Housing Starts: Hints of Improvement

Summary

- March & April brought the best two-month performance since late 2023.

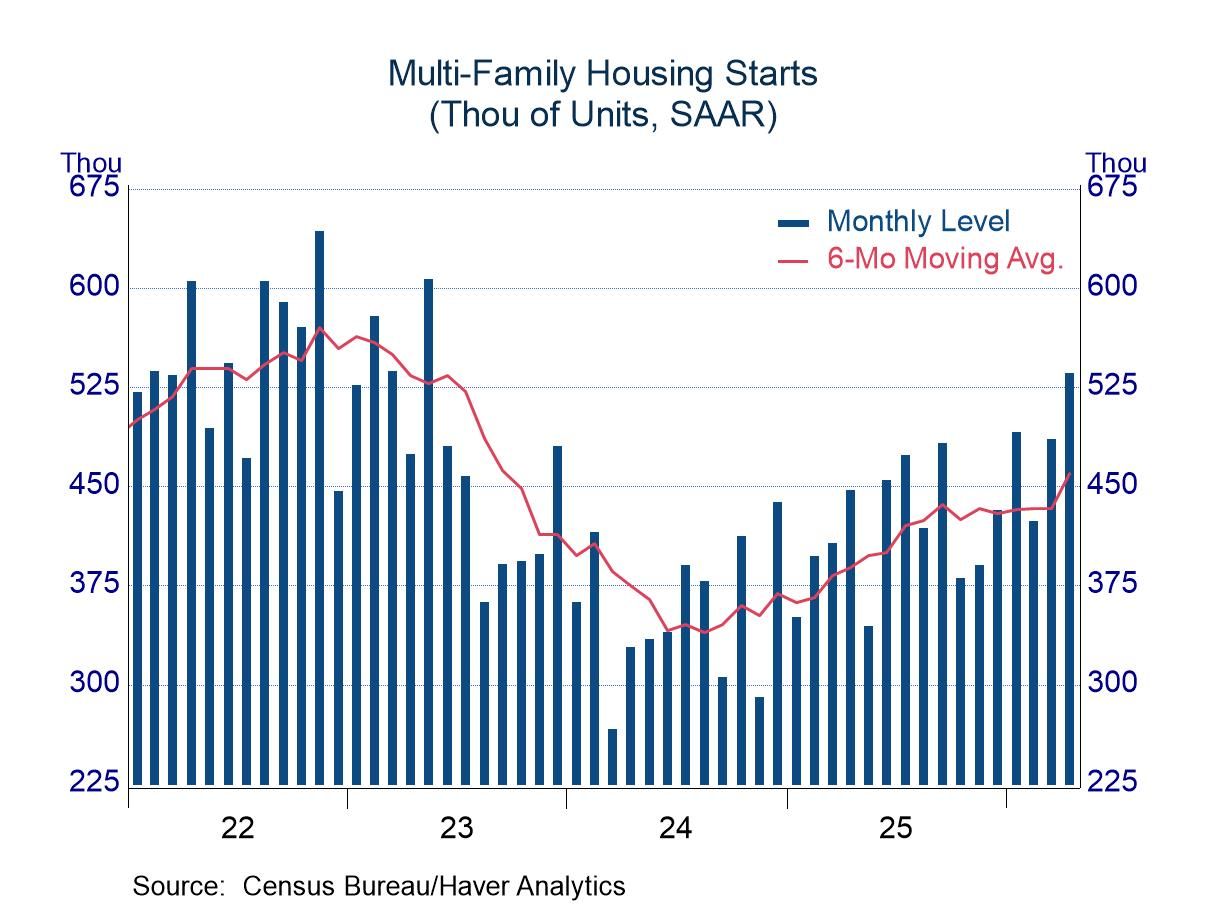

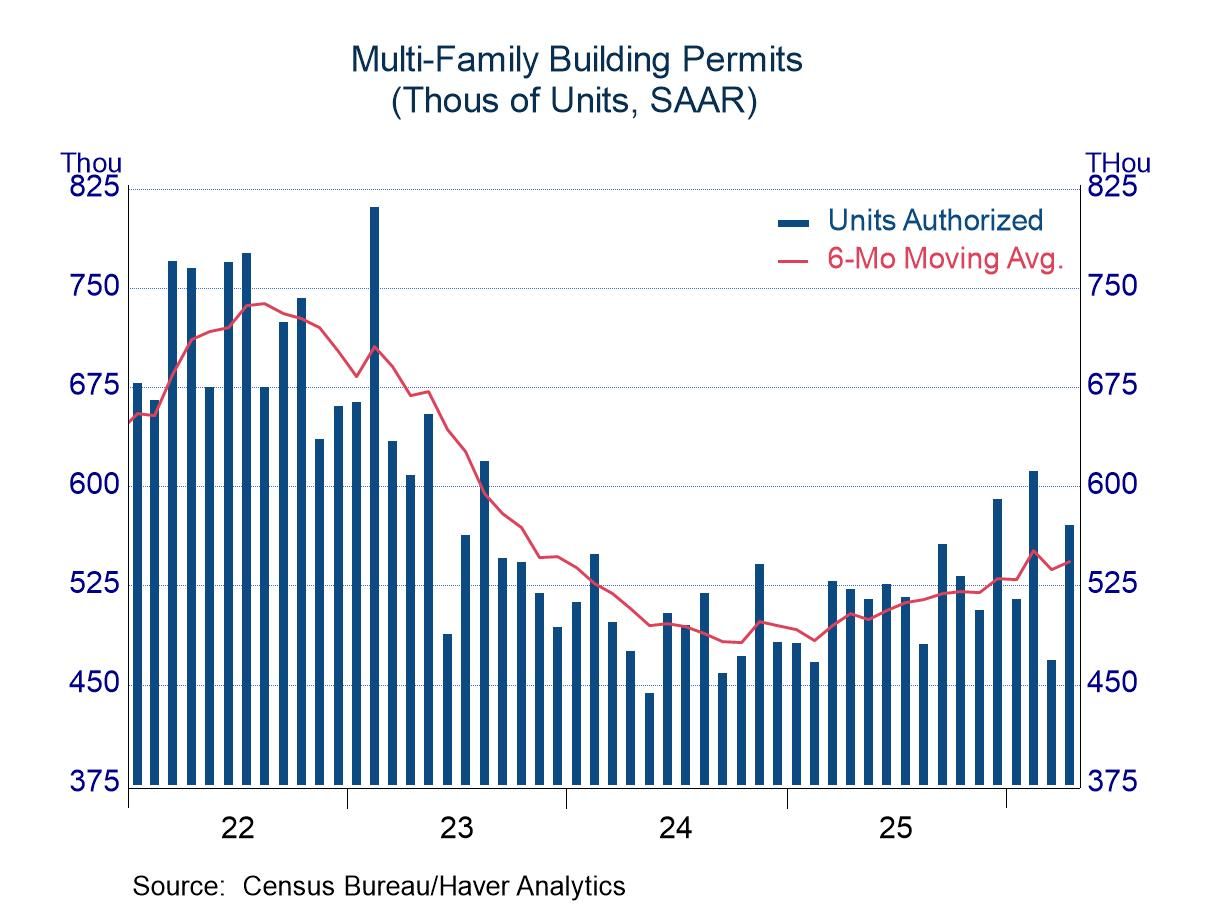

