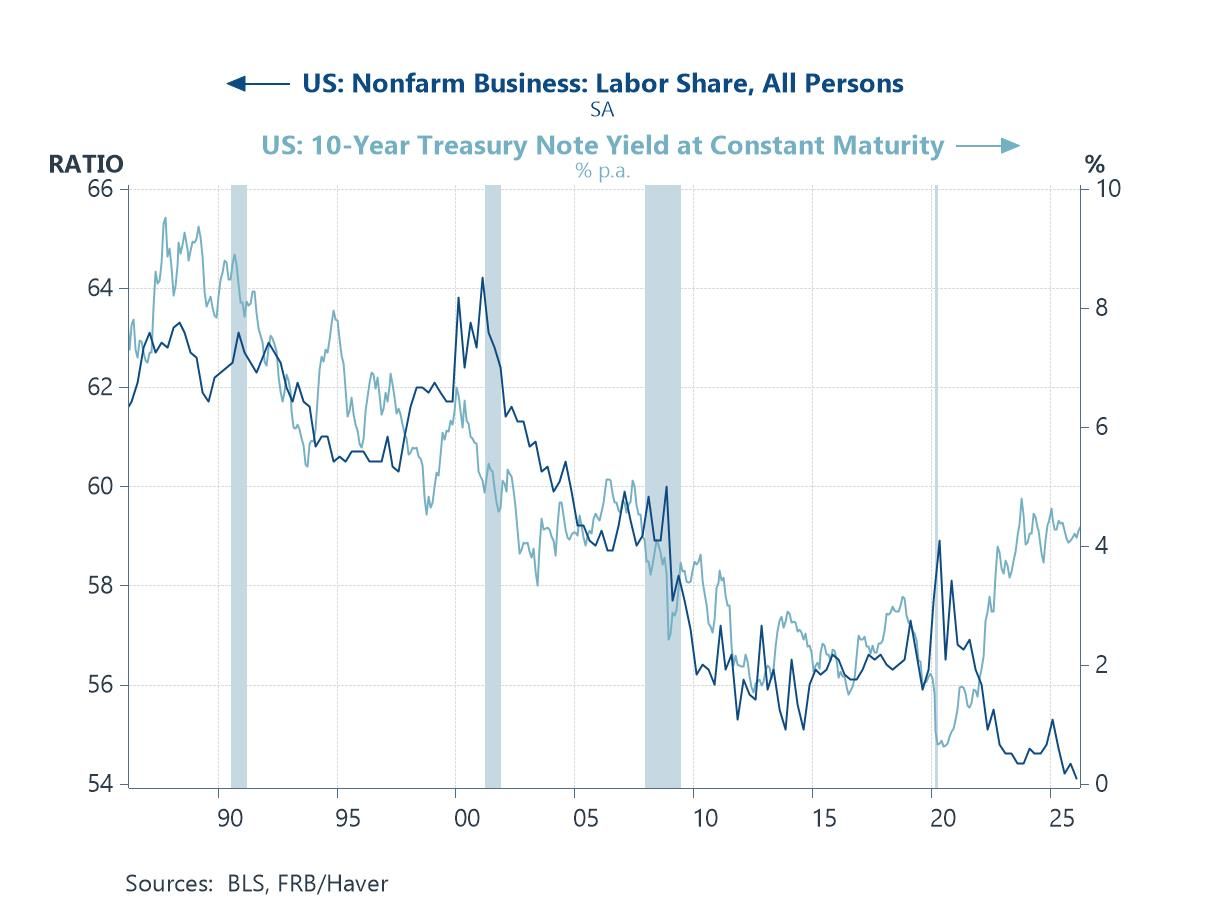

Weak labour bargaining power may limit inflation persistence Despite growing market anxiety about renewed inflation pressures, an important structural counterpoint comes from the continued weakness in labour’s share of US national income. As the next chart illustrates, labour’s share of nonfarm business income has declined to multi-decade lows. Historically, sustained inflation cycles have often been associated with stronger labour bargaining power, rising wage shares and the emergence of wage-price dynamics. Today, however, workers appear to retain relatively limited pricing power within the broader economy, particularly compared with earlier inflationary eras such as the 1970s. This may help explain why longer-term inflation expectations have, so far, remained relatively contained despite higher energy prices and geopolitical instability.

