French Industry and Services Confidence Diverge in June

In June, there's a slight divergence in the performance of industry climate and service sector climate, although broadly the two sectors have seen their composite indexes moving in more or less the same direction. Since 2024, the industry survey has moved up slightly after falling faster than the services gauge. The services survey has been locked in a slow trend of deterioration, largely since it reached a peak in 2021 in the wake of COVID.

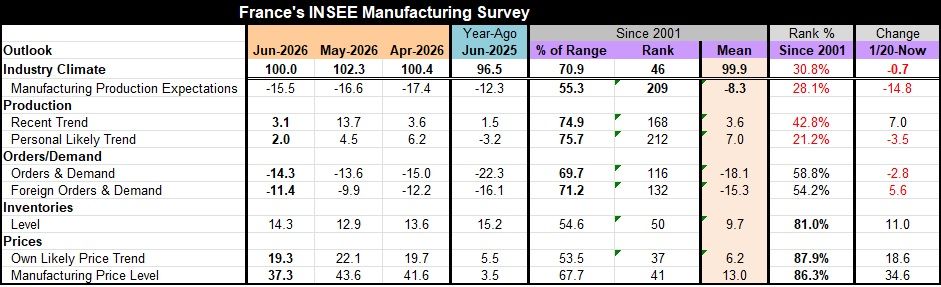

The industry climate gauge has a 30.8 percentile standing, but the recent production trend, while declining, logs a more substantial 42.8 percentile standing. Contributing survey members find their own industry ‘likely trend’ much weaker, at a 21.2 percentile standing. Demand overall, however, has standings above the 50th percentile, putting overall and foreign orders & demand each above their respective medians for this period of ranking back to 2001. Inventories have a strong 81-percentile ranking. Prices are extremely strong, with 87-percentile and 86-percentile standings for respondents for their personal industry trend for prices as well as for the overarching manufacturing sector estimate of prices. Higher prices seem to be the one thing that everyone can agree on by a large margin.

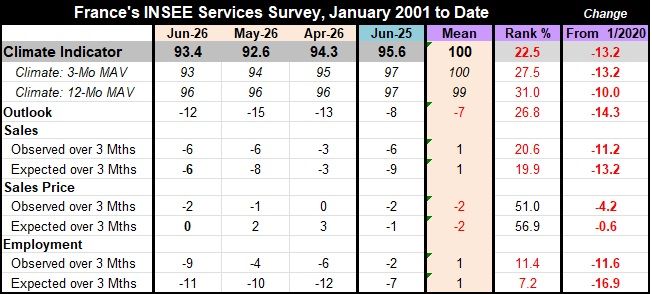

As for services, the service climate index improved slightly to 93.4 in June from 92.6 in May. The three-month moving average was weaker in June than in May as well; the 12-month moving average has been stuck at its current level for a number of months. The outlook in June improved slightly to a reading of -12 from -15 in May, but the outlook ranking is still a weak 26.8 percentile standing. The three-month expectations and observations of past sales trends haven't changed much in the last two months, but there has been a slight improvement for sales expectations. However, both sales metrics have low 20th percentile standings. Sales prices have deteriorated slightly in June compared to May for both the observed and the expected trends, but prices have standings above their 50th percentiles, logging above-median performance. Employment over the last three months has weakened noticeably, and expected employment is weaker by a small amount.

In terms of rankings, all of the sector rankings are below the 50th percentile on all of these observations, including the climate headline except for sales prices where both the past three-month observed trend and the expected trend have readings above their respective 50th percentiles, indicating past and expected price pressures in excess of normal.

Assessment On balance, the readings for the French industry, manufacturing sector and services are not encouraging. In addition, concerns about prices linger. The services sector, those concerns seem moderate compared to the concerns in manufacturing.

The hot war continues between Ukraine and Russia, while in the Middle East there was talk of some improvement and a potential peace deal between the United States and Iran, but every time there is some talk of a breakthrough, there appears to be a breakdown. In the most recent development, Iran has asserted its right to control traffic through the Strait of Hormuz, and it's not clear how that demand would ever be consistent with the U.S. allowing a ceasefire. It appears that Iran may have traded its irreconcilable demand for nuclear weapons for a more pragmatic and real-world argument—that it will control the traffic through the Strait of Hormuz simply because it can—and it still is doing exactly that, even after all the destruction it suffered.

Stopping Iran from controlling the Strait would take a commitment to restart the war. All this makes me personally more pessimistic. I think Iran sees the need for Trump to cut a deal and stop the war before the U.S. mid-term elections, and it is pressing that need to its advantage. Trading its nuclear ambitions for real world control of the Strait would elevate Iran’s power from being dangerous but ethereal to a real world event with constant consequences.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global