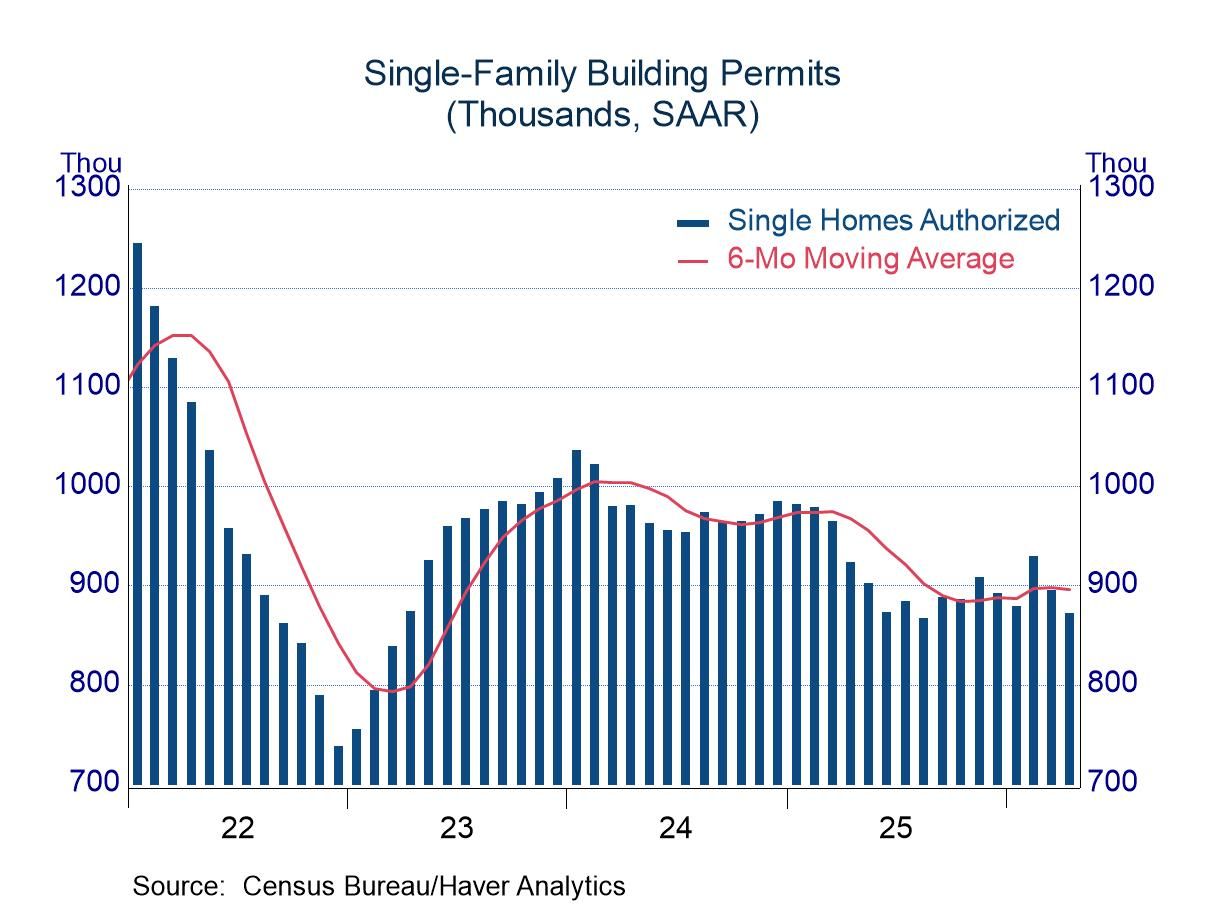

- Multi-family activity has led the advance; single-family activity lags.

