Export and Import Prices: Upward Pressure Points in January

Summary

- Nonpetroleum import prices break from a flat trend with jumps in both December and January.

- Export prices also accelerate, led by consumer goods and capital goods.

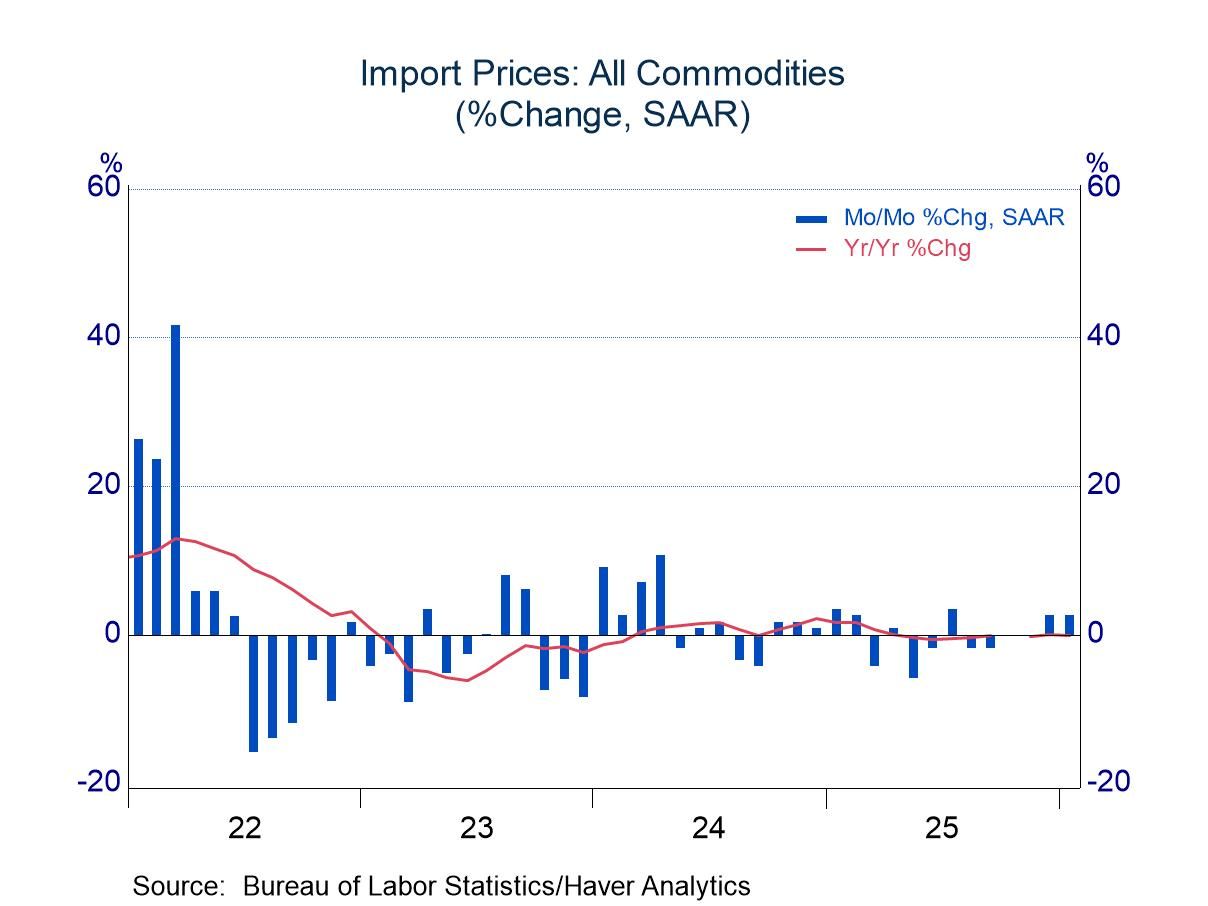

The headline figure for import prices rose 0.2% in January (annual rate of 2.6%), matching the change in December and continuing a pattern of generally subdued changes. The ups and downs of import prices in the past two years have left little net change, with the year-over-year rate at -0.1% in January.