At the same time as this, the prolonged decline in labour’s share of income may also help explain the broader rise of populist politics across many advanced economies. Weak wage growth relative to profits, rising inequality and a growing perception that the gains from globalization and asset appreciation have been unevenly distributed have contributed to mounting political dissatisfaction.

Chart 3: US Labour’s Share of Income Has Declined To Historic Lows

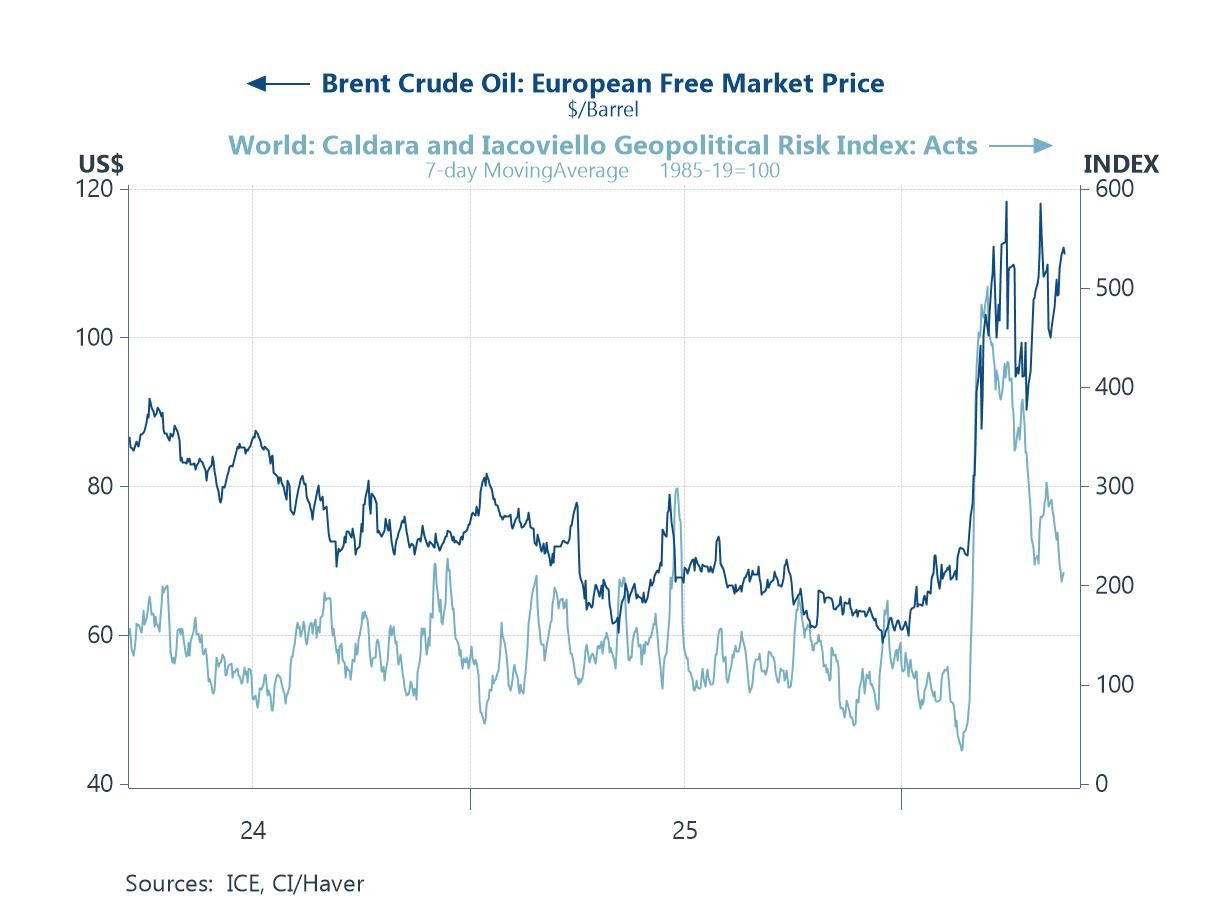

Energy markets remain under strain Yet the principal counterargument to the more benign inflation outlook suggested by weak labour bargaining power lies on the supply side — most notably in energy markets. As the chart shows, oil prices have remained elevated even as broader measures of geopolitical risk have started to retreat from their recent extremes. The Caldara-Iacoviello Geopolitical Risk Index suggests that fears of a major regional escalation in the Middle East have eased somewhat. However, Brent crude prices continue to reflect persistent disruption to energy flows and shipping routes, particularly given the ongoing effective closure and disruption surrounding the Strait of Hormuz. This divergence matters because financial markets and central banks are increasingly confronting the possibility that supply-side inflation pressures may persist even without a further escalation in military conflict. In other words, fading war fears do not necessarily imply a normalization in energy markets. Instead, the global economy may be entering a more prolonged period of structurally higher energy and transport costs, adding to inflation pressures even as underlying demand conditions soften. The result is an increasingly uncomfortable backdrop for policymakers, combining weaker growth momentum with renewed upside risks to inflation and interest rates.

