Global| Mar 09 2026

Global| Mar 09 2026Fiscal Divergence and Sovereign Risk in 2026

|in:Viewpoints

United States & Europe

In the United States—where the fiscal year begins in September—fiscal policy remains expansionary, with Trump’s One Big Beautiful Bill setting the overall policy direction.

The European Commission projects the euro-area fiscal deficit at around 3.3% of GDP in 2026 and insists the year will not be one of fiscal stimulus. Whether this proves accurate remains uncertain.

Within the euro area, Germany’s fiscal plans centre on a major investment push, including the €500bn infrastructure fund, alongside significantly higher defence spending. Germany’s Draft Budgetary Plan suggests the general government deficit could rise to around 4¾% of GDP, driven by spending on infrastructure, innovation, security and defence.

France has also adopted a 2026 budget that reflects political constraints as much as fiscal priorities. Defence spending is rising, but the consolidation path is slower than previously envisaged. As part of a compromise with the left, plans to raise the pension age from 62 to 64 and to cut production taxes have been abandoned.

Italy’s 2026 Budget Law includes measures worth roughly €22bn over 2026–28, though the deficit is still projected to narrow slightly to 5% of GDP in 2026, from about 5.4% in 2025.

Spain, by contrast, faces less need for fiscal support and remains focused on consolidation as pandemic-era emergency measures expire.

Taken together, fiscal policy across the euro area remains broadly restrained, though increasingly shaped by defence priorities. Even so, these developments appear modest when set against fiscal policy elsewhere—particularly Japan.

Japan’s Expansionary Turn

Japan’s government approved a US$135bn fiscal stimulus package in late 2025, the largest in years, aimed at supporting households and economic growth. Around US$118bn comes through general-account spending, with the remainder delivered through tax measures and related initiatives.

The programme focuses heavily on household relief and strategic investment. Measures include utility and gasoline tax relief, subsidies and transfers to support consumption, and expanded investment in infrastructure, AI, semiconductors and other strategic sectors. Support for local governments and small and medium-sized enterprises has also been increased.

The government is also considering a two-year suspension of the 8% consumption tax on food and drinks, though the proposal remains under debate.

Asia: A Measured Fiscal Approach

Compared with advanced economies, Asia’s fiscal position remains relatively strong, reflecting both smaller pandemic stimulus programmes and a longstanding preference for fiscal restraint.

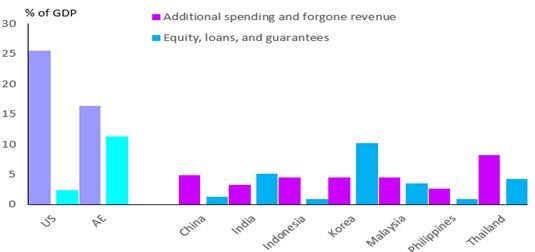

During the Covid-19 crisis, fiscal support in advanced economies averaged about 28% of GDP, while Asian economies averaged only 8.4% (Figure 1).

Figure 1: Covid-19 fiscal stimulus response

Source: IMF & Westbourne Research

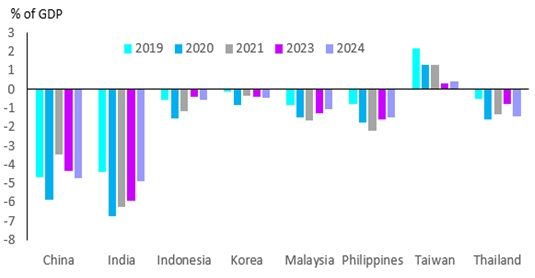

By 2024—apart from China and India—budget deficits across the region were considerably smaller than in the United States or the euro area. Deficits were under 1% of GDP in Indonesia and Korea, and around 1.5% in the Philippines, Thailand and Malaysia, while Taiwan has maintained a fiscal surplus since at least 2019 (Figure 2).

Figure 2: Asia budget balances 2019-24

Source: Haver Analytics & Westbourne Research

Fiscal Policy in Asia for 2026

China’s fiscal policy continues to expand as the government attempts to revive domestic demand, promote next-generation industries and stabilise the economy. The authorities plan to issue 1.3 trillion yuan in ultra-long special bonds in 2026, while maintaining the budget deficit at around 4% of GDP.

Of these bonds, 250 billion yuan will be allocated to support consumer goods trade-in programmes, compared with 300 billion yuan last year. The Government Work Report also proposes issuing 800 billion yuan in new policy-based financial instruments, exceeding the 500 billion yuan launched in 2025 and coming in above market expectations.

Funds are expected to flow to sectors similar to those targeted previously, including the digital economy, artificial intelligence, the low-altitude economy, green technologies and consumption-related infrastructure.

Elsewhere in Asia, fiscal policy remains supportive but measured.

In India fiscal consolidation continues +: the budget deficit is forecast to fall from 4.4% of GDP in FY25/26 to 4.3% in FY26/27 and public debt from 56.1% of GDP to 55.6%. The focus remains firmly on capital expenditure rather than consumption. Public investment – driven by spending on railways, transport, freight logistics, waterways, and connectivity nodes - is set to rise a record US$133bn.

Korea is pursuing a moderately expansionary stance. Its 2026 Economic Growth Strategy increases government spending by about 8.1% relative to 2025 and includes roughly US$15bn in public-institution investment and policy financing, alongside measures aimed at stabilising prices, easing household cost pressures and supporting the property market.