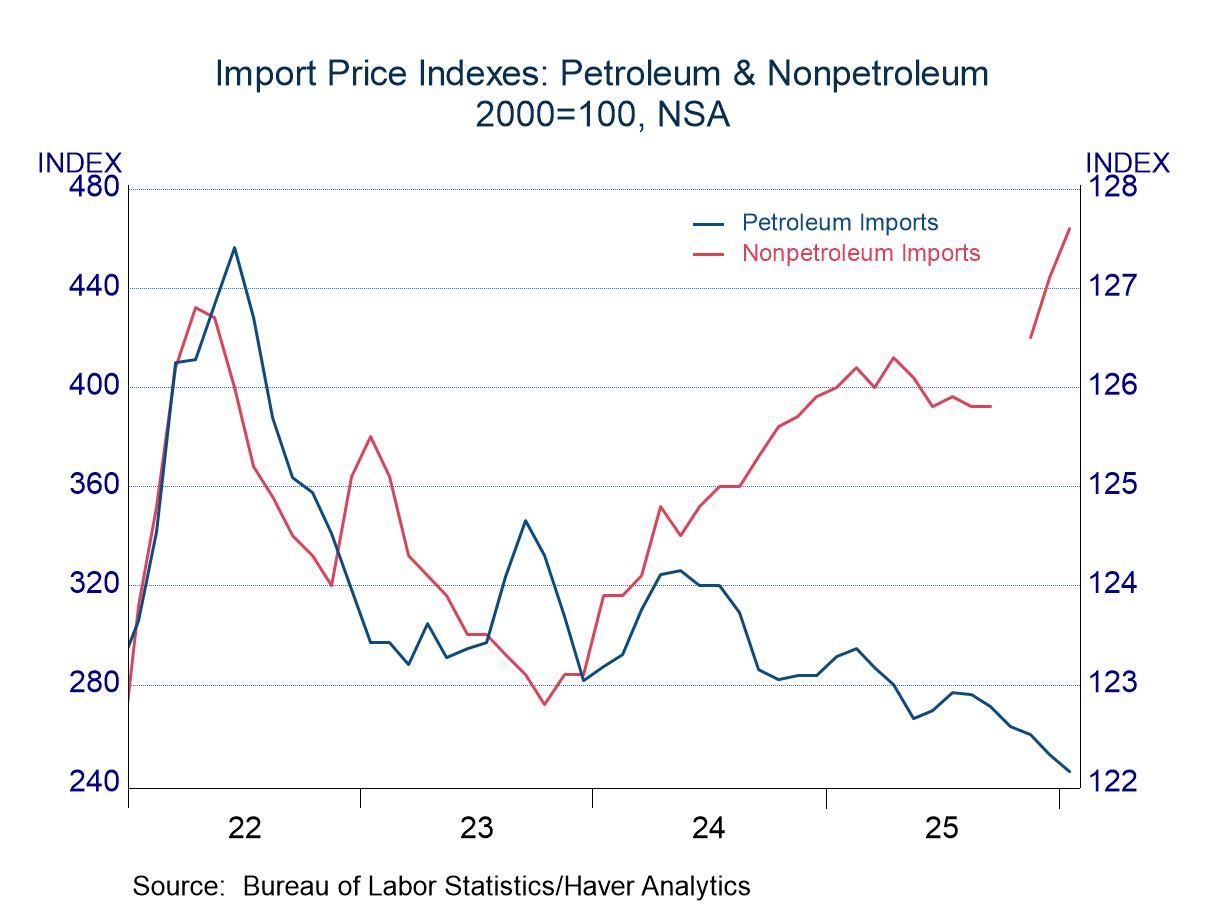

The flat trend, though, reflected distinctly different patterns in the prices of petroleum products and nonpetroleum goods. Petrol prices have traced an irregular downward path, with notable weakness recently: January marked the sixth consecutive decline. Prices of nonpetroleum products, in contrast, broke from a flat trend most of last year with surges in both December and January.

The distinctly different paths are evident in the chart above (right), which plots the levels of these price indexes rather than the percent changes. (Figures for nonpetroleum prices are not available for October because of the government shutdown.) The break in trend for nonpetroleum import prices is striking. One is tempted to argue that the surge reflects the effects of tariffs, but this is most likely not the case. The figures in this report are based on invoices before the imposition of tariffs, and thus there is no direct effect.

However, one might imagine an indirect effect. If foreign producers wished to absorb the tariff burden to remain competitive in the US market, they could reduce invoiced prices to keep post-tariff prices steady. Indeed, nonpetroleum prices fell in both May and June following the announcement of President Trump’s Liberation Day tariffs. The subsequent easing of the draconian tariffs announced in April might have led importers to return to original prices in recent months, which would now be picked up as higher prices.

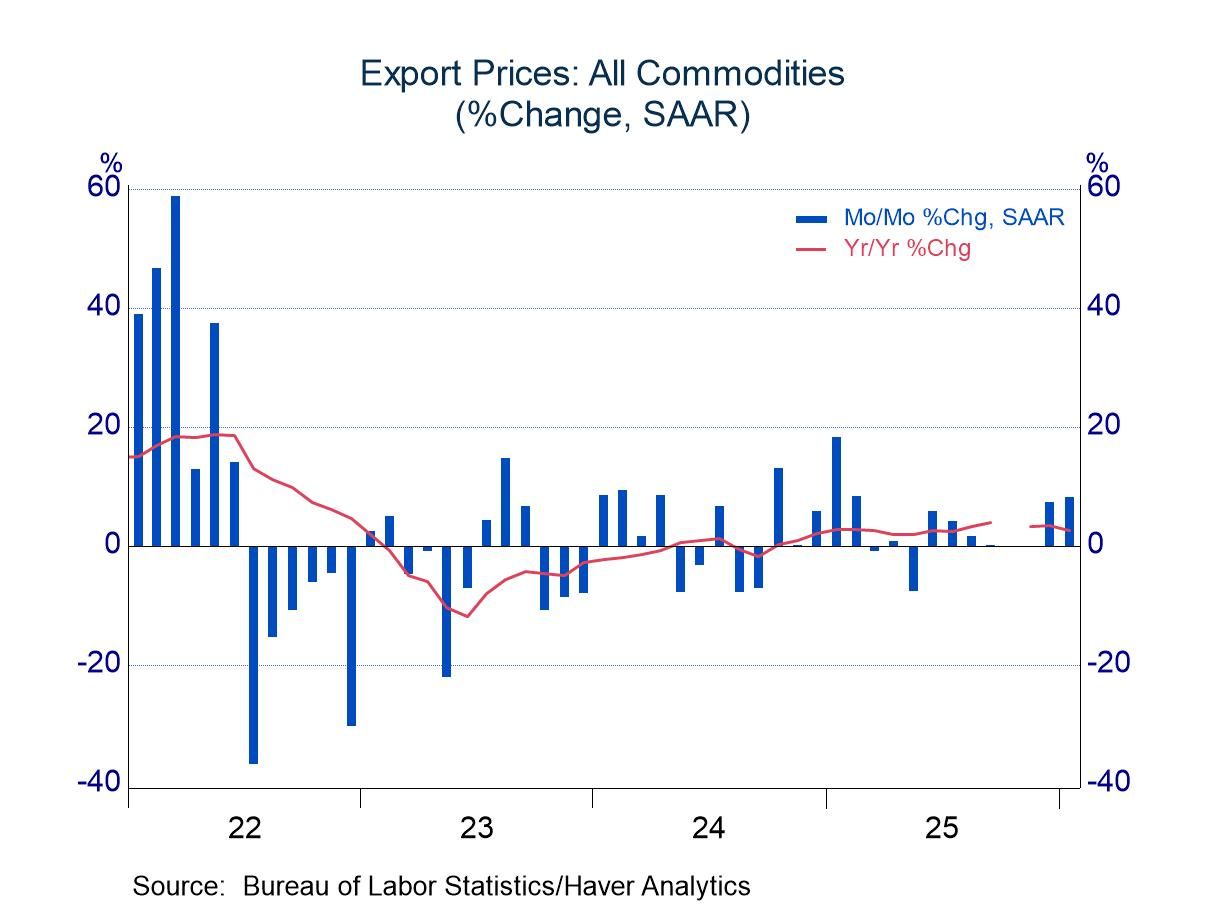

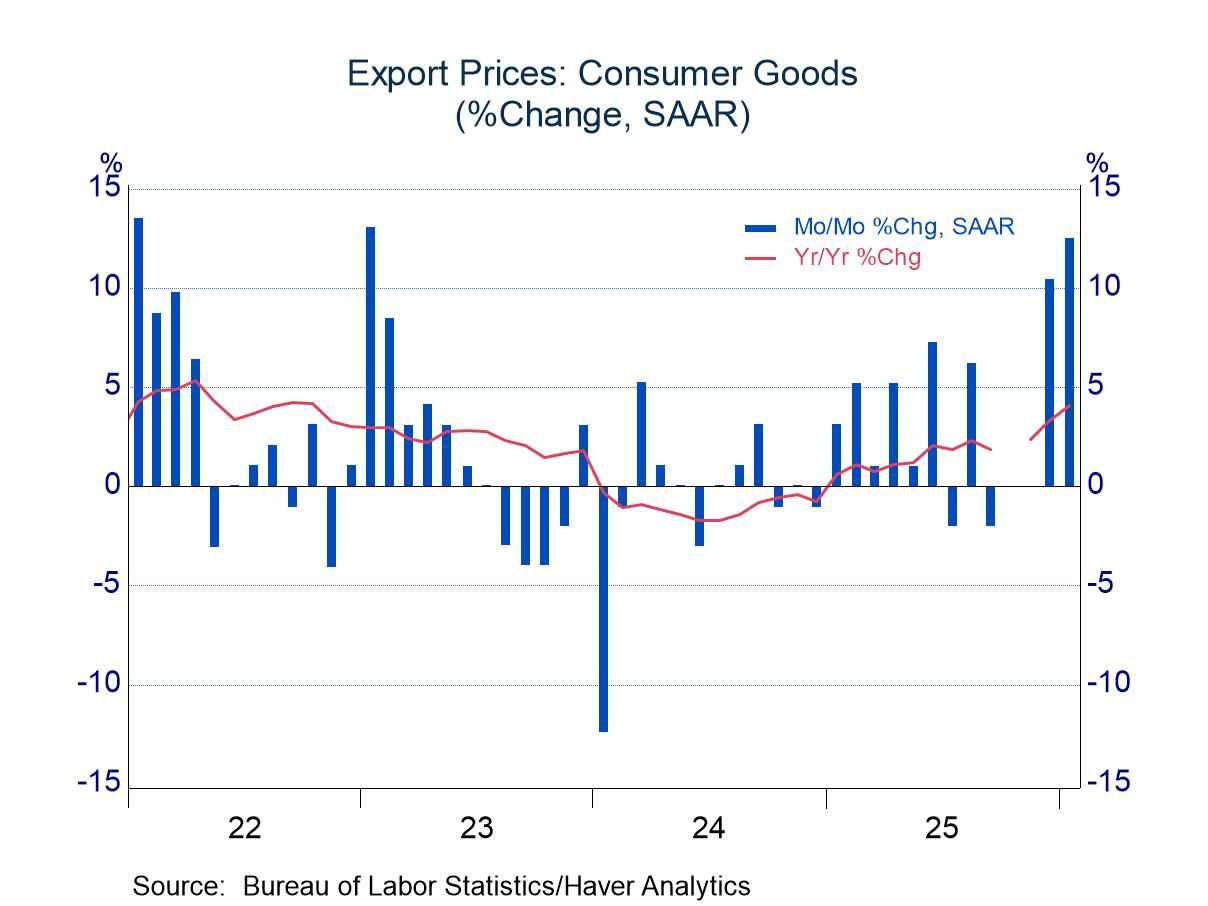

On the export side, prices rose 0.59% in December and 0.65% in January (annual rates of 7.3% and 8.0%). The jumps represent a marked deviation from the modest net change seen from March through September last year (October is not available because of the government shutdown). Several components of the headline index remained contained (automobiles, food, industrial supplies), but prices of consumer goods and capital goods surged. The cause of the acceleration is not perfectly clear. Perhaps the soft tone of the foreign exchange value of the dollar in the past year or so offered the opportunity to boost profit margins by raising dollar prices.

These import and export price series are not seasonally adjusted; they can be found in Haver’s USECON database. Detailed figures are available in the USINT database. The expectations figure from the Action Economics Forecast Survey is in the AS1REPNA database.

Michael J. Moran

AuthorMore in Author Profile »Before joining Haver Analytics in 2025, Michael J. Moran was the chief economist of Daiwa Capital Markets America Inc. He was responsible for preparing the firm’s economic forecast and interest rate outlook. He traveled frequently to visit the clients of Daiwa Capital Markets and wrote weekly economic commentary. Mr. Moran also was involved in the flux of financial markets, as he spent a portion of each day on Daiwa’s trading floor interpreting economic statistics and Federal Reserve activity for traders and salespeople. Mr. Moran is quoted frequently in the financial press, and he appears regularly on cable news shows. He also has published articles in several journals and periodicals. Before joining Daiwa Capital Markets America, Mr. Moran worked as an economist at the Federal Reserve Board in Washington, D.C. where he analyzed a broad range of issues dealing with the financial sector of the economy and regularly briefed the Board of Governors. He was on the faculty of Pennsylvania State University from 1979 to 1980 and taught on a part-time basis at George Washington University from 1980 to 1987.

Mr. Moran received his Ph.D. in economics from Pennsylvania State University in 1980 and a B.S. in business administration from the University of Bridgeport in 1975. He was a CFA charter holder from 2002 until 2016.

More Economy in Brief

Global

Global