Chart 4: Oil Prices Remain Elevated Despite Easing Geopolitical Risk Indicators

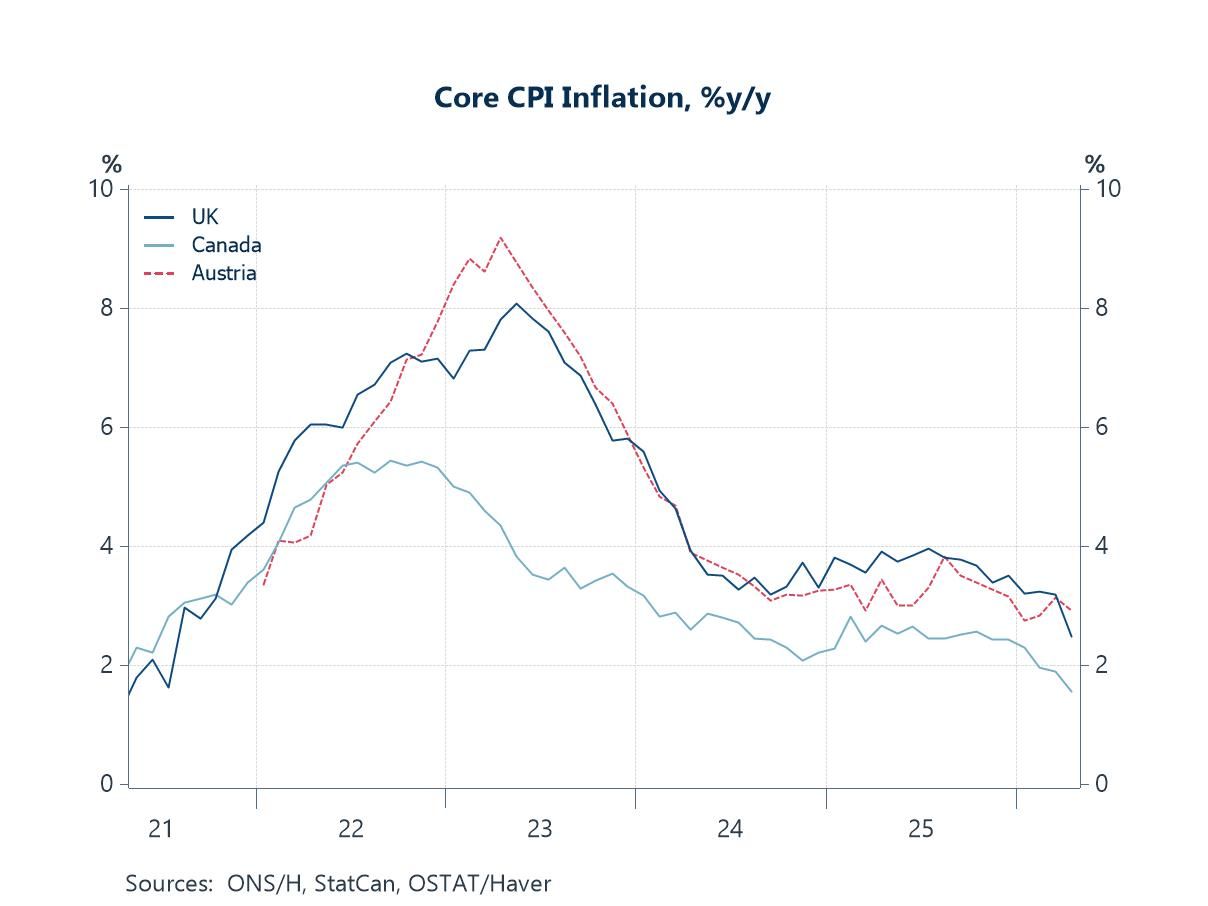

Benign Core CPI Inflation For Now Ultimately, what will matter most for central banks is not simply higher oil prices themselves, but the extent to which those higher costs feed through into broader underlying inflation. On that front, the recent inflation data from several advanced economies have, so far, remained remarkably benign. As the chart illustrates, core inflation measures pubished this week in the UK, Canada and Austria have all continued to moderate despite renewed geopolitical tensions and rising energy prices. This suggests that the broader inflationary impulse across goods, services and wages remains contained for now.

Chart 5: Core CPI Inflation has continued to moderate in the UK, Canada and Austria

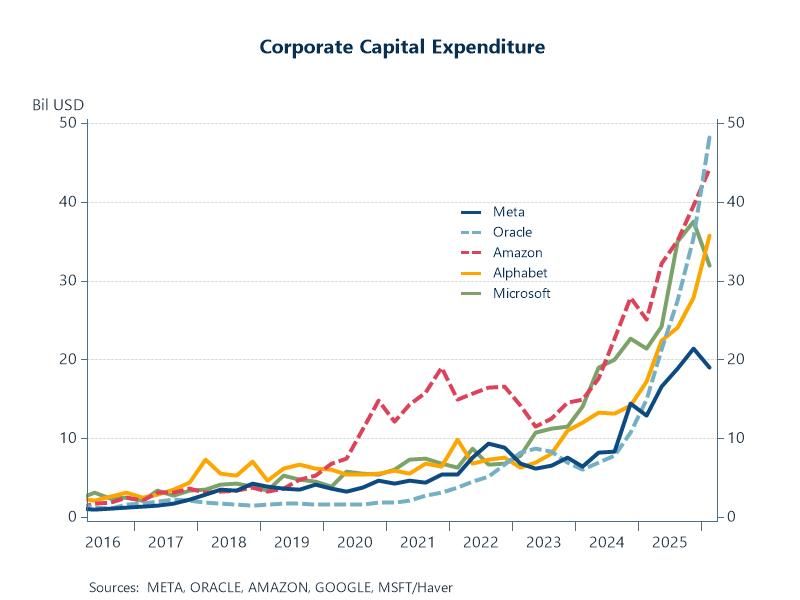

The AI Investment Boom Yet even as markets grapple with inflation risks, energy shocks and slowing global demand, financial markets continue to be dominated by one extraordinarily powerful countervailing force: the AI investment boom. As the chart illustrates, capital expenditure among the major technology firms — including Meta, Oracle, Amazon, Alphabet and Microsoft — has exploded higher over the past several years as the race to build generative AI infrastructure intensifies. Collectively, these firms have spent almost $1.5 trillion on capital expenditure since early 2021, with spending in Q1 2026 alone reaching an extraordinary $179 billion, nearly double the level of a year earlier.

Chart 6: The AI Investment Boom Continues to Reshape the Global Economy

Andrew Cates

AuthorMore in Author Profile »Andy Cates joined Haver Analytics as a Senior Economist in 2020. Andy has more than 25 years of experience forecasting the global economic outlook and in assessing the implications for policy settings and financial markets. He has held various senior positions in London in a number of Investment Banks including as Head of Developed Markets Economics at Nomura and as Chief Eurozone Economist at RBS. These followed a spell of 21 years as Senior International Economist at UBS, 5 of which were spent in Singapore. Prior to his time in financial services Andy was a UK economist at HM Treasury in London holding positions in the domestic forecasting and macroeconomic modelling units. He has a BA in Economics from the University of York and an MSc in Economics and Econometrics from the University of Southampton.

More Economy in Brief