Taiwan’s FY2026 budget prioritises national security, with defence spending rising roughly 20% year-on-year, alongside modest allocations for social welfare and industrial development.

Thailand will continue running a deficit in 2026, though spending increases only modestly. Fiscal support is focused primarily on tourism and household consumption, including tax relief and incentives to boost domestic travel.

Indonesia stands out for maintaining fiscal discipline despite President Prabowo’s populist agenda. A stimulus package of about US$989m introduced in late 2025 included tax relief, infrastructure “cash-for-work” programmes and loan support. The 2026 budget keeps the deficit near the legal cap of 2.5–2.7% of GDP, supported by relatively strong tax revenues.

By contrast the Philippines has approved its largest budget ever, rising 7.4% year-on-year in FY2026. Despite this expansion, the deficit is expected to narrow slightly to 5.3% of GDP thanks to improved tax collection.

Overall, fiscal policy across Asia in 2026 remains supportive but targeted, with countries prioritising tourism, defence, social programmes and public investment rather than broad-based stimulus.

Public Debt Trends

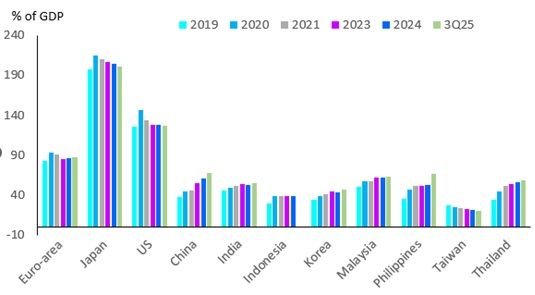

As governments continue to run post-pandemic deficits, public debt has risen across most economies (Figure 3). Exceptions include Taiwan—thanks to persistent fiscal surpluses—and, until recently, Japan. Even so, public debt ratios across Asia remain significantly lower than those in the US, Europe and Japan, suggesting limited risk that government borrowing will crowd out private investment.

Figure 3: Public debt trends

Source: Haver Analytics & Westbourne Research

Fiscal Sustainability and Vulnerability

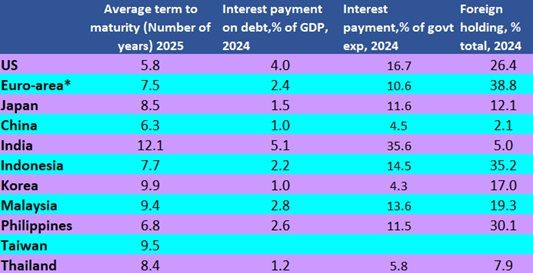

Fiscal sustainability depends on several factors, including debt maturity, servicing costs and reliance on foreign investors.

Three observations stand out.

First, Asian government debt generally has longer maturities than US Treasuries. India’s average maturity is about 12 years, while China’s is around 6.3 years. Europe and Japan also compare favourably with the United States on this metric.

Second, debt-servicing costs remain manageable across most countries. Even in the United States—where they are highest—interest payments amount to roughly 4% of GDP.

Third, vulnerability to shifts in investor sentiment varies widely. The euro area, with the highest foreign ownership of government debt, is the most exposed to market pressure. This partly explains Europe’s increasing reliance on EU-level borrowing and off-balance-sheet financing.

Indonesia ranks second on this vulnerability measure, followed by the Philippines.

Despite recent volatility in Japanese government bond markets, the risk of a fiscal crisis in Japan remains lower than in the euro area. Strong domestic investor demand and low foreign ownership provide a stabilising anchor. These same factors also support a relatively stable outlook for India, where fiscal consolidation continues.

Investment Implications

Combining these indicators provides a framework for assessing fiscal resilience. Countries were ranked across six metrics, including budget balances, debt ratios, debt maturity, servicing costs and foreign ownership (Figure 4).

Higher rankings indicate weaker fiscal performance.

On this basis, the United States recorded the weakest deficit position, while Japan ranked strongest at the time of measurement. Aggregating the indicators produces an overall resilience score.

The results suggest investors should underweight government bonds from the United States, the euro area and the Philippines, while overweighting Korean, Thai and Chinese bonds. Taiwan would likely rank highly if full data were available.

Figure 4: Maturity, debt servicing and foreign ownership

Source: Haver Analytics & Westbourne Research *calculated based on the big four

Sharmila Whelan

AuthorMore in Author Profile »The founder of Westbourne Research (www.westbourne-research.com), Sharmila Whelan is a seasoned Global Geopolitical-Macro Strategist with nearly three decades of experience advising buy-side clients on multi-asset investment strategies and asset allocations. Her career has been defined by her differentiated thinking, a deep understanding of the intricate connections between global geopolitics, macro and policy dynamics, and the Austrian business cycle approach to economic analysis. She has counseled governmental bodies such as the CIA, the US State Department, the British High Commission, DFID, and China’s NDRC.

Sharmila has held prominent roles in both London and Hong Kong, serving as Managing Director at Aletheia Capital, Director at Merrill Lynch Bank of America, Senior Economist at CLSA, and Asia Regional Economist at BP Plc. In 2022, Bloomberg recognised her as one of the UK's "12 New Expert Voices." She is a frequent media commentator on Bloomberg TV and radio, BBC World Business News, and CNBC, and is a sought-after speaker at high-profile events such as the Financial Times Wealth Summit and CFA UK & India conferences. Sharmila also contributes opinion pieces to Financial Times Professional Wealth Management and the Economist Group’s EIU.