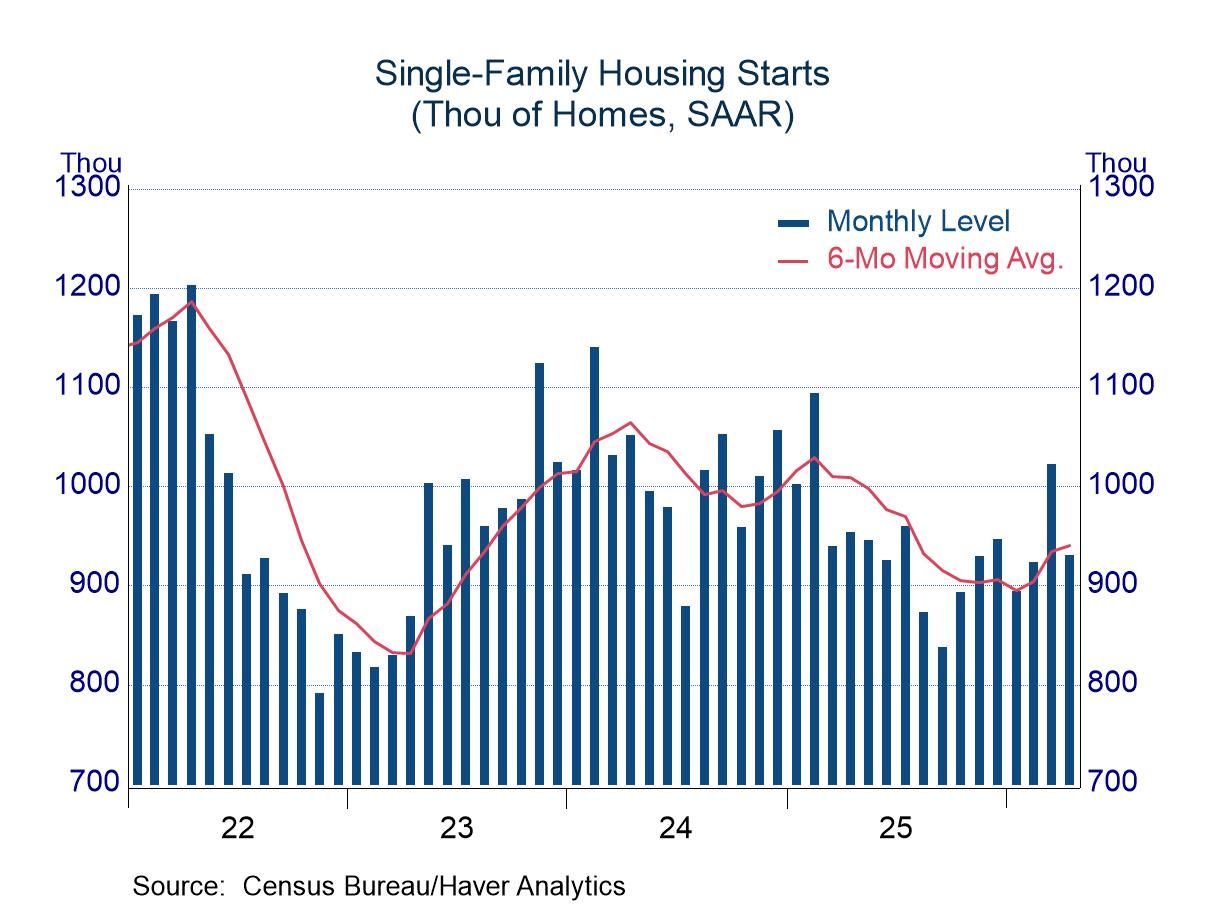

Housing starts fell 2.8% in April, but the drop followed a jump of 12% in March that had pushed activity to one of the firmest levels of the past few years. Even with the decline in April, starts remained in the upper end of the recent range. In fact, March and April combined brought the best two-month performance since late 2023.

The housing sector has been generally soft in the past few years. Activity was strong in late 2020 and 2021 as the economy recovered from the pandemic and as low interest rates boosted affordability. However, the market cooled in 2022 as the Fed tightened monetary policy, and home construction has been lethargic since then. The contribution of residential construction to GDP growth has been negative in seven of the past eight quarters (subtracting 0.1 percentage point on average). The improvement in multi-family activity offers the prospect of a positive contribution in the quarters ahead, but it would probably not be a large one. Single-family activity has a heavier weight in residential construction, and recent results have not been firm enough to suggest meaningful gains.

Multi-family construction led the advance in the past two months, increasing 14.7% in March and 10.3% in April. The trend in multi-family starts had been moving sideways for a time (note the 6-month average in the left chart), but recent gains have quickened the pace, perhaps renewing the upward drift that began in 2024. Single-family construction stirred in March (up 10.7 percent), but it gave back much of the advance with a decline of 9.0% in April. Still, the six-month average of single family starts is tilting upward, although only mildly so.

The slight pick up in single-family starts is encouraging, but recent movement in building permits suggests caution. Single-family permits fell in both March and April, offsetting a hint of improvement in February and leaving little change in the six-month average (chart, lower right). Multi-family permits have moved erratically in recent months, but they are drifting higher on average.

The housing starts and permits figures can be found in Haver’s USECON database. The expectations figure is contained in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief